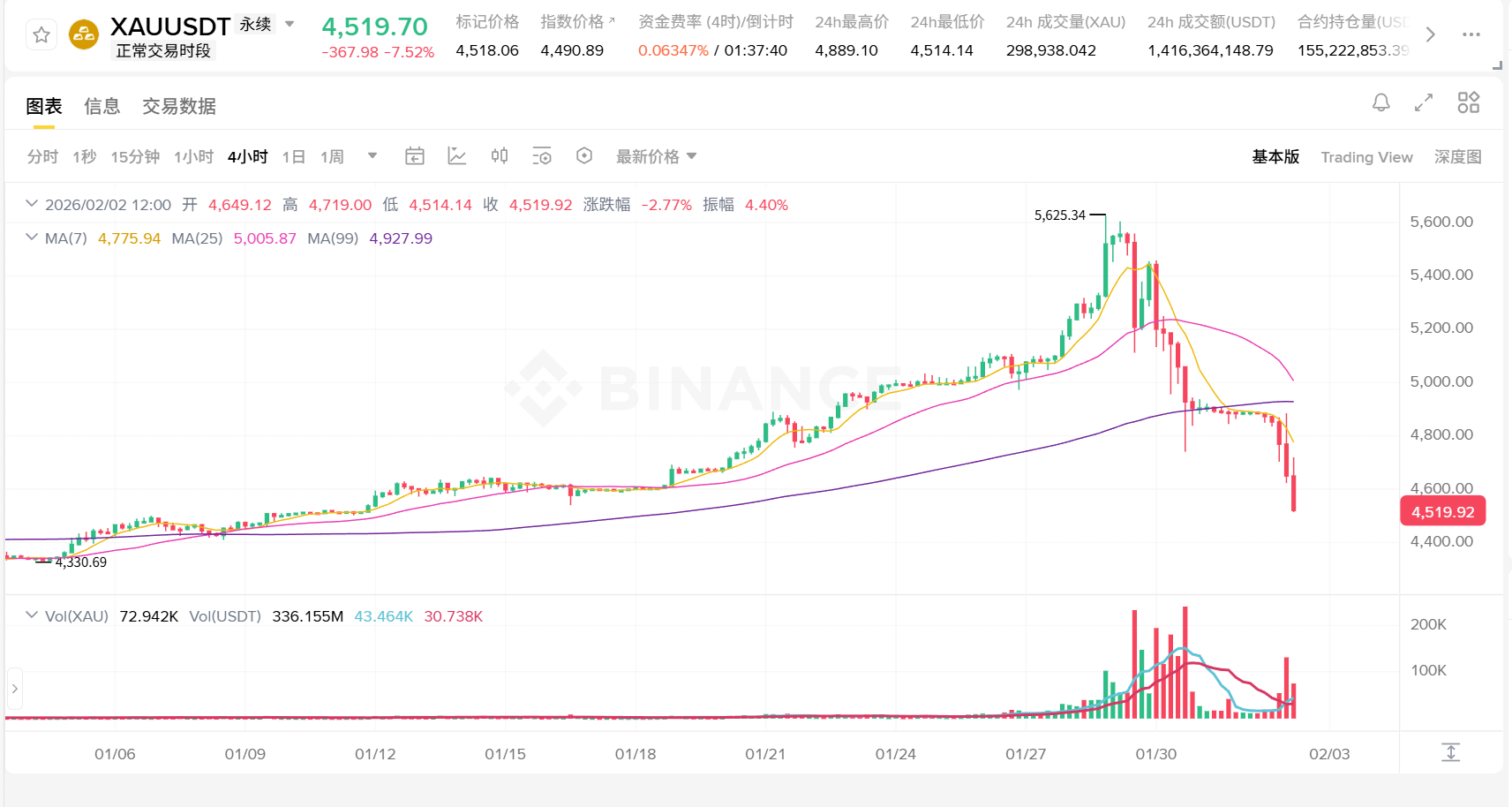

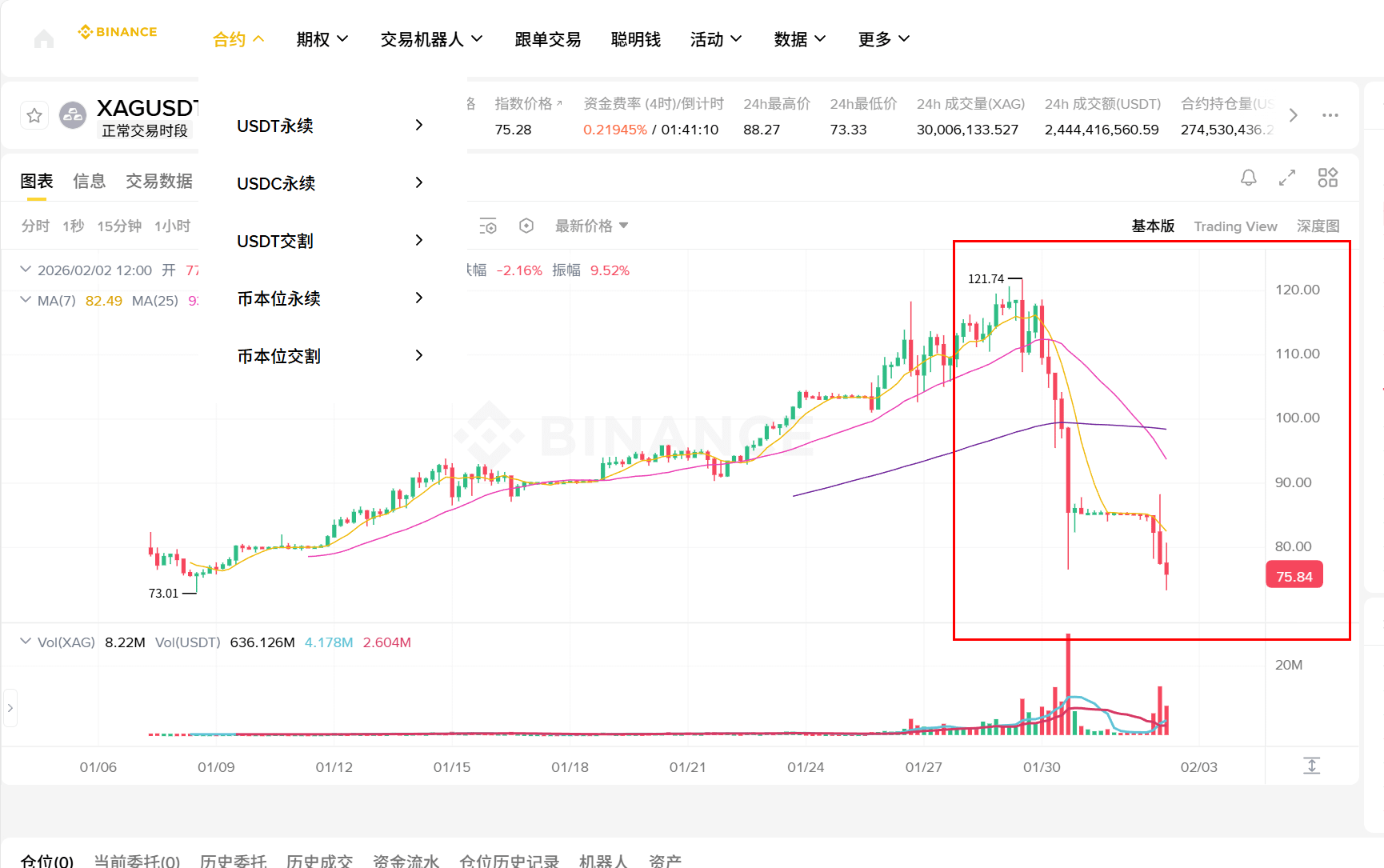

Silver rose for several days—then fell back to pre-liberation levels in just two days.

If you have been watching the market these past few days, you will likely feel a strong sense of disconnection: just a few days ago it was 'precious metals invincible, breaking new highs', and suddenly it turned into 'continuous large bearish candles, super waterfall'. However, I prefer to understand it as a typical complete cycle of 'narrative-driven → crowded trades → structural deleveraging'. What really causes the crash is often not the emotions, but the underlying rules of the international market.

Last Friday (1/30), precious metals experienced a historic drop, and the downward pressure continued on 2/2. The magnitude mentioned in the reports is very intuitive: spot gold fell by about 9% on 1/30 in a single day, called one of the largest single-day declines since 1983; silver was even more extreme, with the drop on 1/30 described as a 'record level' (about 27%) single-day plunge.

Why has it risen to such extremes: three forces have pushed precious metals to the 'consensus peak'.

The first force: uncertainty premium (safe haven) is being repriced.

$XAU What gold excels at is not 'rising every day', but when the market's certainty about the future decreases, it turns into an asset that 'packages and prices uncertainty'. Recent fluctuations around policy and fiscal expectations, as well as rising geopolitical and macro uncertainties, have made 'holding some gold as insurance' shift from a marginal choice to a mainstream allocation.

The second force: structural buying (especially from central banks) has provided a 'foundation' for the rise.

