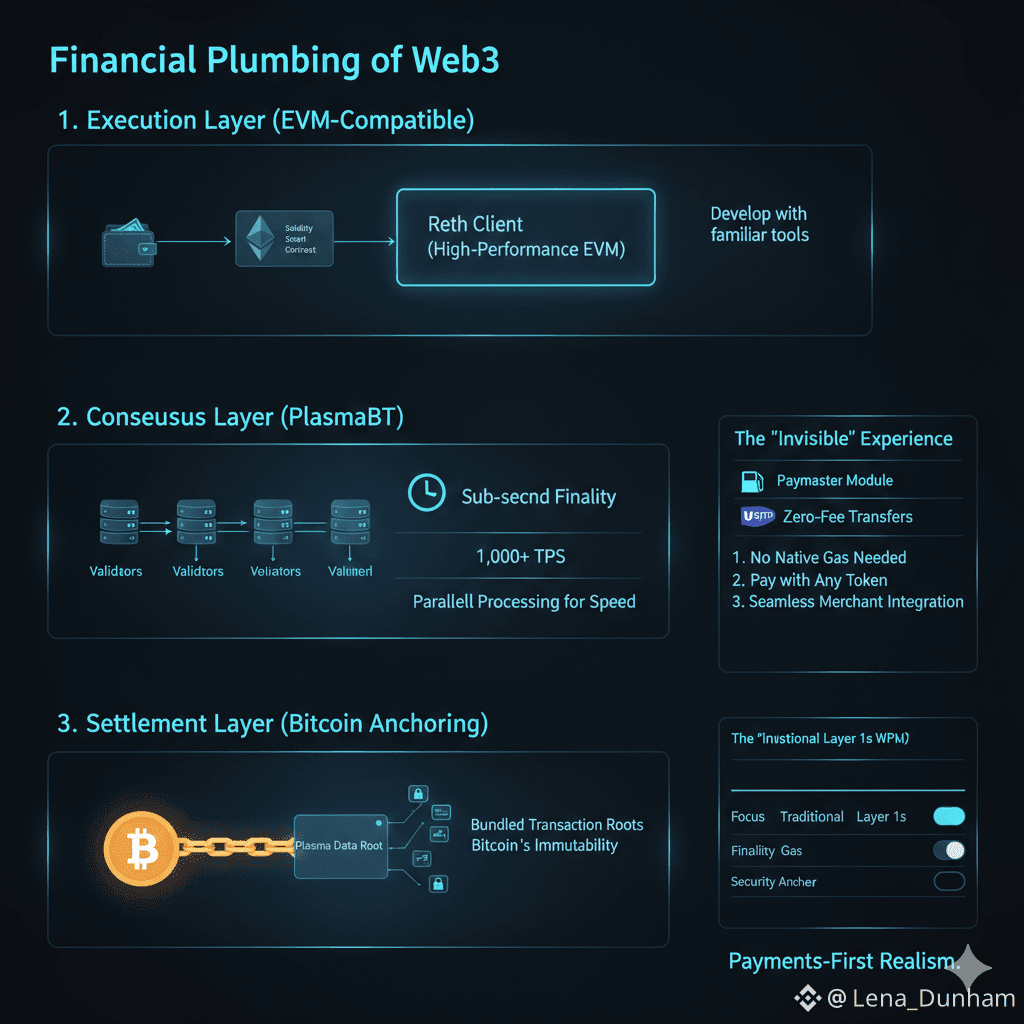

Plasma is a Layer1 blockchain purpose built for stablecoin payments and high-volume value transfer in the Web3 economy. Unlike many general-purpose chains that treat their native token as the unavoidable cost of using the network, Plasma’s design puts stablecoins especially USDT at the center of the user experience, offering features like zero-fee USDT transfers and support for custom gas tokens to lower friction in everyday transactions.

At its core, Plasma combines EVM compatibility with payment-oriented optimizations. This means developers familiar with Ethereum tooling including Solidity, Hardhat, MetaMask and other standard tools can deploy smart contracts on Plasma without relearning new languages or frameworks. The chain uses a consensus protocol called PlasmaBFT, derived from Fast HotStuff Byzantine Fault Tolerant designs, which enables fast transaction finality and the throughput needed for payment applications.

Most blockchains start with a token and then look for problems it can solve. Plasma inverts this flow. The problem it appears obsessed with is payments, not trading or speculation, but routine settlement between people, merchants, platforms, and institutions. On Binance, where XPL trades alongside thousands of other assets, it is easy to reduce Plasma to price action or market cycles. But the more interesting story sits beneath the chart. Plasma’s architecture suggests the team assumes stablecoins have already won the battle for onchain money. The real fight now is about making them usable at scale, predictably, and in environments where users do not want to think about gas tokens, wallet abstractions, or confirmation anxiety.

