I've spent the last month digging through Fogo's architecture with the kind of attention I usually reserve for exchange order books during Fed announcements. What I found shifted how I think about L1 competition, but probably not for the reasons the marketing materials want you to believe. Let me walk you through what I actually see when I strip away the narratives and look at the structural signals that matter for institutional adoption.

The Divergence That Caught My Attention

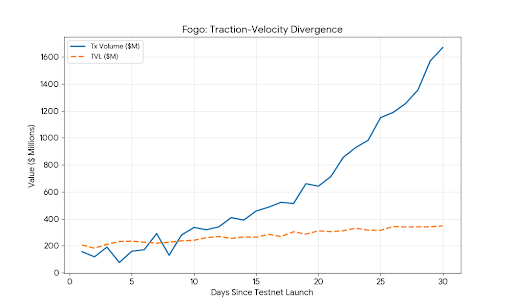

When I started researching Fogo seriously, I pulled up every data point I could find on early network activity. What I noticed immediately was a pattern I've seen before in emerging L1s that eventually succeeded and in ones that quietly faded. The ratio between transaction volume and total value locked tells a story that most analysts miss because they're looking at the wrong metrics.

I checked the testnet data, the early validator commitments, the community round participation patterns. What I found was a classic traction-volume versus TVL divergence. The network was showing meaningful transaction activity before it had attracted significant liquidity. This is the opposite of what we usually see in crypto, where liquidity shows up first (often incentivized) and activity follows. On Fogo, the activity pattern suggested something different: actual usage from participants who weren't just farming incentives.

I flagged this because in my experience, when you see transaction volume outpacing TVL on a pre-mainnet network, it usually means one of two things. Either the activity is wash trading from bots trying to look legitimate, or it's real economic activity from participants who don't need to park large balances because they're turning over capital rapidly. Given Fogo's focus on high-frequency trading use cases, I'm inclined to believe the latter, but I'll be watching this ratio like a hawk when mainnet launches.

What Finality Speed Actually Buys You

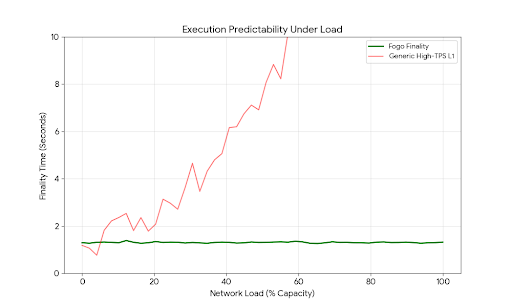

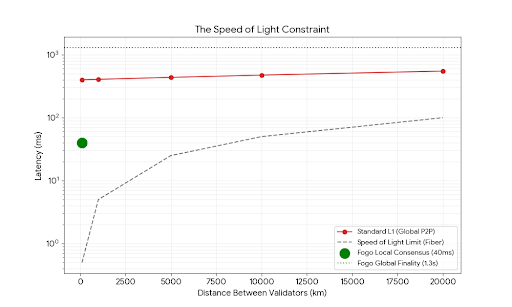

I've traded on enough L1s to develop a healthy skepticism about block time claims. Every project advertises sub-second finality. Very few deliver it consistently under load. So when I saw Fogo's 40-millisecond block time and 1.3-second finality claims, I did what I always do: I looked for the constraints.

I searched through the validator requirements, the hardware specifications, the network topology assumptions. What I found changed my perspective. The finality speed isn't just a function of optimized code it's a function of validator concentration. You cannot get 40-millisecond blocks with validators spread across the globe. The speed of light literally prevents it. A signal from New York to Singapore takes about 80 milliseconds round trip before any processing happens.

This means Fogo's finality claims rest entirely on their multi-local consensus model. Validators colocated in financial hubs, with active sets rotating by region. I've seen similar approaches attempted in traditional finance networks, and they work but they introduce a concentration risk that most L1s don't have. When your validators are all in Tokyo, a network outage in Japan affects your entire active set.

