In the context of the Crypto market being strongly divided between institutional money and Crypto users, the Privacy Asset segment is emerging as an independent defensive infrastructure layer away from the Yield cycle and speculation. The rise of Privacy, as well as the technological shift from traditional Mixer models to Privacy-as-a-layer based on ZK and FHE, demonstrates why privacy is gradually becoming a core infrastructure component of DeFi.

Market Context

From 2024, the Crypto market enters a phase distinctly dominated by institutional money. The emergence and explosion of Spot Bitcoin ETFs have attracted a significant portion of large liquidity into legally compliant assets, with Bitcoin playing a central role. Bitcoin Dominance has remained above 50% for nearly two years – the highest level since 2018 – while CME has risen to become one of the leading global markets in Open Interest and Bitcoin futures volume.

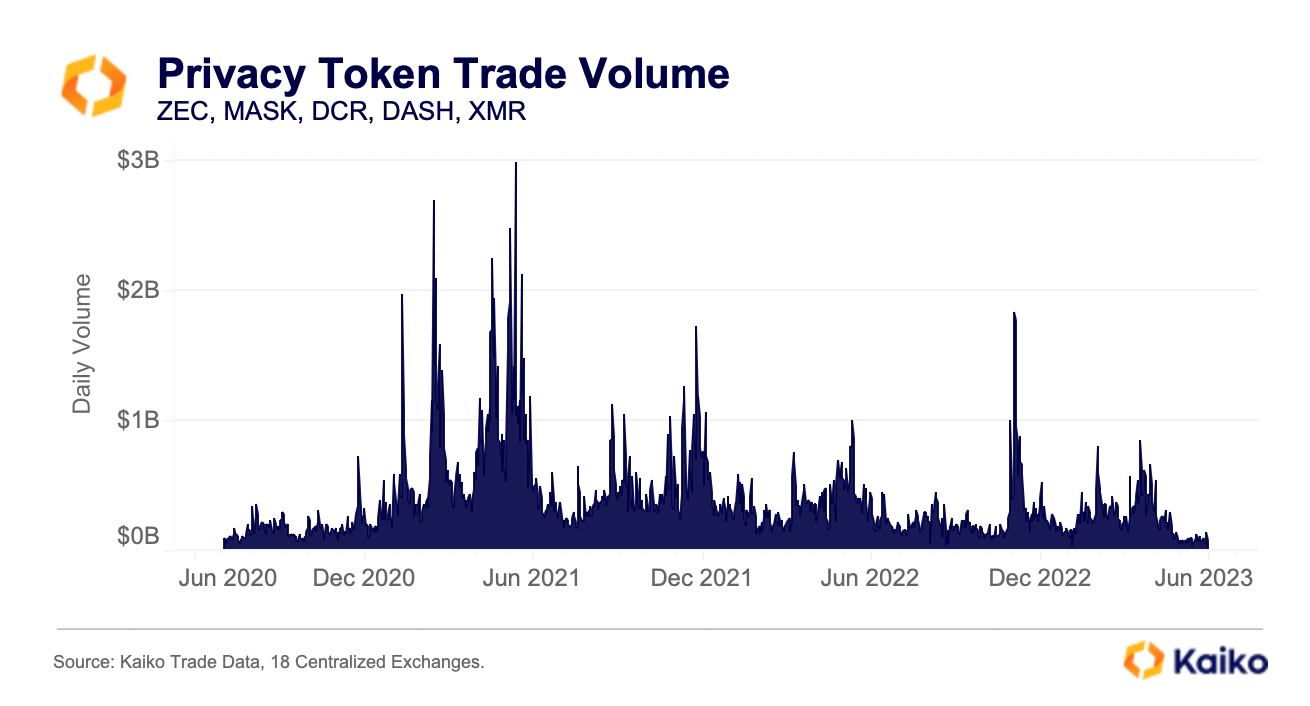

Alongside institutional money, there is a wave of tightening regulations globally. In the EU, MiCA and TFR directly eliminate Privacy Coins from the registered exchange ecosystem, leading to Monero being Delisted from Binance and Kraken for EEA users. In the US, although not officially banned, AML requirements from FinCEN and OFAC exert equivalent pressure, causing major platforms to avoid or impose strong restrictions on Privacy Assets. By 2025, 73 exchanges had Delisted at least one Privacy Coin, reducing this sector's daily transaction volume by hundreds of millions of USD.

