On February 16, 2026, the (Special Preventive Measures Management Measures for Anti-Money Laundering) jointly released by the People's Bank of China, the Ministry of Foreign Affairs, the Ministry of Public Security, and other eight departments will officially take effect.

This time it is not that cash out has become 'more difficult', but that it is 'completely going to cool down'. Even ordinary individuals borrowing a card or companies handling vague accounts may directly face account freezes and asset locks.

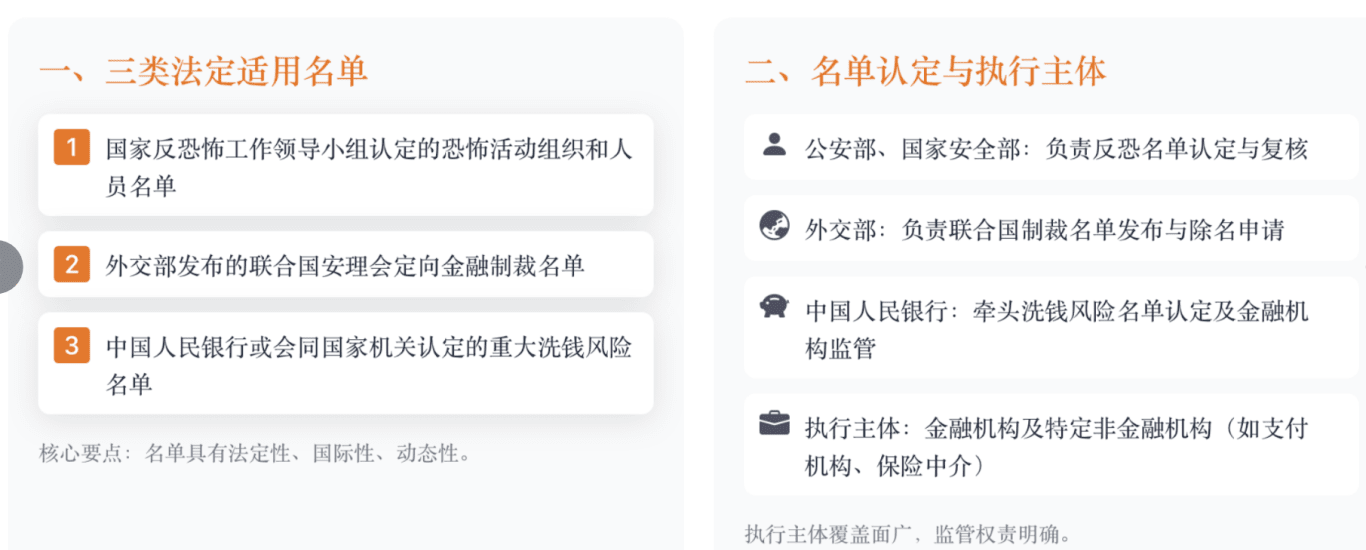

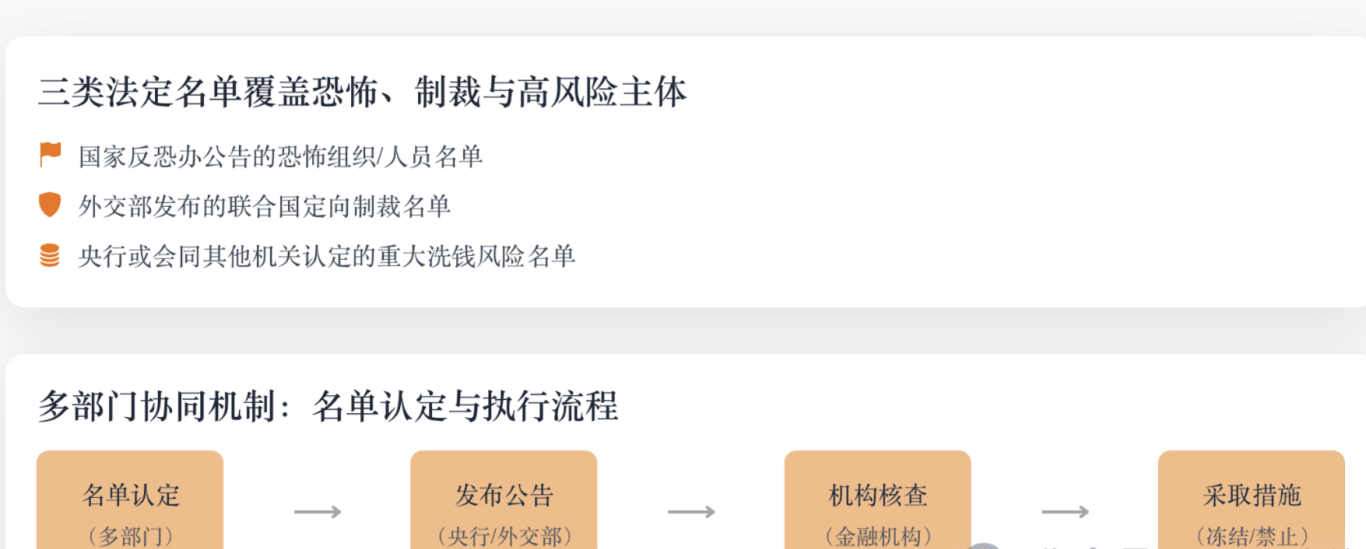

The most severe aspect of this new regulation is not the strengthening of reviews, but the formal establishment of a Chinese version of a three-tier anti-money laundering blacklist. Once you are on this blacklist, it is a direct kill, and the coverage ranges from institutions to individuals, with no one able to escape.

The first layer is executed by the national anti-terrorism working group. Once listed, all accounts and assets are directly frozen. Don’t even think about transferring or withdrawing cash.

What is even more hopeless is that this list has essentially no relief channels. The so-called 'application for review' is merely a formality. Even if you are wrongfully impacted, there is fundamentally no opportunity to prove your innocence.

The second layer is executed by the Ministry of Foreign Affairs. Those on the blacklist cannot move domestic funds, and cross-border transactions are directly suspended. Even if you have assets abroad, as long as they involve Chinese-funded institutions, they will be controlled.

Moreover, whether or not to remove a name from the blacklist is entirely dependent on UN resolutions; domestic regulatory statements do not count, equivalent to being blacklisted by the global financial system.

The third layer is executed by the central bank, covering subjects suspected of major money laundering both domestically and internationally, including underground currency dealers, over-the-counter transaction intermediaries, and high-risk cross-border trade enterprises.

The central bank seems to have administrative review and litigation relief channels, but in practice, proving one's innocence requires presenting complete, legal, and traceable transaction records and proof of the source of funds.

The underground currency dealers and over-the-counter cash transactions in the cryptocurrency realm cannot provide legal proofs and are essentially a life-and-death gamble.

Even more terrifying is that the enforcement rules of this blacklist are instant, penetrating, and collective punishment.

Financial institutions must not only check the clients themselves but also verify the transaction parties, agents, and organizations under indirect control. As long as any party is involved in the blacklist, all financial services must be stopped, and funds frozen, without prior notice.

You may think you are just transferring money to an ordinary merchant, but if the other party's upstream is an underground currency dealer, your account will still be frozen. If you only lent your bank card to a relative for a transaction, but your relative used your card to transfer money for a scoring group, your assets will be locked directly.

Want to prove you are a 'well-meaning third party'? You can, but it will take months or even years to provide evidence, and the threshold for evidence is absurdly high. Most people can only watch their accounts get frozen, with no way out.

