The public sees scandal.

Names. Flights. Court transcripts. Billionaires and politicians splashed across headlines.

But buried inside the Epstein document releases is something far more consequential than moral collapse.

It is financial architecture.

And that architecture reads like a long-prepared strategy to choke — and eventually detonate — the silver $XAG market.

This is not gossip.

This is structure.

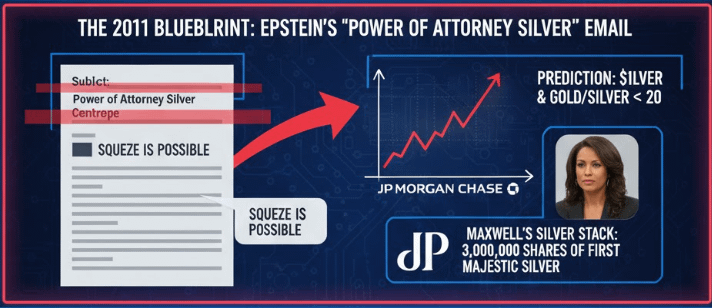

1. The Opening Scene: 2011 — The Blueprint Is Written

May 27, 2011.

An email titled “Power of Attorney Silver Centrope” lands in Jeffrey Epstein’s inbox.

This was not routine account management. Attached was a structured breakdown of how to engineer a silver squeeze through forced physical delivery on COMEX futures contracts.

Not rolling paper.

Not trading volatility.

Standing for delivery.

Draining warehouses.

Stress-testing the system.

The core thesis was direct: if a concentrated entity demanded full physical settlement instead of cash rollover, exchange inventories could be pushed to the edge.

The valuation model projected silver $XAG at $150 inflation-adjusted at the time — the equivalent of well above $200 in 2026 dollars — and a Gold/Silver ratio compressing below 20.

That is not speculative enthusiasm.

That is mechanical pressure modeling.

2. The Positioning: Capital Moved Before the Thesis Circulated

Five months before that email, Ghislaine Maxwell accumulated millions of shares in First Majestic Silver.

First 100,000 shares.

Then roughly 3 million more through a JP Morgan account.

Timing matters.

Large allocations do not appear randomly ahead of structural analysis.

They appear when asymmetry is identified.

Positioning came before disclosure.

Capital moved before conversation.

That is not coincidence.

That is sequencing.

3. The Suppression Machine: Depress Price, Accumulate Metal

Now layer in JP Morgan’s record.

In 2020, the bank paid $920 million to resolve charges tied to years of spoofing in precious metals markets. Fake orders. Artificial liquidity. Engineered price distortion.

Nearly a decade of documented manipulation.

Simultaneously, JP Morgan accumulated one of the largest physical silver stockpiles in modern history.

By 2017, public estimates placed its holdings above 133 million ounces — exceeding what the Hunt Brothers held during their 1980 silver episode.

While paper prices were pressured downward, vault inventories were expanding.

Depress price.

Accumulate physical.

Allow deficits to build.

This is not contradiction.

It is strategic asymmetry.

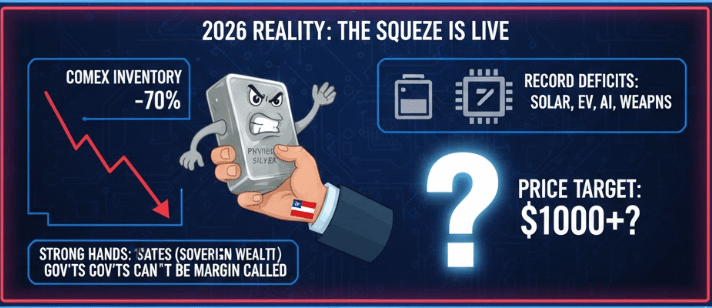

4. The Numbers in 2026: Theory Has Become Stress

In 2011, the squeeze thesis was conceptual.

In 2026, the backdrop is structural.

COMEX inventories have trended lower.

Shanghai inventories have tightened.

Global silver $XAG markets have endured multiple consecutive years of supply deficit.

Industrial demand from solar expansion, EV infrastructure, semiconductor manufacturing, and defense systems has grown materially compared to a decade ago.

The participants have also changed.

In 2011, retail traders attempting squeezes were neutralized through margin hikes.

In 2026, increasingly, sovereign actors are securing physical supply for strategic use.

Governments are not margin-called.

Governments do not liquidate under volatility.

They accumulate.

When physical withdrawal is driven by state-level demand instead of leveraged funds, the suppression mechanism weakens.

Paper can be expanded.

Physical cannot.

5. The Indictment: Price Is Not Value

The Epstein releases do not merely expose individuals.

They expose foresight.

They reveal that more than a decade ago, certain financial actors understood the vulnerability of a paper-heavy silver market resting on finite physical inventory.

Suppress the price through leverage.

Accumulate physical inventory quietly.

Let structural deficits tighten the system.

Wait.

If even part of this structure reflects real positioning, then today’s silver price may represent delay rather than equilibrium.

And delayed repricing in commodities does not unfold gently.

It accelerates.

The danger is not volatility.

The danger is mistaking suppressed price for fair value.

When physical scarcity confronts synthetic supply, repricing is not incremental.

It is violent.

6. Documentation and Verification

This analysis is not based on anonymous claims. The referenced materials are accessible within the publicly released U.S. Department of Justice Epstein document archive.

The May 27, 2011 email referenced above appears under DOJ archive reference code FA01165353. The associated JP Morgan portfolio report appears under reference code FA01520542.

Do not rely on interpretation.

Access the documents.

Read them.

Because once you understand the structure outlined more than a decade ago, the present market stress no longer looks accidental.

It looks engineered.

This is structural analysis, not financial advice.

And structural pressure does not disappear simply because it is inconvenient.

🔔 Insight. Signal. Alpha.

Hit follow if you don’t want to miss the next move!