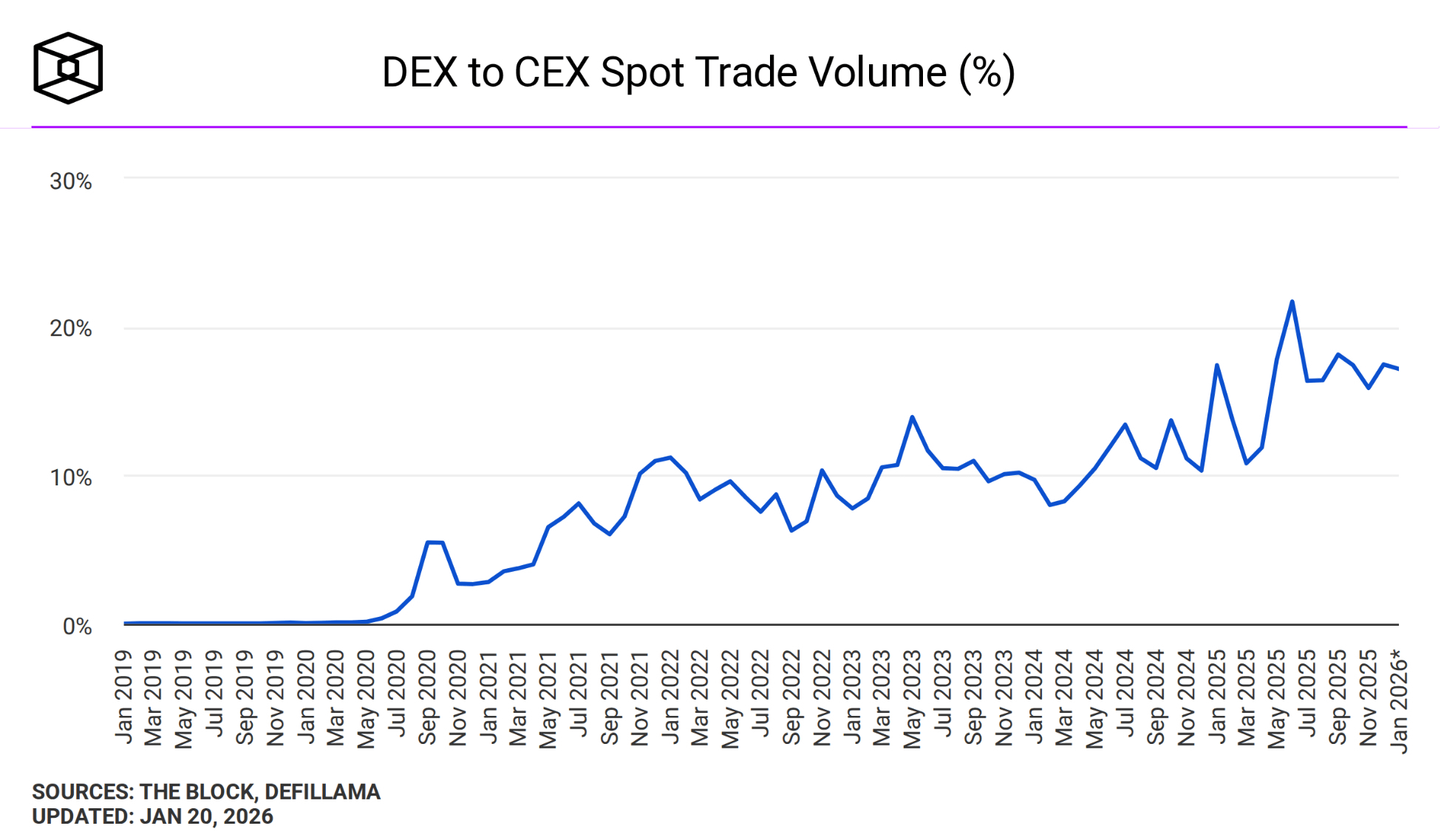

Meanwhile, Crypto-native users continue to shift towards decentralized infrastructure. The ratio of DEX/CEX and derivative volume on DEX has reached record highs, with Bitcoin and Ethereum reserves on CEX continually decreasing, reflecting a prolonged loss of confidence in centralized custody models. The result is an increasingly clear polarization: institutional capital concentrated in regulated channels, while native Crypto capital continues to seek sovereignty and resistance to control on Onchain, creating a long-term binary state of the market.

Privacy Narrative Analysis

In the late 2025 timeframe, the security segment in the Crypto market has increasingly demonstrated its independence from the rest of the ecosystem. Privacy assets no longer simply move in sync with Bitcoin or Altcoins during Bull phases but begin to form their own direction, reflecting distinctly different internal dynamics.

The current context is shaped by two forces: institutional money flowing heavily into regulated channels and the relentless expansion of financial oversight. As users move activities Onchain at a larger scale than ever, the demand for discreet financial security tools becomes a natural response. The Onchain activity of security protocols has reached historical highs, even surpassing many other areas that are heavily focused on Yield Farming or Staking.

