If 2020 was the year of the "DeFi Summer" casino, and 2022 was the year the house of cards collapsed, 2026 has emerged as the year DeFi finally disappeared. It didn’t vanish in the literal sense—Total Value Locked (TVL) is at all-time highs—but it has receded into the background, becoming the invisible operating system for a new global economy.

The narrative of "DeFi killing banks" is dead. Instead, a far more interesting reality has taken hold: DeFi is becoming the backend API for traditional finance (TradFi), while simultaneously evolving into the native currency of the "Machine Economy."

This article explores the unwritten reality of DeFi in 2026, moving beyond the tired tropes of yield farming to examine the three pillars defining this new era: The Rise of AI Financial Agents, The "Mullet" Strategy of Fintech, and the Paradox of Compliant Privacy.

I. The Rise of the Machine Economy: When the "Whale" is a Bot

For years, DeFi interfaces were designed for humans. They had flashy buttons, gamified staking rewards, and complex dashboards. In 2026, the most important user of DeFi protocols is no longer a human; it is an Autonomous Financial Agent (AFA).

The explosion of Large Language Models (LLMs) and agentic AI has created a layer of software that interacts with smart contracts far more efficiently than any human trader.

The Death of the "User Interface": Top-tier protocols are seeing a decline in direct website traffic but a massive spike in direct contract interaction. Why? Because users aren't connecting their wallets to Uniswap anymore. They are telling their personal AI assistant, "Optimize my savings for low-risk yield," and the AI is executing a complex strategy across Aave, Curve, and Morpho Blue in seconds, rebalancing automatically as rates change.

JIT (Just-in-Time) Liquidity: Liquidity is no longer static. AI agents now practice "Just-in-Time" liquidity provision, moving capital into a pool the exact second a trade is requested and withdrawing it immediately after to avoid exposure. This has made markets hyper-efficient but brutally competitive for human market makers.

The Unwritten Insight: We are witnessing the birth of B2A (Business-to-Agent) DeFi. Protocols are now optimizing their code not for human readability, but for AI composability—simplifying logic so that autonomous agents can audit, trust, and utilize them without human intervention.

II. The "Mullet" Strategy: Fintech in the Front, DeFi in the Back

The mass adoption of DeFi didn't come from people buying MetaMask wallets; it came from people using their regular banking apps without realizing what was powering them. This is the "Mullet" Strategy: a clean, regulated, Web2 "business" interface in the front, with a wild, permissionless Web3 party in the back.

Neobanks as Gateways: In 2026, major neobanks offer "High Yield Savings" accounts offering 6-8% APY. The user sees a standard bank interface. Behind the curtain, the bank is converting user deposits into USDC and lending them into over-collateralized DeFi protocols or Real World Asset (RWA) pools comprising tokenized U.S. Treasury bills.

The Gas Fee Abstraction: The biggest barrier to entry—gas fees—has been solved not by lower costs, but by subsidy. Fintech companies now pay the gas fees on behalf of their users (using Paymasters on Layer 2 networks like Optimism or Base) as a customer acquisition cost (CAC). The user never sees "ETH" or "Gas"; they just see a transaction fee of $0.00.

The Unwritten Insight: "DeFi" is becoming a dirty word in marketing, even as it becomes the standard in engineering. Companies tout "Blockchain-based settlement" or "Programmable Capital," stripping away the crypto-anarchist branding to sell the efficiency of the technology to institutional boards.

III. The RWA Reality Check: Boring is the New Bullish

The hype cycle of 2024 promised that we would be tokenizing residential houses and selling them in fractions to retail investors. That failed because of liquidity issues (selling 1/100th of a house is hard when no one wants the other 99/100ths).

In 2026, Real World Assets (RWA) have succeeded by being incredibly boring.

