Peter Thiel, the renowned contrarian billionaire investor and co-founder of PayPal and Palantir, has a long history of bold, unconventional bets. A US Securities and Exchange Commission (SEC) filing revealed that Thiel-linked Founders Fund entities exited ETHZilla after disclosing a 7.5% stake in 2025. ETHZilla is an Ether-focused digital asset treasury company.

The sale underscores broader market pressures on Ether treasury models, as ETHZilla’s stock has fallen sharply from its summer 2025 highs amid falling Ether prices. This comes at a time when investor enthusiasm for leveraged or equity-wrapped crypto exposure appears to be waning.

This article examines why Thiel’s Founders Fund exited ETHZilla and analyzes the risks of leveraged Ether treasury models, debt-driven balance sheets and forced asset sales. It explores what the move signals about volatility, capital discipline and the sustainability of public crypto treasury strategies.

ETHZilla: From biotech to Ether treasury

In July 2025, biotech company 180 Life Sciences made a bold shift, raising $425 million to launch an Ether-focused treasury strategy and rebranding as ETHZilla. It positioned itself as a publicly traded vehicle for gaining exposure to Ether, with plans to build up its Ether holdings and deploy them in decentralized finance (DeFi) protocols and tokenized asset initiatives.

Just two months later, ETHZilla sought to secure an additional $350 million through convertible bonds to expand its reserves and support further projects. Reports indicated that the company held over 100,000 ETH on its balance sheet at one stage.

The idea behind the endeavor was straightforward: Secure funding, buy and hold Ether, generate potential returns through staking or DeFi activities and offer public shareholders leveraged exposure to Ether’s growth.

However, the strategy faced significant challenges as market conditions deteriorated.

ETHZilla’s pivotal sale and Peter Thiel’s exit

As crypto markets retreated from their earlier highs, ETHZilla began reducing its Ether position.

In December 2025, ETHZilla sold 24,291 ETH, generating roughly $74.5 million at an average price of about $3,068 per coin. The stated purpose of the sale was to meet debt repayments. Following the transaction, its Ether holdings reportedly fell to around 69,800 ETH.

The sale of ETH marked a pivotal turning point for the company.

For a company built around an Ether treasury, being forced to offload ETH to cover debt highlighted a fundamental vulnerability. Combining leverage with crypto’s volatility can trigger the sale of holdings at any time. A strategy originally designed for patient, long-term accumulation can quicklytransform into a scramble to stabilize the balance sheet.

