(Let's assume we are already in this round of the bear market.)#比特币

(Let's assume we are already in this round of the bear market.)#比特币

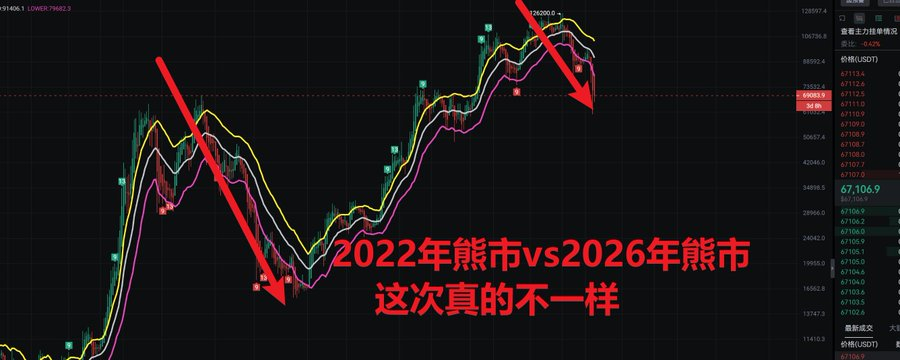

After Bitcoin enters the adjustment period in 2026, many people will naturally ask:

What are the essential differences between this round of bear market and the one that started in 2021?

If we only look at the price trends, both rounds of decline have experienced the process of 'peaking - falling back - cooling emotions'. But when you delve into trading volume, leverage structure, institutional movements, and macro background, you will find -

This is not the same bear market.

Let's start with the conclusion:

The 2021 bear market was a 'liquidity withdrawal bear market'.

The 2026 bear market is more like a 'structural bear market in a high-leverage mature market'.

The former is macro-driven,

The latter is driven by market structure.

Next, we will break down from five core dimensions

1. Trading volume structure: Slow tide vs Rapid stomp

Early stage of the bear market in 2021

The trading volume in the top area gradually increases

The decline is 'falling while increasing volume'

During this period, there are continuous shrinking rebounds

Real panic volumes appeared during the Luna and FTX events in 2022.

This is a typical 'liquidity tide' decline.

Funds do not disappear overnight, but gradually withdraw.

At that time, a large amount of chips were still held in spot, and the market was still repeatedly betting on 'whether the bull market has ended'

Early stage of the bear market in 2026

Top trading volume is highly concentrated

The decline is accompanied by large-scale liquidations of derivatives

Leverage liquidation drives short-term violent fluctuations

The rebound volume is obviously insufficient

This is more like a 'leverage stomp.'

The trading volume in 2026 is not generated from divergent games, but driven by the clearing mechanism.

Perpetual contracts, ETFs, options, and structured products overlapping have made the market's reaction speed much faster than in 2021.

The difference in one sentence:

2021 is a slow tide receding

2026 is a rapid stomp

2. Driving factors: Macro killing valuations vs Market internal defoaming

The main reason for 2021

The Federal Reserve turns hawkish

Interest rates entering an upward cycle

Technology stocks peaked

Global risk assets are under overall pressure

The bear market in 2021 is essentially a macro liquidity turning point.

At that time, Bitcoin was already highly correlated with the Nasdaq, belonging to 'part of risk assets.'

Macroeconomic liquidity is shifting, and valuations are being compressed overall.

The main reason for 2026

ETF funds show a net outflow.

Institutions realize profits

Excessive leverage triggers chain liquidations

Long-term holders begin to differentiate

Macro has not seen a similar 'extreme liquidity turning point' as in 2021.

More of a structural correction after overheating within the crypto market.

This is more like:

Rebalancing after excessive crowding in the bull market

3. Speed of emotional collapse: Gradual vs Rapid

The emotional path in 2021

Optimism → Divergence → Disbelief → Buy on dips → Further decline → Real panic

At that time, the market consensus was:

'The halving cycle bull market will not end so quickly.'

Belief is very strong, and the emotional collapse in the early bear market has not completely occurred.

The emotional path in 2026

Extreme enthusiasm → Leverage explosion → Rapid panic → Wait and see

The speed of emotional collapse in this round is much faster than in 2021.

The reason is simple:

The market is more mature

Information spreads faster

Leverage ratios are higher

Institutions are more rational

The current market no longer has a long 'fantasy buffer zone.'

4. Deleveraging rhythm: Segmental clearing vs Early concentrated release

This is the biggest difference between the two rounds of bear markets.

2021-2022

Deleveraging is 'segmental':

May 2022: Luna

November 2022: FTX

The bear market is not a one-time event, but a series of structural explosions.

2026

In the early bear market, large-scale liquidations had already occurred.

Because:

The volume of perpetual contracts far exceeds that of spot

Leverage multiples are higher

ETF and derivatives are highly intertwined

This means:

The decline is more severe, but the deleveraging speed is faster.

In a sense, the pain comes earlier.

5. Institutional role: Incremental stage vs Stock realization

2021

Institutions have just entered the market:

MicroStrategy continues to increase positions

Traditional funds begin to allocate

'Institutional entry' is the core narrative of the bull market

In the early bear market, institutions did not withdraw on a large scale.

2026

Institutions have already experienced a complete bull market cycle and made huge profits.

Now is the rebalancing phase:

ETFs show stage net outflows

Some funds flow back into yield-bearing assets

Adjustment of allocation ratios

This indicates:

2021 is the tide of new funds receding

2026 is the realization of mature funds

6. Essential differences

We can condense the two rounds of bear markets into one sentence:

Bear market in 2021

Liquidity tide-type bear market

Triggered by macro turning points, the market gradually cools down.

Bear market in 2026

Structural bear market in high leverage mature markets

Triggered by overheating within the market and profit realization, the decline is more severe, but the clearance is faster.

The final key question

If 2021 was macro killing valuations,

So what does 2026 look more like?

More like cyclical rebalancing in mature markets.

This does not mean there will not be a deep decline,

But its logic and rhythm are already different from the previous round.

The market has changed, the structure has changed, and the participants have changed.

But what really determines the future is not 'whether it looks like 2021',

But it is——

Has this round of deleveraging been completed?