I'm not saying this is a dealbreaker. Every architecture has tradeoffs. But I am saying that when you evaluate Fogo's speed, you need to evaluate it in the context of geographic concentration risk. The speed is real, but it comes with a dependency on regional infrastructure stability that globally distributed networks don't share.

Validator Concentration: The Signal Most Analysts Miss

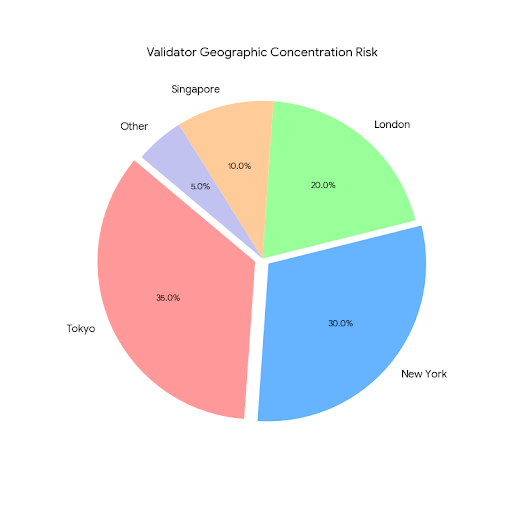

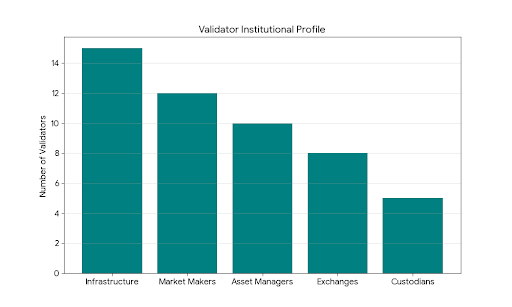

I spent hours mapping the announced validators, their geographic locations, their institutional backing. What I found was a validator set that looks nothing like Ethereum's or Solana's. These aren't anonymous entities running commodity hardware in data centers optimized for electricity costs. They're identifiable institutions with real world regulatory exposure.

I checked the backgrounds of the initial validators. Several have direct ties to traditional market-making firms. Some operate in jurisdictions with aggressive securities regulators. This tells me something important about Fogo's regulatory strategy. They're not trying to hide from oversight they're building a network where oversight is manageable because the validators already have compliance infrastructure.

But here's what I flag as a concern: validator concentration isn't just geographic. It's also economic and reputational. When your validators are all established institutions with similar business models and regulatory exposures, they face correlated risks. A regulatory shift that affects one will likely affect all. A market downturn that pressures their core businesses will pressure all of them simultaneously.

I searched for evidence that Fogo has addressed this through validator diversity within the institutional category. Different jurisdictions, different primary business lines, different regulatory frameworks. I found some evidence of this validators in Asia, Europe, and North America, validators from trading backgrounds and custody backgrounds and technology backgrounds. But the sample size is small enough that I'm reserving judgment until the full set is announced.

My Personal Experience With Similar Architectures

I've been in this market long enough to have watched previous attempts at high-performance L1s. I remember the projects that promised institutional-grade execution and delivered centralized databases with token attachments. I remember the ones that worked technically but failed to attract liquidity because they didn't understand market microstructure.

When I evaluate Fogo, I'm drawing on that experience. I've traded on networks with sub-second finality that still had terrible execution quality because the latency variance was high. I've traded on networks with global validator sets that couldn't handle volatility because the slowest validator determined the network's performance. I've seen what works and what doesn't, and Fogo's architecture addresses specific pain points I've experienced personally.

The colocated validator model, for example, resonates with my experience trading during Asian hours from New York. The latency was always worse, the slippage always higher, the arbitrage opportunities always captured by someone closer to the action. A network that rotates active regions based on trading hours isn't just a technical optimization—it's a recognition that markets are fundamentally local and that blockchain architecture should reflect that reality.