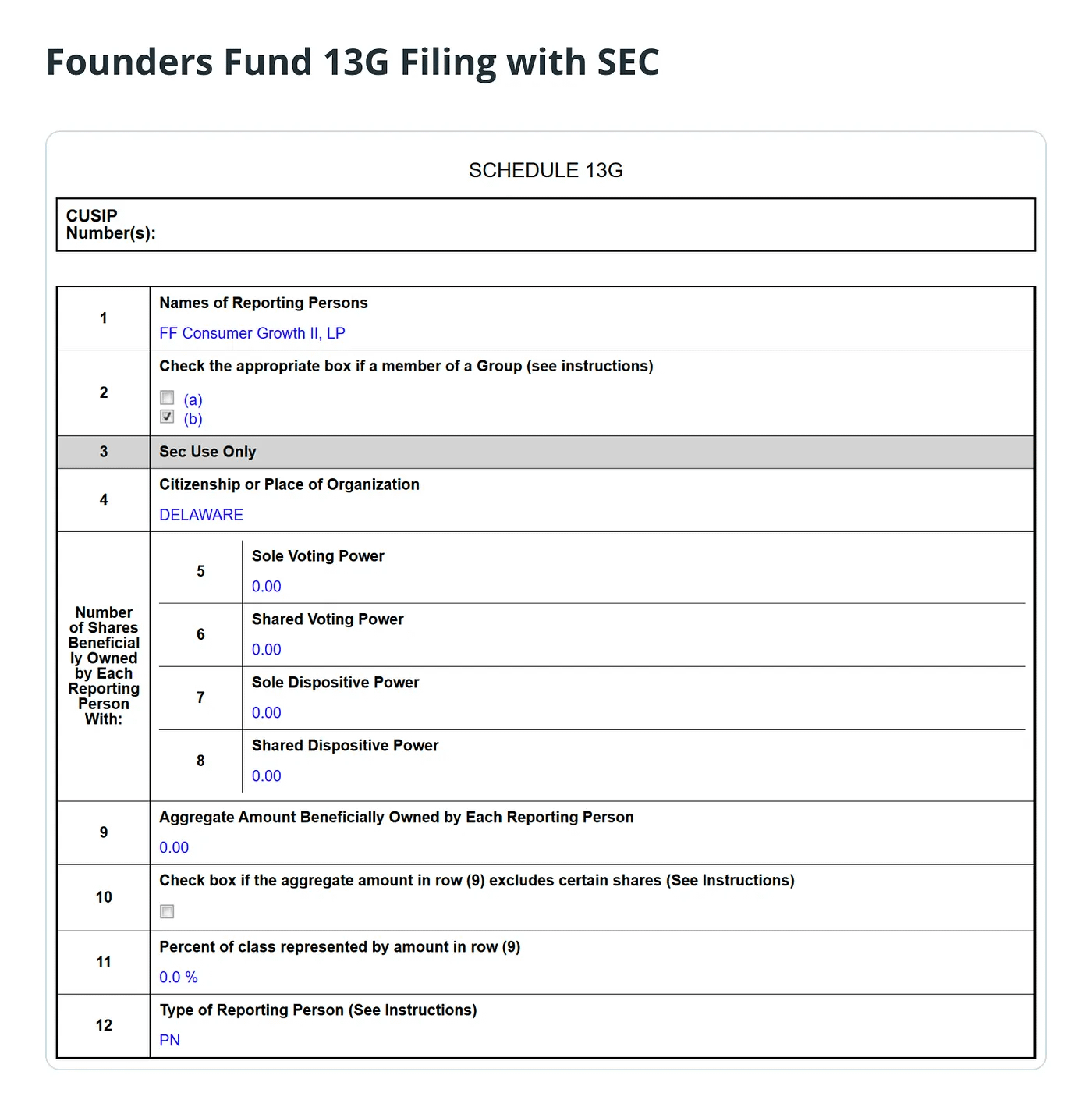

Not long afterward, Thiel’s Founders Fund reduced its ownership in ETHZilla to zero, fully exiting its position by the end of 2025, according to SEC filings.

Bitcoin vs. Ether treasuries: Store of value vs. layers of hidden complexity

While comparisons to Bitcoin treasury strategies are inevitable, Ether introduces layers of complexity that Bitcoin treasuries typically avoid.

Heightened volatility amplified by leverage

Ether tends to experience greater price volatility driven by underlying sentiment compared to Bitcoin. This behavior stems from Ether’s role as both a digital asset and the fuel for a programmable blockchain platform. When treasury companies rely on convertible debt or other forms of leverage, drawdowns may trigger forced selling.

Yield pursuit introduces new risks

Bitcoin treasury companies typically follow a straightforward hold-and-appreciate model. Ether-focused companies, on the other hand, often emphasize staking rewards or DeFi yields to enhance returns. However, this approach comes with trade-offs:

Smart contract exploits and bugs

Slashing penalties or validator downtime

Liquidity lock-up periods

Counterparty and protocol risks.

What promises higher returns can also increase operational complexity and systemic vulnerabilities.

Greater narrative and perception challenges

Bitcoin treasury players benefit from a “digital gold” narrative rooted in scarcity and store of value appeal. Ether, however, represents a dynamic, evolving ecosystem shaped by network upgrades, gas fee dynamics, shifting regulatory views and competition from other blockchains. This added complexity heightens uncertainty and makes it harder for markets to price the strategy.

Ether accumulators following diverse paths

Not all companies that opted for Ether treasuries reacted similarly to the downturn in crypto markets.

Some of these companies continued to accumulate ETH, trusting that Ether’s long-term network expansion and utility would outweigh near-term price turbulence. Others took the opposite path, liquidating all or a significant portion of their holdings and realizing substantial losses.

This divergence in approaches suggests that the Ether treasury model is not inherently flawed or doomed across the board. Its sustainability depends on factors such as leverage levels, risk controls and resilience to market cycles.

Capital structure risks in volatile asset classes

Convertible debt structures can amplify potential gains in bull markets by providing relatively low-cost leverage to acquire additional assets such as Bitcoin, effectively magnifying returns as prices rise.

When companies trade at premiums to their net asset value (NAV), they can issue equity or convertible instruments to raise capital, which boosts holdings and may further enhance upside.

However, in downturns, when equity discounts widen and crypto prices fall, the feedback loop can reverse:

NAV declines.

Share prices fall.

Refinancing becomes more expensive.

Asset sales become necessary.

In this kind of bearish environment, even long-term investors with large Ether portfolios may decide to trim or exit positions to limit downside risk.

Opportunity cost and cleaner exposure

Today’s institutional investors have far more direct avenues for gaining Ether exposure than in earlier market cycles. Options include secure direct custody solutions, regulated spot exchange-traded funds (ETFs), staking-enabled products and sophisticated derivatives. These structures can reduce exposure to company-specific operational, execution or governance risks.

By contrast, investing through an equity wrapper around a leveraged crypto treasury strategy adds an extra layer of complexity and uncertainty. This includes exposure to management’s discretionary decisions, funding and refinancing strategies, governance structures and capital allocation priorities, which may diverge from pure asset performance.

Founders Fund is a venture firm historically focused on backing high-growth operating companies with scalable, technology-driven business models. A vehicle centered on a leveraged crypto balance sheet may not align seamlessly with its long-term portfolio strategy or risk preferences. Recent developments, including its complete exit from Ether treasury plays such as ETHZilla amid market pressures, underscore this selective approach to crypto exposure.