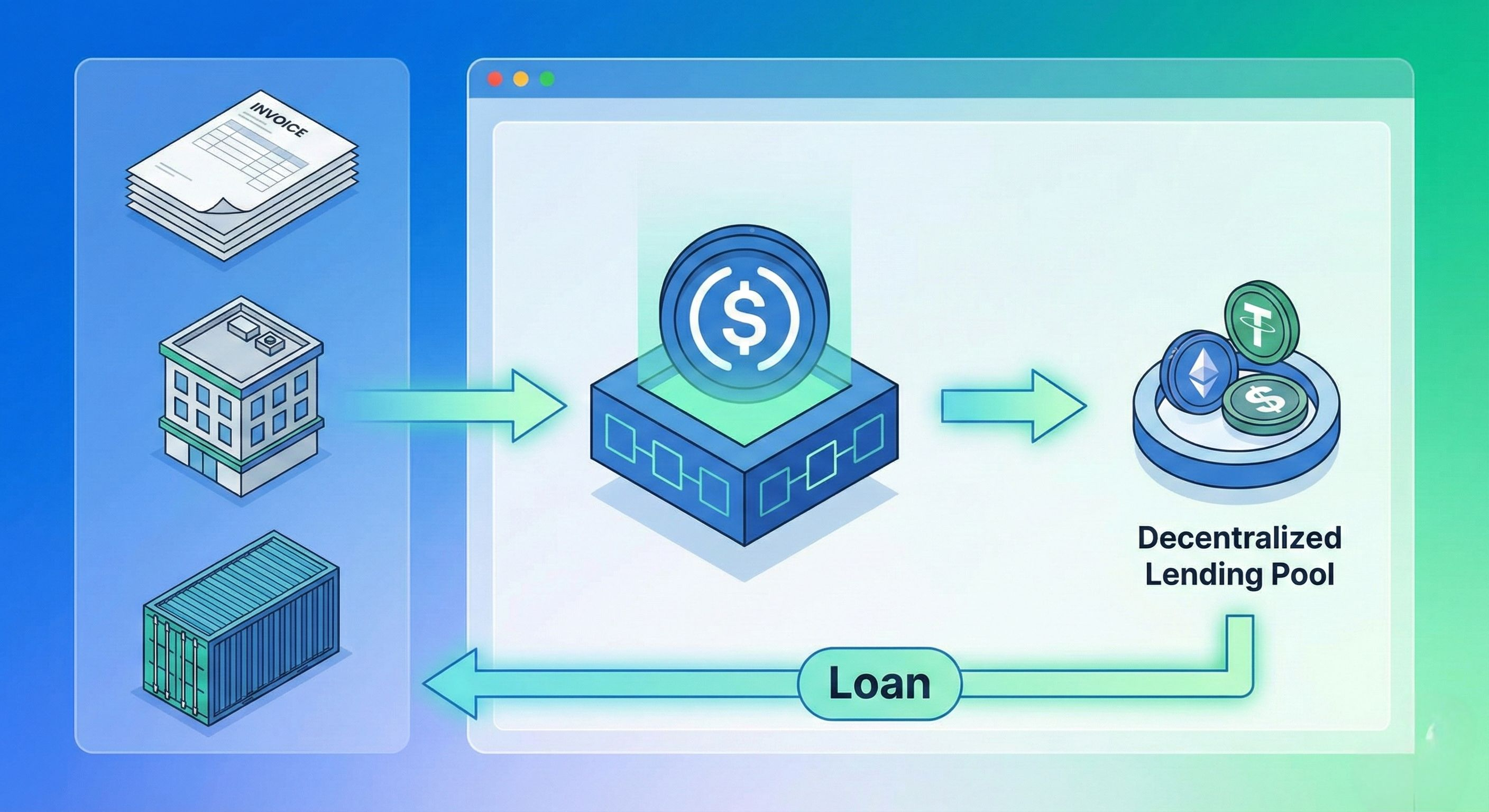

The Collateral Shift: The most valuable collateral in DeFi is no longer volatile ETH or BTC; it is tokenized private credit and corporate debt. Small businesses in emerging markets are financing their inventory by collateralizing their invoices on-chain. Global liquidity providers (often searching for yield in a low-interest-rate fiat world) fund these loans instantly.

The "On-Chain S&P 500": Instead of synthetic stocks, we now see compliant, tokenized wrappers of major ETFs used as collateral. You can now borrow stablecoins against your tokenized S&P 500 portfolio without selling the asset, unlocking liquidity while maintaining market exposure—all settled in seconds without a 3-day bank clearing period.

IV. The Compliance Paradox: How Privacy Saved Regulation

For years, regulators viewed "privacy" (like mixers) as a tool for crime. In 2026, the narrative has flipped: Zero-Knowledge (ZK) Proofs are now the primary tool for regulatory compliance.

Proving Without Revealing: Institutional players needed a way to use DeFi without doxxing their entire trade history to competitors. ZK-Identity layers now allow a hedge fund to prove: "I am an accredited U.S. investor, and I am not on a sanctions list," without revealing "I am BlackRock, and I am buying $50M of this asset."

Permissioned Pools (DeFi 3.0): We now see a bifurcated liquidity landscape. There are "Dark Pools" for institutions (compliant, KYC-gated via ZK proofs) and "Wild Pools" for permissionless retail. Interestingly, the Dark Pools often have lower yields but massive liquidity, while Wild Pools remain the frontier for high-risk speculation.

