A Structural Analysis of Banks, Neobanks and DeFi Banks

Financial systems are undergoing a structural shift comparable to the early evolution of the internet.

The transition is not simply about “crypto replacing banks.”

It is about how financial infrastructure is organized and where trust resides within the system.

Over the last decade, three distinct banking architectures have emerged.

Traditional Banks

Neobanks

DeFi Banks

Each represents a different model for organizing custody, liquidity, credit creation, and settlement.

The result is a new financial topology where institutions, software platforms and open protocols coexist.

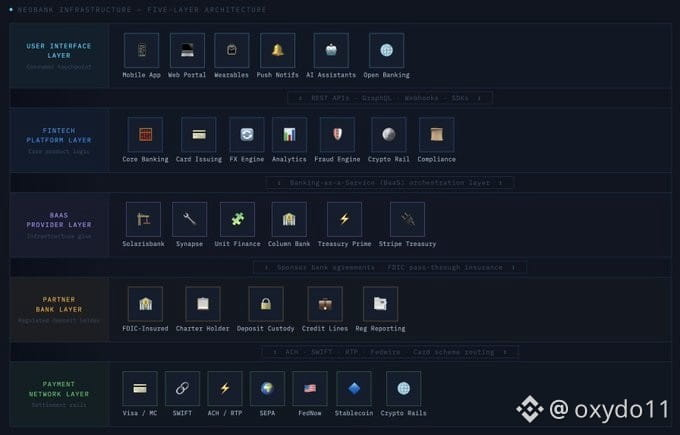

The Financial Infrastructure Stack

To understand the differences between these systems, it helps to decompose finance into its functional layers.

Every financial system must solve four problems.

Identity

Custody

Liquidity

Settlement

These layers form the core architecture of financial infrastructure.

Traditional Banks

Institutional Credit Infrastructure

Traditional banks remain the backbone of the global financial system.

They perform three essential economic functions.

Deposit custody

Credit creation

Payment settlement

Unlike most digital platforms, banks operate through state-backed regulatory frameworks and central bank settlement systems.

Hierarchical Liquidity Structure

Modern banking operates as a multi-tier liquidity network.

Central Banks

Reserve currency issuance

Interbank settlement

Commercial Banks

Deposit custody

Loan origination

Payment Institutions

Consumer and merchant services

Commercial banks hold reserve accounts at central banks.

When banks settle transactions between each other, the final settlement occurs through central bank reserves.

Credit Creation

Banks expand the money supply through lending.

When a bank issues a loan, it simultaneously creates a deposit on its balance sheet.

Loan Issued

New Deposit Created

Money Supply Expands

This balance-sheet expansion mechanism makes banks the primary credit engines of modern economies.

System Characteristics

Institutional custody

Centralized liquidity management

Regulatory oversight

Permissioned financial access

While this architecture provides stability and monetary policy control, it introduces structural friction.

Settlement can take hours or days.

Cross-border payments rely on intermediary banking networks.

Financial access remains uneven globally.

These limitations opened the door to fintech innovation.

Neobanks

The Software Layer of Traditional Finance

Neobanks represent the digitization of banking distribution rather than a reinvention of financial infrastructure.

They are software platforms that deliver financial services through modern digital interfaces while relying on existing banking rails.

Most neobanks operate through Banking-as-a-Service partnerships with licensed institutions.

In this model, the neobank functions as the operating system for financial services, while the underlying bank remains responsible for balance sheet operations.

Key Innovations

Real time financial visibility

Global card infrastructure

Improved fee transparency

API-driven financial services

Neobanks transformed the user experience of banking.

However the fundamental financial infrastructure remained largely unchanged.

Settlement still occurs through legacy payment rails.

Liquidity still resides within regulated banking institutions.

The deeper shift appears in decentralized finance.

DeFi Banks

Protocol Based Financial Markets

Decentralized finance introduces a fundamentally different architecture.

Instead of relying on institutional intermediaries, DeFi uses blockchain networks and smart contracts to coordinate financial activity.

Protocols replicate core banking functions.

Lending

Trading

Collateralized credit

Asset issuance

But they do so without centralized custodians.

DeFi Financial Stack

Users interact directly with protocols through cryptographic wallets.

Liquidity is supplied by participants who deposit capital into shared pools.

Interest rates and collateralization parameters are governed algorithmically.

Credit Markets in DeFi

Traditional banking

Depositors → Bank Balance Sheet → Borrowers

DeFi lending

Liquidity Providers → Smart Contract → Borrowers

Protocols such as $AAVE , $SKY and Compound operate as automated credit markets, where capital allocation occurs through transparent onchain rules.