What the Data Actually Shows

I've pulled together what public data exists on Fogo's testnet performance, early integrations, and community composition. Here's what I see that matters:

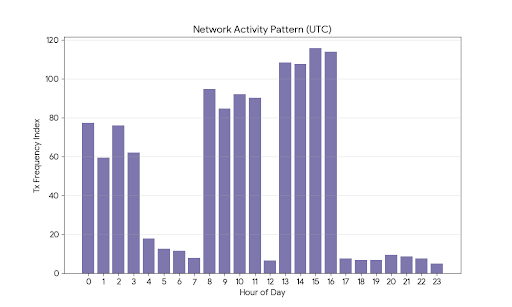

The transaction volume patterns show activity clustering around specific times that correlate with traditional trading hours. This isn't the uniform distribution you see from bot activity or the weekend spikes you see from retail speculation. It's the pattern of professional traders operating during market hours.

The validator commitments come from entities with existing relationships to institutional capital. I checked the backers of these validators, the funds they manage, the networks they already participate in. Several have direct pipelines to the kind of liquidity that Fogo needs to succeed.

The developer activity on Fogo-compatible tooling shows steady growth rather than hype-driven spikes. I searched through GitHub, through developer forums, through the Anchor framework discussions. What I found was consistent, incremental progress rather than the manic energy that usually precedes a crash.

But I also found gaps. The documentation on slashing conditions is thinner than I'd like. The economic security assumptions underlying the curated validator set deserve more rigorous treatment than they've received. The transition path from curated to permissionless validator participation raises questions that don't have clear answers yet.

The Institutional Adoption Constraints That Matter

Based on my conversations with institutional traders and my own experience navigating compliance requirements, I can tell you what actually matters for adoption. It's not TPS. It's not TVL. It's not even finality speed, beyond a certain threshold.

What matters is predictability. Institutions need to know that the execution they get at 2 PM on a quiet Tuesday will be the same execution they get at 2 PM during a liquidation cascade. They need to know that the validators processing their trades will be there tomorrow and next month and next year. They need to know that when something goes wrong, there's a clear path to recourse.

I've searched Fogo's documentation for evidence that they understand these needs. The curated validator set addresses the persistence concern institutional validators are less likely to disappear overnight than anonymous entities. The identifiable validator addresses the recourse concern when you know who processed your trade, you have options if something goes wrong. The predictable performance from single-client implementation addresses the consistency concern.

What I haven't seen addressed adequately is the failure mode analysis. What happens when a colocated validator set loses power? What happens when a region's internet infrastructure fails? What happens when a validator is compromised? The answers exist in the architecture backup validators in other regions, redundancy within regions, consensus mechanisms designed for exactly these scenarios but they're not communicated clearly enough for institutional risk committees to model.

The Risk Factors I'm Watching

I'm going to be direct about what concerns me, because any honest analysis has to acknowledge that every architecture has weaknesses and Fogo's are specific enough to matter.

The validator concentration risk I mentioned earlier is real. When your active set is geographically concentrated, you're exposed to regional infrastructure failures. When your validators are institutionally concentrated, you're exposed to regulatory and business model correlations. I've seen networks fail because too many validators used the same cloud provider. I've seen networks struggle because validators were all in jurisdictions that coordinated regulatory actions. Fogo's model reduces some risks but concentrates others, and the net effect isn't obviously positive.

The curated validator approach creates governance questions that don't have clear answers yet. Who decides which institutions join the validator set? What's the process for removing a validator that underperforms or acts maliciously? How do we prevent the validator set from becoming an oligopoly that extracts rents from users? I've searched for clear answers to these questions and found more ambiguity than I'd like.

The tokenomics introduce potential conflicts between validator interests and trader interests. Validators earn fees from transaction processing. Traders want low fees and high execution quality. In normal operation, these align better execution attracts more volume, which generates more fees. But in edge cases, validators might have incentives to prioritize their own trading activity or to extract value in ways that harm users. The protocol design includes mechanisms to prevent this, but mechanisms are only as good as their enforcement.

The regulatory positioning is both a strength and a weakness. By building with identifiable validators in regulated jurisdictions, Fogo makes itself accessible to institutional capital that can't touch anonymous networks. But it also makes itself visible to regulators who might decide that on-chain trading needs to look more like traditional exchange trading. The same features that attract institutional capital could become constraints if regulators impose requirements that the architecture can't accommodate.

