Robotics is advancing quickly. Machines already move goods across warehouses, inspect infrastructure, assist in hospitals, and operate in environments where human labor is limited or unsafe. The hardware is improving, the software is becoming more autonomous, and deployment costs are gradually declining.

But the way robots are organized economically still resembles an older industrial model.

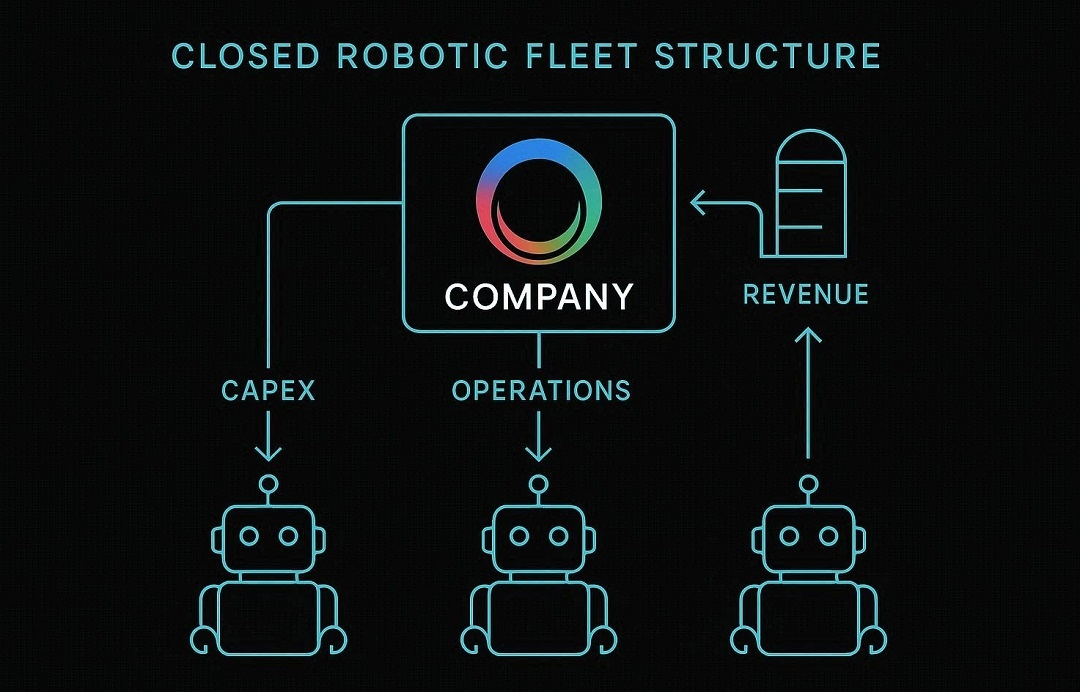

Most robotic systems today operate as closed fleets. A company raises capital, purchases hardware, manages operations internally, and signs service contracts directly with customers. The robots themselves remain embedded inside this vertically integrated structure. Capital, infrastructure, and revenue flow through the same institutional channel.

At first glance, this model appears efficient. It allows companies to maintain control over their machines, ensure operational reliability, and manage risk centrally. Yet as robotics begins to scale across industries and geographies, the limitations of this architecture become more visible.

Closed fleets concentrate participation.

Only organizations capable of raising large amounts of capital can deploy significant robotic infrastructure. Access to automation therefore expands at the pace of institutional financing rather than the pace of global demand. Even when there is clear need for robotic labor, deployment remains constrained by ownership structures.

This creates a structural mismatch.

Demand for robotic services is geographically distributed and highly diverse. Infrastructure inspection in one region, logistics support in another, environmental monitoring elsewhere. But the fleets capable of fulfilling these tasks are controlled by a small number of operators managing proprietary systems.

Instead of a network, robotics behaves like a collection of isolated silos.

Each fleet maintains its own operational stack. Each operator negotiates contracts independently. Performance data remains private, and coordination between fleets rarely occurs. The machines may be technologically advanced, but the economic layer organizing them remains fragmented.

Other industries have already faced similar limitations.

