MicroStrategy, as one of the publicly listed companies holding the most Bitcoin globally, is closely tied to the price of Bitcoin. With the market hitting $60,000 in early February, a key question arose: If the price falls to $50,000, will MicroStrategy face liquidation risk?

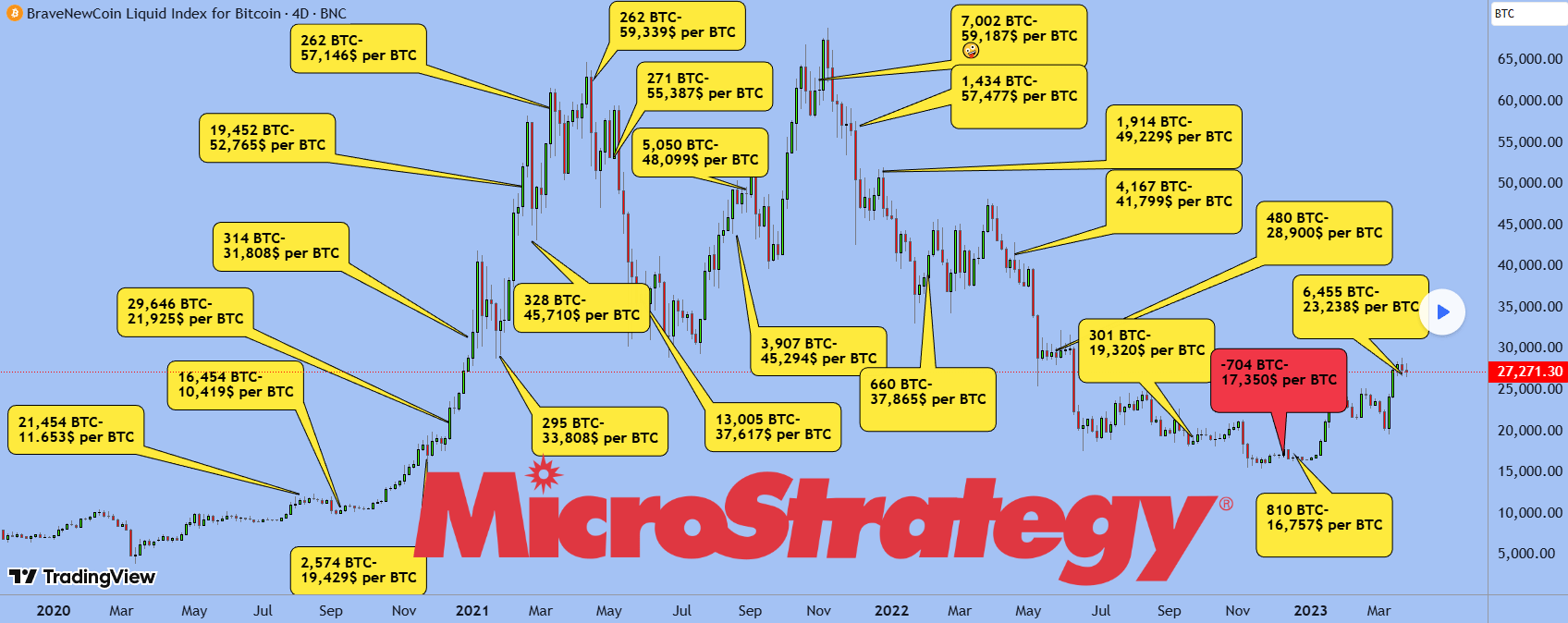

Starting from August 2020, under the leadership of CEO Michael Saylor, MicroStrategy began to aggressively buy Bitcoin as its primary reserve asset. The company raised funds to purchase Bitcoin through various means, including issuing convertible bonds, equity financing, and utilizing operating cash flow. As of February, MicroStrategy's holdings exceeded 710,000 Bitcoins! The average holding cost is approximately $76,000!

Previously, it was rumored that MicroStrategy's 'leveraged' accumulation of Bitcoin could trigger liquidation after its debt potentially falls below 50,000 after $BTC . However, after looking through a lot of data, it turns out to be nonsense...