Notably, societal demand for financial privacy is increasing according to a distinctly counter-cyclical model: the more legal constraints and oversight, the greater the demand for security becomes. In fact, the very strict legal frameworks in major jurisdictions – designed to control – are indirectly reinforcing the long-standing argument for Privacy by creating structural tension between Traceability and the need for personal autonomy.

Q1 2025 data shows Privacy Coins processed a total of $258 billion in transaction volume, accounting for about 12% of the total global Crypto transaction Volume, reinforcing the view that this segment currently operates as a parallel ecosystem based on actual use rather than speculation dependent on the overall cycle.

Security in DeFi: From Mixers to Privacy-as-a-Layer

Although the Market Cap is still small compared to the entire industry, Privacy continues to play a strategic role as a structural defense tool in DeFi, entirely independent of Yield cycles and institutional participation.

The total TVL of security protocols reached $1.34 billion in November 2025 – a new ATH, surpassing the 2021 peak without any supportive institutional capital. This figure even exceeds the total TVL of the entire Onchain insurance category, a field often driven by clear Incentives. Tornado Cash – still under OFAC sanctions – accounts for over 90% of TVL (approximately $1.22 billion). The slow but steady Deposit accumulation since 2023 shows that the demand for direct Onchain anonymity remains persistent despite the adverse legal environment.

The new generation of protocols like Railgun, Nocturne, Zama, Aleo, and Nillion are leading the shift from the classic Mixer model to Privacy-as-a-layer, utilizing FHE, Advanced ZK Proofs, and Cross-chain Modularity. Security is gradually becoming an integrated foundational service seamlessly embedded into existing Stacks rather than a standalone product heavily reliant on Mixing mechanisms. The ecosystem remains small in Volume and Adoption but is becoming increasingly coherent in technical terms: low visibility, few clear Incentives, fully focused on true Onchain sovereignty.

The Growth of Privacy Coins Previously.

The performance of Privacy Coins always follows a distinct repeating pattern: briefly appearing at the end of each major Bull Market, then quickly fading as liquidity shifts to new Narratives, specifically as follows:

In 2017: The narrative of 'anonymous digital cash' dominated. Zcash (ZEC), Monero (XMR), and Dash (DASH) significantly outperformed the broader market due to the promise of completely untraceable transactions – something Bitcoin only provided at a pseudonymous level.

In 2021: The Privacy trend gradually faded as capital flowed heavily into DeFi and NFTs on Ethereum. The correlation of Privacy Coins with Bitcoin increased, technical innovation slowed, and the segment became overshadowed.