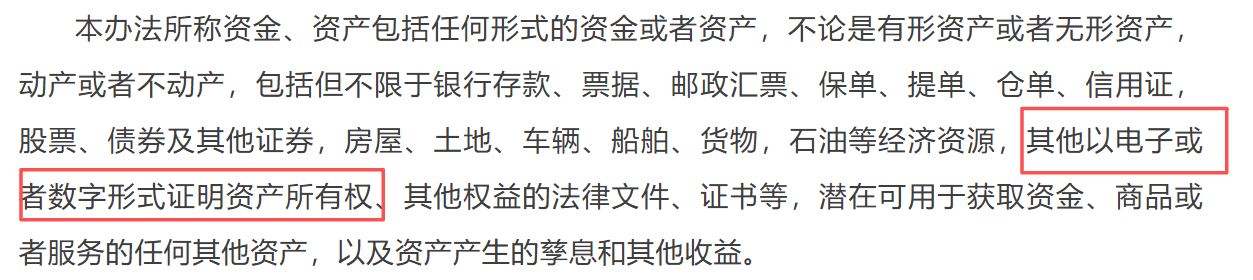

In the past, everyone thought 'virtual currency is not legal tender, so regulation doesn't apply,' but Article 29 of the new regulations clearly states: funds include assets ownership proven in electronic or digital form.

This statement directly incorporates virtual currencies into the full-process management of anti-money laundering and effectively sentences all gray inflows and outflows to death.

Starting from February 16, all mainstream methods of inflow and outflow in the cryptocurrency realm are high-risk minefields.

For example, if you are looking for an underground currency dealer to exchange fiat for USDT, the funds of the dealer are very likely tainted with proceeds from telecommunications fraud and online gambling. Once the dealer is blacklisted, your account will be immediately implicated.

For example, finding OTC stores in Hong Kong to exchange currency; recently, a college student in Shenzhen was scammed by this kind of part-time job, helping someone exchange USDT in Hong Kong for a fee, only to find that the upstream was a money laundering gang. Not only was their bank card frozen, but they were also charged with aiding and abetting.

Even so-called cash transactions are now under extreme scrutiny by banks. Frequent deposits and withdrawals of large amounts within 5 days without a fixed income will directly be marked as high risk.

Moreover, regulators have long understood the tricks of money laundering in virtual currencies, from 'card back to USDT' to 'virtual currency running scores', from fragmented transfers to cross-border capital shifts. All these small tricks have been incorporated into the bank's big data monitoring system.

Frequent small transfers within a short period, frequent transactions with unfamiliar accounts, and capital flows involving foreign encrypted asset merchants will trigger automatic alerts in the system, and financial institutions will directly take control measures, leaving no opportunity for explanation.

Some may ask: What if I accidentally get listed on the blacklist or my account gets frozen? Is there any solution?

As a lawyer, I can only say that the channels for remedy are absurdly narrow, and the distinctions between different levels are significant.

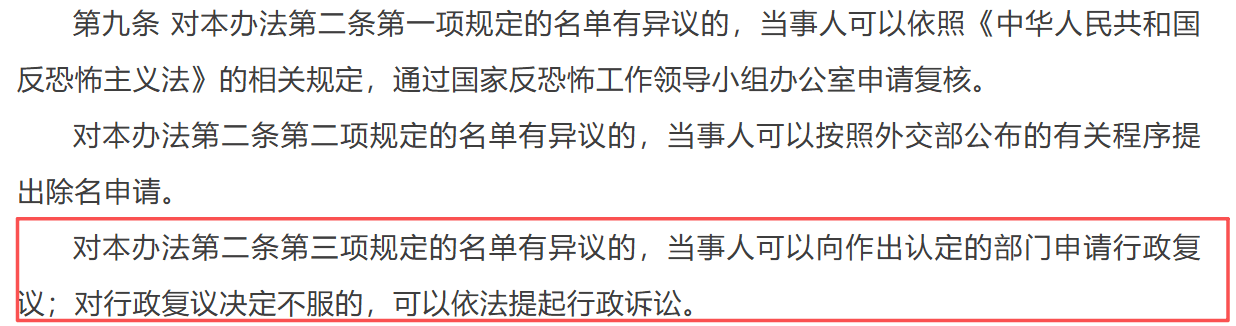

The anti-terrorism blacklist and UN controls directly abandon treatment. No lawyer can help you 'remove your name' from the blacklist. The so-called review and application are just procedural and cannot fundamentally change the outcome.

