1. Introduction: Moving Beyond Financial Intuition

In the contemporary financial landscape, investors are often paralyzed by a "buffet of options" that ranges from foundational assets to high-complexity structured products. For the serious professional, the primary obstacle is rarely a lack of opportunity; rather, it is the absence of a formal decision-making architecture. In a world characterized by information density, relying on financial intuition—responding to headlines or "gut feelings"—is a recipe for structural failure.

The investment industry frequently obscures its inner workings behind a veil of jargon and complex modeling, often to maintain an air of exclusivity. As a strategist, my objective is to demystify nine core investment models, providing you with the tools to transition from reactive participant to a systematic architect of your own wealth. We must begin with a foundational truth: before a single dollar is allocated to a tactic, one must first master the strategic mandate.

2. The Strategic Mandate: Systems vs. Speculation

A strategy is not a reaction to the market’s daily fluctuations; it is a rigid system of governance. It consists of a predefined set of rules, criteria, and habits that dictate the deployment of capital. Without this framework, you are not "investing"—you are betting.

The mandate of a true strategist is to replace improvisation with planning. While betting relies on the whims of fortune, investing is a calculated exchange between risk and return. I must be clear: there is no legitimate strategy that offers high returns with negligible risk; such claims are narratives, not financial realities. To mitigate what I call the "cost of ingenuity"—the price paid for being unprepared—knowledge must be your primary acquisition.

"An investment in knowledge always pays the best interest." — Benjamin Franklin, 1758

This perspective underscores that a framework’s purpose is not to predict an unpredictable future, but to serve as a structural defense against the twin emotional extremes of panic and euphoria. By establishing your rules in advance, you ensure that your behavior remains disciplined even when the market is not.

3. The Efficiency of Inaction: Passive Investment Models

For the non-specialist professional, the strategic mandate is often "doing less." Passive models operate on the empirical reality that attempting to "outsmart" the collective market frequently results in higher costs and lower net returns.

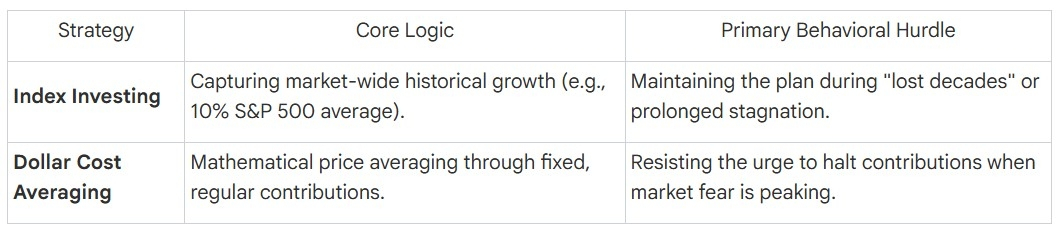

Index Investing (Passive): This model rejects the search for individual "winners" in favor of capturing the growth of the entire market via Index Funds or ETFs. The logic is grounded in history: since 1926, the S&P 500 has delivered an average nominal annual return of approximately 10%, according to Ibbotson Associate data collected by Morningstar. Popularized by John Bogle and the "Boglehead" philosophy, this strategy posits that after accounting for fees and human error, most active managers fail to surpass the market average.

Dollar Cost Averaging (DCA): This strategy involves the systematic investment of a fixed sum at regular intervals. By maintaining a consistent contribution schedule, an investor mathematically acquires more units when prices are low and fewer when they are high. This solves the "timing" problem by removing the need for market prophecy.

4. The Alpha Pursuit: Analyzing Active Selection Strategies

The pursuit of "Alpha"—returns that exceed the market benchmark—requires a more aggressive strategic posture. These models demand higher criteria, more rigorous analysis, and extreme emotional fortitude.

Value Investing: Rooted in the principles of Benjamin Graham and Warren Buffett, this is the discipline of identifying market inefficiencies. The strategic goal is to purchase a "50-dollar bill for 30 dollars," targeting resilient companies whose stock prices have decoupled from their intrinsic value.