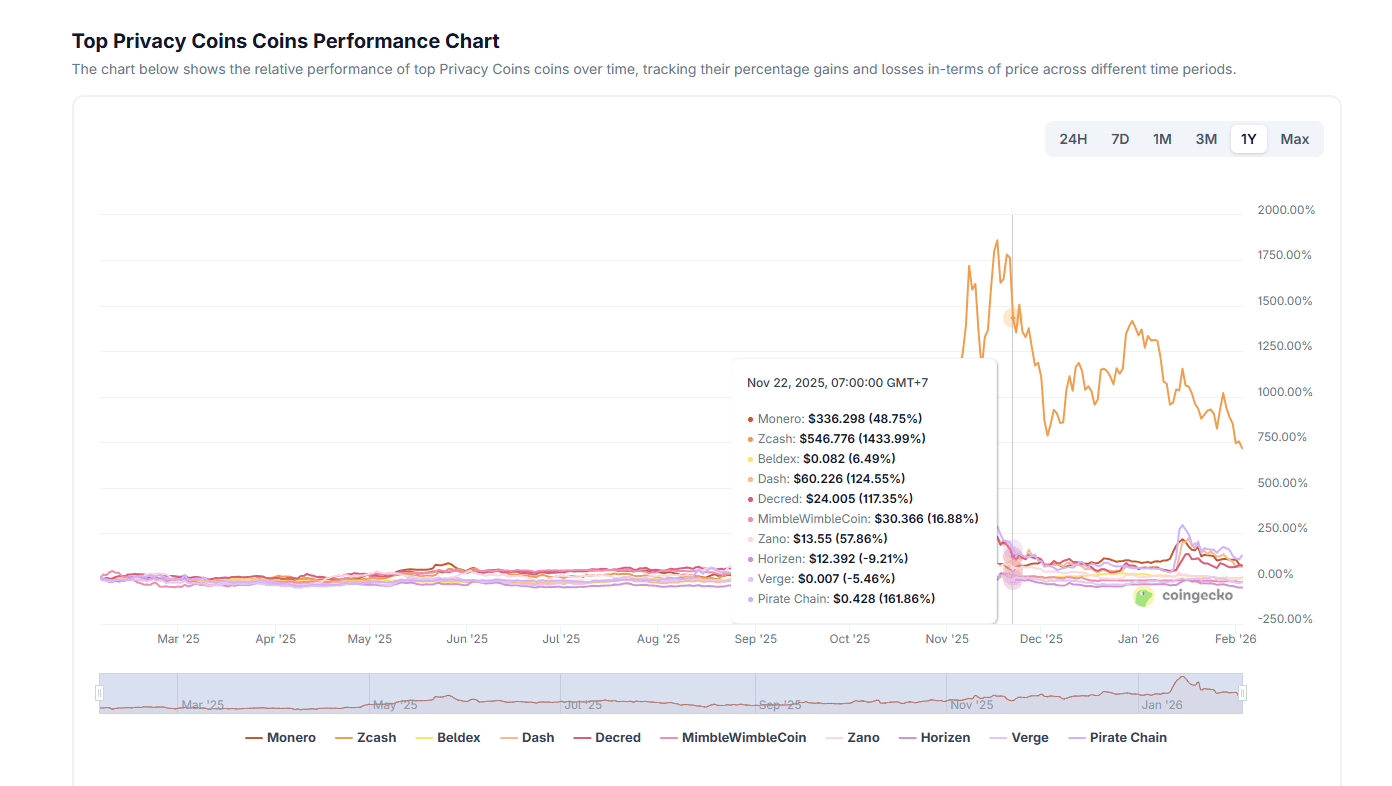

In 2025: The theme of security resurfaces strongly in the context of increased financial oversight and stricter regulations than ever before. Zcash stands out with clear Outperformance compared to Bitcoin since the beginning of the year, while Monero and Dash also record significant positive performance.

The explosion of Zcash in 2025 largely stems from its unique hybrid design: not all transactions are Shielded. The parallel existence of transparent and Shielded addresses allows regulated exchanges to easily maintain listings of ZEC, while Monero, with complete opacity, is often systematically Delisted due to incompatibility with KYC/AML requirements. As a result, ZEC has more stable liquidity on major platforms like Coinbase and Kraken, allowing investors to access privacy without fully abandoning the compliance environment.

Nevertheless, history shows that 'Privacy Seasons' have never lasted long. The Outperformance phases of ZEC, XMR, or DASH compared to BTC/ETH are often limited to a few weeks to a few months before sharply reversing as liquidity shifts direction. The long-term relative performance chart always displays the same Pattern: a brief Spike followed by a prolonged Sideway phase or clear Underperformance.

Specific data from Q1 2025 shows that privacy transactions account for 11.4% of the total Crypto transactions in the industry (up from 9.7% in 2024). In February 2025, the total transaction volume of the segment reached $8.7 billion, a 15% increase compared to the same period last year. Monero continues to hold a pillar position with 58% of Privacy Market Cap, Zcash 21%, Dash 10%. Monero remains the core reference due to its ability to withstand legal pressures and rare systematic Delistings. The surge in 2025 still follows this familiar Pattern: strong acceleration in a tense legal environment, yet still too new and too concentrated to be considered a sustainable regime change.

What Will the Future of Privacy Look Like?

Legal implementation

The implementation of legal frameworks in the coming years will be a key driver shaping the entire Privacy Asset segment. Many regulations are still in the process of refinement or have just been initially applied, but they can significantly impact access to privacy assets as well as how regulated platforms handle them.

In Europe, the specific implementation process of MiCA, TFR, and the AML package from 2026 onwards will determine the position of anonymity-enhancing Coins in the Regulated environment. The impact of these regulations on listings and how private transactions are conducted on exchanges will be factors that need to be closely monitored.

In the United States, FinCEN regulations on record-keeping and reporting of digital asset transactions may continue to tighten the use of security tools. Developments of the GENIUS Act, the proposed framework for Stablecoins and Non-KYC services, along with updates to IRS Form 1099-DA, are the most sensitive points. The greatest risk lies not only in the content of the text but in how these regulations are enforced by the market in practice.

The evolution of privacy

Technological innovation is gradually moving away from pure transaction mixing models, shifting towards integrating security directly at the Blockchain infrastructure layer. Early-stage FHE implementations like Zama or Nillion have enabled the execution of simple operations on encrypted data. The new generation of ZK systems like Halo2 or Plonk significantly reduce proof costs and expand the scope of security beyond Token transfers, into Governance, Settlement, and automation.

Cross-chain approaches like Railgun, Nocturne, or Anoma aim to maintain privacy consistency across both L1 and L2, despite the increasingly fragmented Blockchain architecture. Overall, these developments indicate a structural shift: privacy is gradually moving from an independent product to a core infrastructure component of the Blockchain ecosystem.

#Privacy