Many people only see gold prices hitting the peak, but they overlook the slower, steadier funds behind this trend: the increasing allocation tendencies of central banks and long-term investors. This won't determine daily price fluctuations, but it will determine 'whether anyone is there to catch it during a pullback'. Multiple institutions continue to emphasize the mid-term logic of gold after the pullback, with the core reason being that this structural demand remains.

The third force: the 'crowding' at the trading level makes the rise steeper.

When a narrative is smooth enough and prices are strong enough, funds shift from 'allocation' to 'chasing'. Gold often behaves like a 'financialized safe haven' in the final stages, while silver, due to its smaller market and greater volatility, is more easily treated as an 'amplifier' by leveraged funds. So you will see: within the same narrative, silver's fluctuations are always more exaggerated than gold's — it's not more 'certain', just more 'sensitive'.

Why did it crash again: it's not that the story changed, but that the 'funding chain' broke.

Many people instinctively ask: Does it mean there is suddenly no risk? Does it mean inflation is suddenly no longer a concern?

I think the closer truth is: the narrative is just a spark, but what truly triggers the liquidation is the structure of positions and changes in rules.

1) Catalyst: policy and personnel news trigger instant repricing of 'dollar/interest rate expectations'.

Around 1/30, the market's imagination of the US monetary policy path was forcibly pulled to the other side by a piece of news: Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve chairman was interpreted by many analysts as leaning towards a policy orientation of 'controlling inflation and a strong dollar', leading to a retreat of crowded long positions in precious metals.

You can understand it as: when the market feels that 'future real interest rates may be higher/ the dollar may be stronger', the appeal of non-yielding assets like gold will be repriced.

2) The real accelerator: margin adjustments trigger 'forced selling'

A more lethal blow comes from CME Group: in the margin requirement adjustments published on 1/30, the margin for gold-related contracts was raised from 6% to 8%, and for silver from 11% to 15% (with higher levels for different risk tiers).

What does this mean? It's simple: your position might not be wrong, but your margin could be insufficient. When margins suddenly increase, leveraged players either have to supplement funds immediately or can only liquidate positions; and liquidating will continue to drive prices down, triggering further margin calls — this is the classic 'forced liquidation chain'. This is why you see those seemingly 'irrational' large bearish candles: it's not emotions selling, but rules forcing you to sell.

3) Why is silver worse off: it is inherently more prone to 'waterfalls'.

$XAG Silver possesses both 'precious metal attributes' and 'industrial attributes', making the narrative more complex; but from a microstructural perspective, its market depth and liquidity are not as thick as gold's. Once it enters a deleveraging phase, it is easier to create a 'vacuum zone of continuous breaches of support, where fewer and fewer dare to catch the falling knife'.

This is also why you see the performance on the ETF side is equally extreme — iShares Silver Trust (SLV) closed at about $75.44 on 1/31, with an extreme single-day drop; gold ETFs also saw significant pullbacks.

This round of market movements provides the most important insight for ordinary people: don't just focus on 'right or wrong', but on 'can it withstand it'.

The recent extreme fluctuations in precious metals have amplified an old problem:

The market's extreme short-term movements are often not driven by fundamentals, but by the structure of positions.

When a 'crowded consensus' forms in the up phase, the down phase will transform into a 'reverse resonance of liquidity and leverage'. You may disagree with the market's direction, but you cannot ignore the market's mechanisms — especially the three aspects of margin, leverage, and liquidity, which determine whether the market will shift from a 'pullback' directly into a 'liquidation'.

I have always thought that the most brutal aspect of the market is: short-term extreme movements are often not driven by fundamentals, but by the structure of positions.

You can judge the macro direction, but as long as you are on the crowded side and using excessive leverage, you may be eliminated early by 'rules and liquidity'.

How to observe going forward: use three lights to judge whether 'the decline is a rebound or a reversal'

If you want to follow what's next, I suggest focusing on three things (there’s no need to guess positions every day):

The first light: the US dollar and real interest rate expectations.

As long as the market continues to trade on 'stronger dollar/higher real interest rates', it will be difficult for gold to return quickly to its previous one-sided tailwind.

The second light: whether margin and volatility continue to increase/spread.

Margin increases are a hard switch for deleveraging; if there are no further increases, the forced selling pressure may diminish.

The third light: whether there are 'buying signals' from structural buyers.

For example, whether long-term funds are returning to replenish in panic (in media and institutional views, some still emphasize the mid-term allocation value of gold).

As I write this, I feel that this wave is not a 'collapse of precious metal narratives', but rather a violent rebalancing that squeezes out the bubbles and cleans the positions: gold remains one of the core assets for hedging uncertainty, but silver, as an 'amplifier', reminds us — when you use leverage to embrace consensus, you often end up being bitten by that consensus.