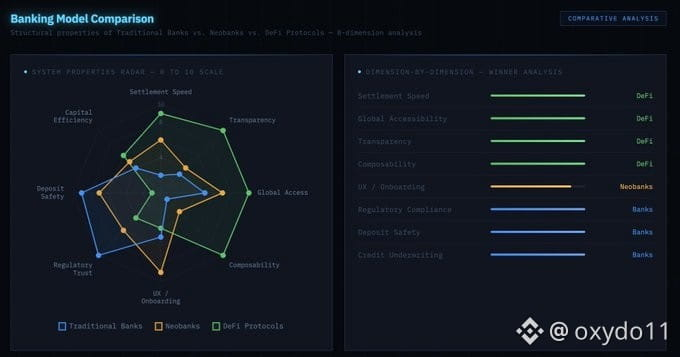

Structural Properties

Permissionless access

Global liquidity pools

Transparent accounting

Continuous settlement

DeFi therefore transforms finance from an institutional system into a programmable infrastructure layer.

However the model also introduces new constraints.

Collateral efficiency remains limited.

Smart contract vulnerabilities require rigorous security frameworks.

Regulatory frameworks are still evolving.

Despite these challenges, DeFi represents the first time financial infrastructure has been built as open source software.

Comparative Architecture

Each architecture optimizes for different priorities.

Banks prioritize stability and regulatory compliance.

Neobanks prioritize usability and accessibility.

DeFi prioritizes openness and programmability.

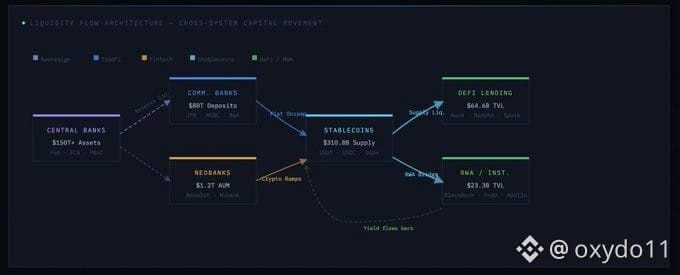

Toward a Hybrid Financial System

The next generation of financial infrastructure will likely combine elements of all three systems.

Traditional institutions are experimenting with tokenized assets.

Payment companies are integrating stablecoin settlement.

DeFi protocols are developing compliance frameworks for institutional participation.

Emerging architectures include

Tokenized treasury markets

Onchain money markets

Stablecoin payment networks

Institutional #defi liquidity pools

Rather than replacing existing systems, blockchain infrastructure is increasingly acting as an alternative settlement layer within global finance.

The Core Transformation

The most important shift is not technological but structural.

Financial systems historically relied on trusted intermediaries to coordinate economic activity.

Decentralized finance proposes a different model where financial coordination occurs through programmable protocols.

Banks institutionalized trust.

Neobanks digitized access to financial services.

DeFi attempts to embed trust directly into infrastructure.

This transition marks the beginning of a new phase in financial architecture where institutions, software platforms, and decentralized protocols operate within the same economic network.

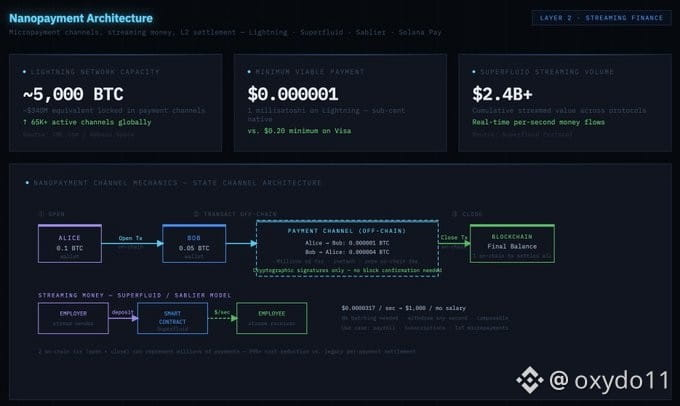

Nanopayments and the Next Economic Layer of the Internet

Nanopayments might sound like a niche feature, but they’re actually one of the clearest signs that the payment system is changing.

In the traditional world, paying “tiny” amounts just doesn’t work. Cards and banks have minimum fees, batch settlement, intermediaries, and fixed costs baked in. So anything like paying a few cents or fractions of a cent, becomes pointless. That’s why the internet ended up leaning so hard on subscriptions and ads instead of true pay per use.

Onchain rails change the shape of that problem. When settlement is faster, cheaper and programmable, you can start to pay at the level of actions instead of invoices. A fraction of a cent to read an article section, value streamed per second for a service, automatic micro rewards to creators, or even machine-to-machine payments where agents pay other agents for data, compute, or execution.

The big idea is simple. When money can move in extremely small amounts without friction, the internet gets a new business model. Less “paywalls and ads,” more “fair pricing per usage,” more direct creator revenue, and eventually a world where digital services charge and get paid in real time.

Nanopayments are not just about smaller payments. They’re about a more native way for value to move online.