Growth Investing: This model prioritizes future potential over current valuation. Investors pay a premium for companies like Apple, Amazon, or Netflix, wagering that future earnings will justify current multiples. The inherent risk is that market expectations often outstrip operational reality.

Dividend Investing: This approach focuses on the creation of consistent cash flow by selecting companies that regularly distribute profits. While often more stable, particularly in low-interest environments, the total return may be more modest compared to growth-oriented models.

The "So What?" of Active Management As a strategist, I observe that the failure of these models is rarely due to their internal logic, but rather to the "investor gap." The 2023 Dalbar study, Quantitative Analysis of Investor Behavior, consistently demonstrates that the average investor underperforms the very markets they inhabit because they abandon their strategy at the point of maximum pessimism. John Maynard Keynes famously described the market as a game of "anticipating what the average market believes the average market will believe." Success requires the discipline to ignore the crowd's belief and adhere to the system's rules.

5. Structural Robustness: Modern Portfolio Theory and the Permanent Model

In 1952, Harry Markowitz introduced "Portfolio Selection" theory, now known as Modern Portfolio Theory (MPT). This shifted the strategic focus from individual asset performance to the correlation between assets. The "holy grail" of MPT is finding assets with an inverse relationship; if one falls while the other rises, the portfolio achieves diversification that reduces risk without necessarily eroding returns.

Modern strategies apply this through various structural lenses:

Fixed Income (Bonds): Traditionally the "ballast" of a portfolio. However, a strategist must remain wary: during the 2022–2023 period of aggressive interest rate hikes in the US and Europe, we saw a rare "correlation break" where both stocks and bonds fell simultaneously, proving that no counterweight is infallible.

REITs (Real Estate Investment Trusts): These provide liquid exposure to real estate, though they carry a "double exposure" to both property cycles and equity market volatility.

Momentum Investing: This is a trend-following mandate, buying assets that are already rising under the hypothesis that trends persist longer than the average investor expects.

The most resilient application of MPT is the Permanent Portfolio, designed by Harry Browne in 1981. It utilizes a strict 25/25/25/25 split to ensure the portfolio survives regardless of the economic climate:

Stocks (25%): Deployed to capture gains during periods of Economic Growth.

Long-term Bonds (25%): Included to provide protection and appreciation during Deflation.

Gold (25%): Utilized as a hard-asset hedge against Inflation.

Cash (25%): Maintained as a liquidity buffer and stabilizer for periods of Recession.

The Permanent Portfolio is not designed to "win" during a bull market; its mandate is to be the strategy that survives the worst-case scenario.

6. The Myth of the Perfect Strategy: Historical Context and Reality

Strategy is a tool for specific conditions, not a universal panacea. History provides a sobering look at the "failure modes" of even the most respected frameworks:

Indexing's "Lost Decade": Between 2000 and 2010, the S&P 500 yielded near-zero returns, testing the resolve of passive investors for ten straight years.

Value's Stagnation: From 2010 to 2020, Value Investing significantly underperformed as the market entered a period of "tech-growth" dominance that ignored traditional valuation metrics.

The Permanent Portfolio's Yield Crisis: During the era of zero-interest rates, the cash and bond portions of the model provided no yield, leading to frustratingly flat performance.

The strategic takeaway is this: the goal is not to find a "perfect" strategy—it does not exist. The goal is to select the strategy whose specific failure mode you are psychologically equipped to tolerate.

7. Strategic Conclusion: Navigating Uncertainty as a Constant

Ultimately, the technical mechanics of these nine strategies are secondary to your personal psychology. The market is not a problem to be "solved"; it is a landscape of perpetual uncertainty. As we navigate "strange times" characterized by shifting interest rate regimes and geopolitical volatility, your most robust defense is not a complex algorithm, but informed conviction.

The ultimate question you must answer is: "What level of uncertainty can I tolerate without abandoning my plan?"

Understanding why you own an asset—knowing its purpose and the conditions under which it will fail—is what separates the informed investor from the crowd. As Francis Bacon wrote in 1597, "Knowledge is power." In the realm of investing, that power is the only thing that prevents you from being dragged away by the current of public opinion. Build your architecture of resilience on a foundation of systems, not stories.