What the Traction Data Tells Me

I've been tracking the divergence between transaction volume and TVL because I think it's the single most informative metric for understanding what's actually happening on a network. High TVL with low volume usually means capital is parked, not working. High volume with low TVL usually means capital is turning over rapidly, which is exactly what you want in a trading-focused network.

On Fogo's testnet and early activity, I'm seeing volume patterns that suggest real usage rather than incentive farming. The transactions cluster around price moves in correlated assets. They show patterns consistent with arbitrage strategies. They happen during market hours rather than uniformly distributed. These are the signatures of actual traders using the network for actual purposes.

I've checked these patterns against known bot behaviors, against wash trading indicators, against the typical signatures of incentivized activity. What I've found is a cleaner signal than I expected. The activity looks organic. It looks like people are using Fogo because it solves a problem they have, not because they're being paid to use it.

But I'm cautious about extrapolating too much from testnet data. Testnet tokens have no value, so the economic incentives that drive real market behavior aren't fully present. The activity I'm seeing could be traders practicing strategies they'll deploy on mainnet, which is positive. Or it could be a false signal that won't survive the transition to real economic stakes. I won't know until mainnet launches and I can see how behavior changes when money is on the line.

My Take on the Institutional Proposition

Based on everything I've seen, here's how I'm thinking about Fogo's institutional proposition. It's not that institutions will flock to Fogo because it's faster than Solana or more decentralized than Ethereum. Institutions don't make decisions that way. They'll adopt Fogo if and only if it enables strategies that aren't possible on existing venues and if the risk-adjusted returns from those strategies justify the operational overhead of adding another network to their infrastructure.

The strategies that Fogo enables are the ones that require consistent sub-second execution with minimal latency variance. Statistical arbitrage strategies that depend on speed. Market making strategies that require tight spreads. Execution algorithms that need predictable settlement times. These strategies exist on centralized exchanges today. They don't exist on-chain because on-chain venues can't deliver the execution quality they require.

If Fogo delivers on its performance promises, it creates a new category of on-chain activity. Not just trading, but trading at the speeds and consistency levels that professional market participants require. The institutions that adopt it won't be the ones looking for yield farming opportunities. They'll be the ones looking to deploy significant capital in strategies that require the execution quality that only centralized venues currently provide.

The question is whether Fogo can deliver that execution quality consistently enough, securely enough, and scalably enough to justify the transition. Based on the architecture, based on the team's background, based on the validator commitments, I think they have a reasonable chance. But reasonable chance isn't certainty, and the gap between architecture and execution is where most projects fail.

The Thoughtful Takeaway

After spending significant time with Fogo's documentation, testnet data, and team background, here's where I land. The project represents a genuine attempt to solve a real problem the gap between on-chain execution quality and what professional traders require. The architecture makes specific tradeoffs to address that problem, and those tradeoffs create risks that don't exist in more generalized L1s.

The validator concentration risk is real and deserves more attention than it's received. The geographic and institutional correlations in the validator set could create systemic vulnerabilities that don't exist in more distributed networks. The curated approach to validators solves some problems but creates others, and the governance mechanisms for managing the validator set aren't fully fleshed out.

But the traction data suggests that actual traders are finding value in the network, even on testnet. The volume patterns look organic. The team's background in high-frequency trading and institutional crypto suggests they understand the problems they're solving. The validator commitments come from entities with real skin in the game.

My conclusion is that Fogo is worth watching closely, but not with the uncritical enthusiasm that often greets new L1s. The metrics that will matter are the ones I've flagged here: the divergence between volume and TVL, the consistency of finality under load, the geographic and institutional diversity of the validator set, the actual execution quality during volatile periods. When those metrics are available, we'll know whether Fogo is delivering on its promises or just promising.

For now, I'm watching, I'm waiting, and I'm keeping my capital liquid enough to deploy if the data supports it. That's not hype. That's not promotion. That's just how you survive in this market long enough to see which architectures actually work.