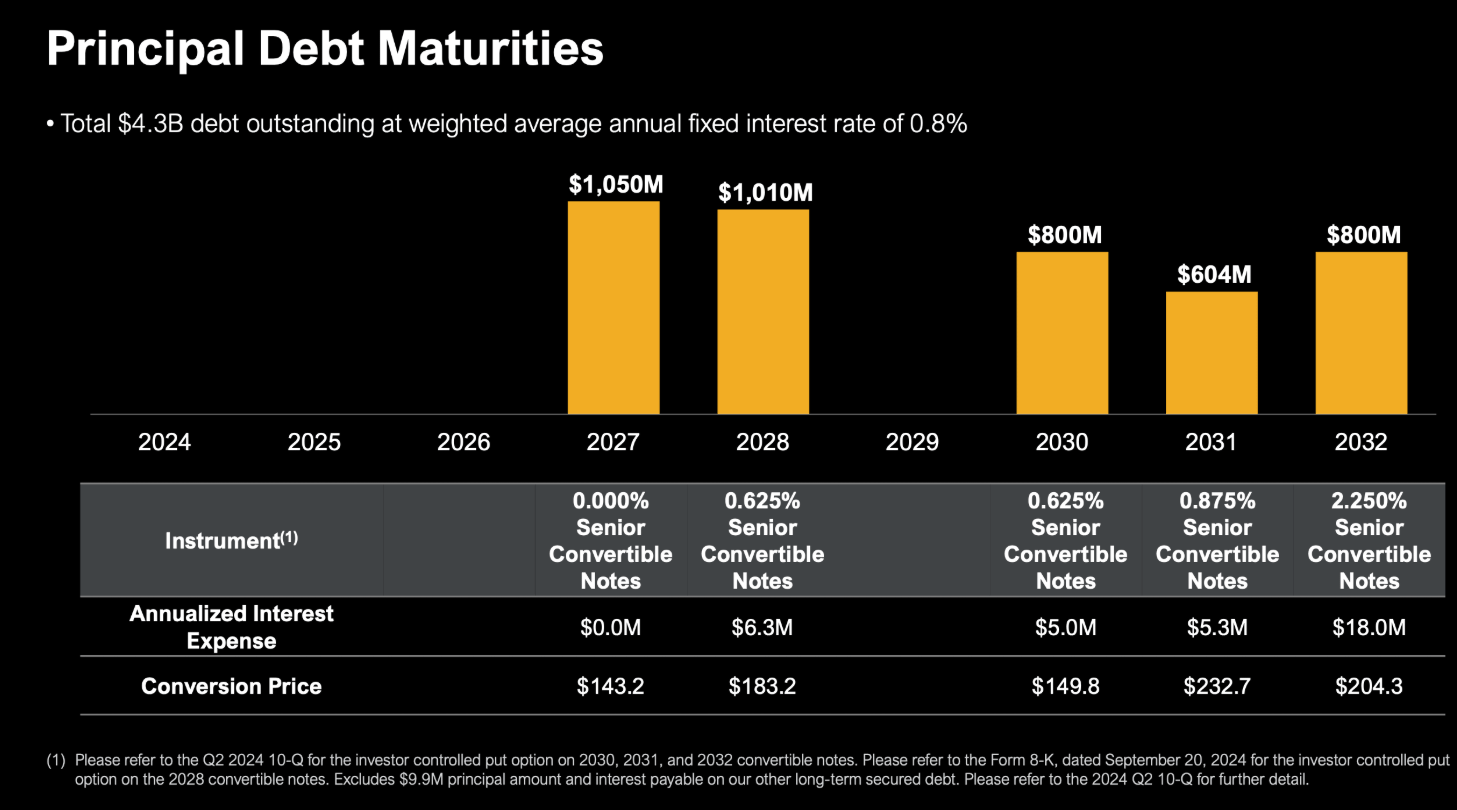

MicroStrategy's current debt scale is roughly over 8 billion dollars, and most of this debt is unsecured convertible preferred notes! This means creditors do not have the right to directly pursue Bitcoin assets! Therefore, there is no automatic liquidation based on Bitcoin prices, unlike the margin positions on exchanges.

The above chart shows that the main principal repayment period for MSTR is concentrated between 2027 and 2031. This means that before 2027, MicroStrategy only needs to pay interest each year. Currently, the company has about 1.4 billion in reserves, enough to cover all interest and operating expenses for the next year and a half.

According to the financial model, MSTR has very few loans with restrictions. Even accounting for all leverage, its theoretical liquidation trigger point is around 20,000 dollars, or even lower. Michael Saylor himself even previously stated that even if Bitcoin falls to 1 dollar, we will not be liquidated.

Looking at this, it is actually found that for the short term, MicroStrategy is still relatively safe. But a real crisis is still looming overhead. It is the collapse of logic and the disappearance of premiums!

1. If Bitcoin remains sluggish for a long time, by the time the debt matures between 2027 and 2030, the company may have difficulty refinancing or repaying, leading to a collapse of its spiral financing model.

2. Continuous losses may lead to a downgrade in credit ratings, triggering cross-defaults on debt.

3. If operational cash flow is insufficient to pay interest, and new financing cannot be obtained, it may fall into trouble.

4. Although not subject to forced liquidation, it may be forced to sell some Bitcoin to meet operational needs.

5. Shareholder value is severely damaged, which may ultimately lead to bankruptcy or restructuring.

Do not deify any institution; in this brutal market, everyone is a gambler! Preserving capital and surviving, slowly waiting for that one chance that could potentially be a killing blow offers a glimmer of hope. Let's encourage each other!