The decision to be fully EVM compatible may sound ordinary in 2026, but in Plasma’s case it signals pragmatism rather than conformity. By aligning with Ethereum tooling, Plasma lowers the cognitive and operational barrier for developers who already know how to ship smart contracts. This matters because payments infrastructure is not built by hobbyists alone. It is built by teams that need reliability, auditing standards, and compatibility with existing libraries. Plasma does not ask them to relearn everything. Instead, it invites them to bring familiar code into an environment tuned for fast finality and stablecoin-centric flows. That subtle design choice makes Plasma feel less like a destination chain and more like a settlement layer that wants to disappear into the background of applications.

Consensus design reinforces that intention. PlasmaBFT, derived from HotStuff-style consensus, prioritizes near-instant finality rather than probabilistic settlement. This is not an academic distinction. In a trading app, waiting a few blocks may be acceptable. At a point of sale, or in a remittance corridor where FX exposure matters by the second, it is not. Fast finality allows businesses to reason about settlement as something deterministic, closer to traditional payment networks, but without giving up onchain programmability. This is where Plasma quietly challenges the assumption that blockchains must choose between decentralization purity and user experience. Instead, it frames consensus as an economic tool, one that must align with how money behaves under time pressure.

What truly separates Plasma from many EVM peers is its treatment of stablecoins as first-class citizens. Gasless USDT transfers and alternative gas payment models are not cosmetic features. They represent an acknowledgment that asking users to acquire and manage a volatile native token just to move stable value is a tax on adoption. Plasma pushes that complexity away from end users and into protocol-level abstractions like paymasters and relayers. This is not free magic. Someone ultimately pays those costs. But by relocating them, Plasma enables applications to design payment experiences that resemble familiar fintech flows, while still settling onchain. In markets where Binance data shows stablecoin volume consistently outpacing many native assets, this design choice feels less speculative and more aligned with observed behavior.

The role of XPL itself becomes more nuanced in this context. Rather than positioning the token as the primary medium of exchange, Plasma assigns it a structural role in security, incentives, and governance. This is a quieter narrative than “number go up,” but arguably a more sustainable one. If stablecoins carry transactional demand, XPL’s value proposition is tied to the health of the network, validator participation, and the economics of abstraction layers. On Binance, traders may focus on liquidity and volatility, but long-term relevance depends on whether XPL successfully underwrites an ecosystem where stable value moves frictionlessly and at scale. That is a harder story to sell, but a more defensible one if execution holds.

Plasma’s decision to anchor periodically to Bitcoin adds another layer to this story. Anchoring is not about borrowing hype from Bitcoin maximalism. It is about signaling security and auditability to institutions that already trust Bitcoin as a neutral reference point. For regulated entities, that external checkpoint can matter more than internal claims about decentralization. At the same time, anchoring introduces real trade-offs. It creates costs, governance questions, and dependencies on another chain’s economics. Plasma seems aware of this tension and treats anchoring as a credibility mechanism rather than a cure-all. In a world where payment infrastructure must satisfy auditors as much as developers, this hybrid approach may prove more realistic than purist designs.

Yet no serious infrastructure story is complete without acknowledging risk. A stablecoin-first network inherits the systemic vulnerabilities of the stablecoins it relies on. Regulatory action, issuer risk, or liquidity shocks can ripple through usage far more violently than on chains where the native token dominates. Plasma’s architecture concentrates these questions rather than avoiding them. Gasless transfers depend on robust relayer economics. Paymaster models must remain solvent across market cycles. Governance decisions around fees and incentives will shape whether the network remains neutral or drifts toward capture by a small set of large participants. These are not theoretical concerns. They are the exact pressure points where payment systems succeed or fail.

The more compelling way to view Plasma is as an experiment in prioritization rather than technology. Instead of asking how to be the fastest or most decentralized in abstract terms, Plasma asks which frictions actually prevent people from using crypto as money. That leads to uncomfortable but practical answers: onboarding, predictable costs, instant settlement, and compliance-friendly design. The network’s roadmap, when viewed alongside Binance market data showing sustained demand for stablecoin pairs, suggests Plasma is betting that infrastructure which feels boring to speculators can still be essential to the next wave of adoption.

In the end, Plasma’s relevance will not be decided by whitepapers or influencer threads. It will be decided by whether merchants integrate it without friction, whether developers choose it as a default settlement layer, and whether users can move stable value without even realizing which chain they are on. If XPL becomes the quiet enabler of that experience, it may never dominate headlines, but it could embed itself deeply into the financial plumbing of Web3. In an industry that has spent years chasing novelty, Plasma’s bet on payments-first realism might be exactly what makes it endure.