Ride-sharing networks, distributed computing platforms, and open digital marketplaces all emerged from the realization that coordination can be more efficient when infrastructure is shared rather than vertically controlled. When participation expands beyond a single operator, the system evolves from an isolated service provider into a network.

Robotics may be approaching the same transition.

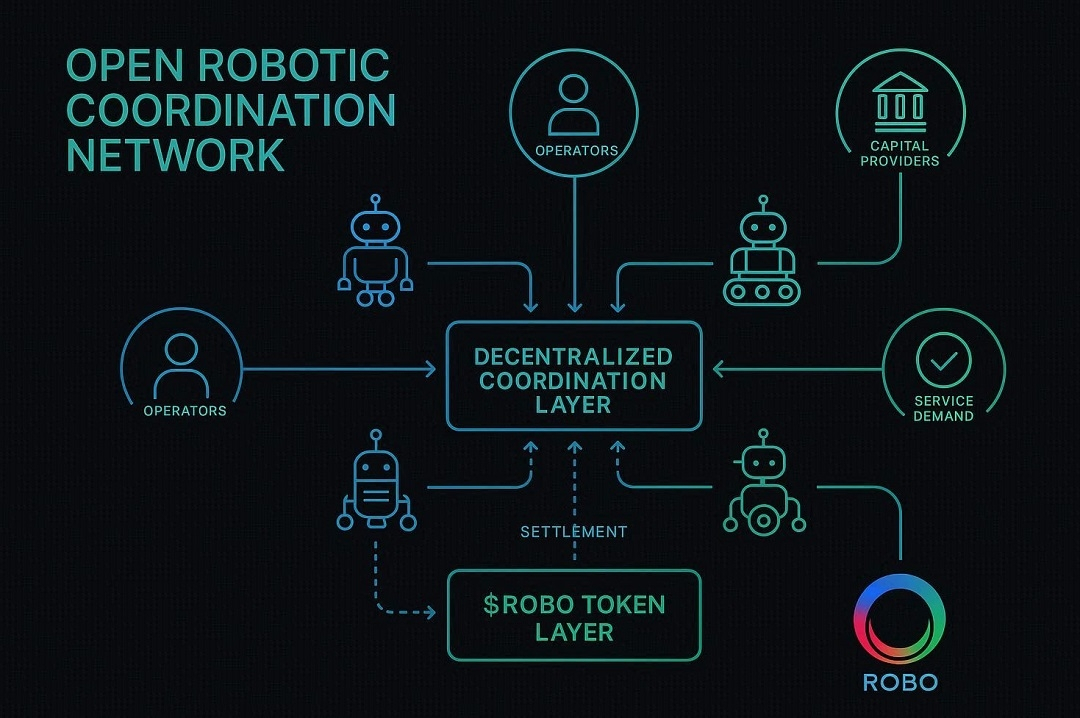

An open coordination layer would allow robots, operators, capital providers, and task demand to interact within a shared framework rather than through isolated corporate structures. Instead of every deployment requiring a new institutional fleet, machines could register identity, verify completed work, and settle payments through common infrastructure.

This is the architectural direction Fabric Foundation is attempting to formalize.

Rather than replacing hardware operators, Fabric proposes a coordination layer where robotic activity can be registered, verified, and economically settled onchain. Identity, task validation, and compensation become standardized processes rather than proprietary internal mechanisms.

Within this structure, $ROBO operates as the network asset supporting participation. Robots can register identity, verified tasks can trigger settlement, and contributors coordinating infrastructure can stake and interact within the same system.

The shift may sound subtle, but it represents a fundamental change in how robotic economies scale.

Closed fleets optimize for control.

Open coordination layers optimize for participation.

Robotics does not scale through fleets.

It scales through networks capable of coordinating machines, capital, and demand simultaneously.

If automation is going to expand across industries facing persistent labor gaps, the limiting factor may not be the capability of robots themselves. It may be the architecture that determines who can deploy them, who can access them, and how their work is economically coordinated.

Robotics does not only require better machines.

It may require a new coordination layer capable of connecting them.

@Fabric Foundation $ROBO #ROBO #robo