The central bank's high-risk list can go through administrative review or litigation, but you must be able to prove your innocence.

The key here is not 'you say you haven't laundered money,' but 'you can provide evidence that every transaction is legal'—for example, for the USDT you exchanged, you need to prove that the source of fiat currency is salary or investment, not unidentified funds; for the transfers you made, you need to prove that the trading counterpart is a legitimate entity, not involved in illegal activities.

However, the gray transactions in the cryptocurrency realm inherently lack legal proof, and at this step, basically no one can accomplish it.

Some people think, 'I don't deal with cryptocurrencies; I'm just an ordinary individual/business, so this new regulation has nothing to do with me.' This is a big mistake.

The new regulations clearly include 'any unit and individual' as subjects of anti-money laundering obligations. This means that if an ordinary person lends their bank card or ID card, even if it is just to earn a little money, once they are involved in a blacklist, they become an accomplice.

For enterprises engaged in cross-border trade and large transactions, if they do not conduct thorough reviews of their partners, once a partner is listed, the enterprise will be deemed an 'associated entity' with frozen funds and suspended operations becoming the norm.

Past lucky operations, starting from February 16, are now high-risk illegal activities with extremely high costs.

In fact, this new regulation clearly reveals the core trend of future financial supervision: full-process traceability, thorough review, and zero-tolerance penalties.

Money laundering activities have long overflowed from traditional financial institutions to non-financial institutions and the virtual asset field, and this new regulation is precisely aimed at this overflow.

In the future, all fund flows, whether fiat or virtual currency, whether online or offline, must have legitimate sources, clear directions, and traceable proof—non-compliant inflows and outflows are not 'becoming difficult,' but are 'completely dead.'

As a lawyer deeply involved in this field, based on new regulations and practical experience, I offer a few objective suggestions for individuals and enterprises.

For individuals: Do not lose big for small gains; guard your own accounts.

1. Do not lend your card or ID, even to close friends or relatives. Under the new regulations, once a borrowed account is involved in a blacklist, you become an accomplice, and all assets will be frozen. Attempting to 'clean up' is harder than reaching the sky.

2. Stay away from all gray inflow and outflow channels related to virtual currencies. Underground currency dealers, over-the-counter cash transactions, and part-time currency exchange in Hong Kong are all key targets of the new regulations. Touching them is stepping on a landmine, leading to asset freezing at best and criminal detention at worst.

3. If your account is frozen, do not operate blindly. Immediately seek professional lawyers in anti-money laundering and virtual currency fields to determine which blacklist you are implicated in and handle it accordingly. Never attempt to transfer assets, as this will only worsen the punishment.

For enterprises: ensure thorough review and do not step on the landmines of partners.

1. Establish a self-check ledger for the blacklist, especially for enterprises engaged in cross-border trade and large transactions. Regularly check partners through the central bank and FATF official websites. Once abnormalities are found, immediately terminate cooperation and report.

2. Leave a full trace of every transaction; the source, direction, and transaction contracts of every fund must be completely preserved. This is the only proof for future self-defense.

3. Do not touch any gray businesses related to virtual currencies. Even if a client requests to settle with virtual currency, refuse outright. Under the new regulations, providing payment settlement services for virtual currencies will be prosecuted directly under money laundering-related charges.

Many people say that this new regulation has made inflows and outflows more difficult, but in fact, it is not—it has simply eliminated all avenues for non-compliant inflows and outflows.

The essence of anti-money laundering has never been to restrict legal capital flows, but to block the dirty money and black funds hidden in the gray areas outside the financial system.

For ordinary people, this is a barrier to protect legal assets; for enterprises, this is the bottom line for compliant operations; and for the cryptocurrency realm, this is a complete reshuffle—those who only want to profit from trading cryptocurrencies and capital shifts will be gradually eliminated.

After February 16, do not harbor any illusions.

In this increasingly strict regulatory era, compliance is the only safe channel for inflow and outflow.