Conclusion: The End of "Crypto"

By 2026, the distinction between "The Crypto Economy" and "The Economy" has begun to blur. DeFi has stopped trying to burn down the banks and has instead started selling them better plumbing.

The future isn't a single "Super App" that does everything. It is a mesh of thousands of purpose-built protocols, managed by AI agents, settled on Layer 2 blockchains, and accessed through the banking apps we already use. The revolution wasn't televised; it was integrated.

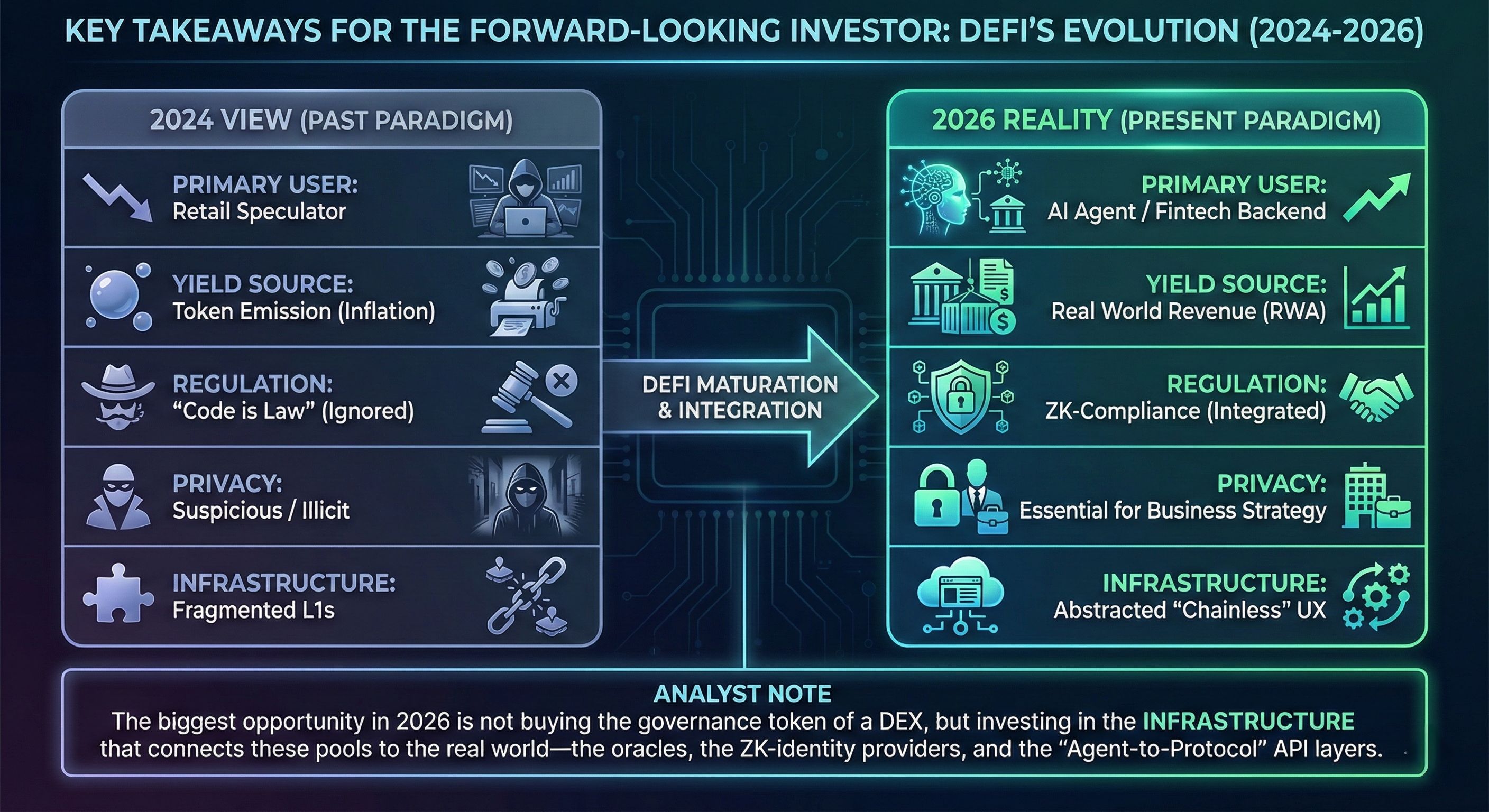

Key Takeaways for the Forward-Looking Investor