Stablecoins used to feel like a crypto niche: a convenient “digital dollar” for traders who didn’t want to hop back to a bank account. That picture has changed fast. Today, stablecoins are showing up in places that look a lot more like everyday finance—remittances, merchant settlement, payroll experiments, cross-border B2B transfers. And when money starts moving like that, the plumbing matters. Not the flashy parts. The boring parts: fees, finality, congestion, and what happens when the network is busy at the worst possible time.$XPL

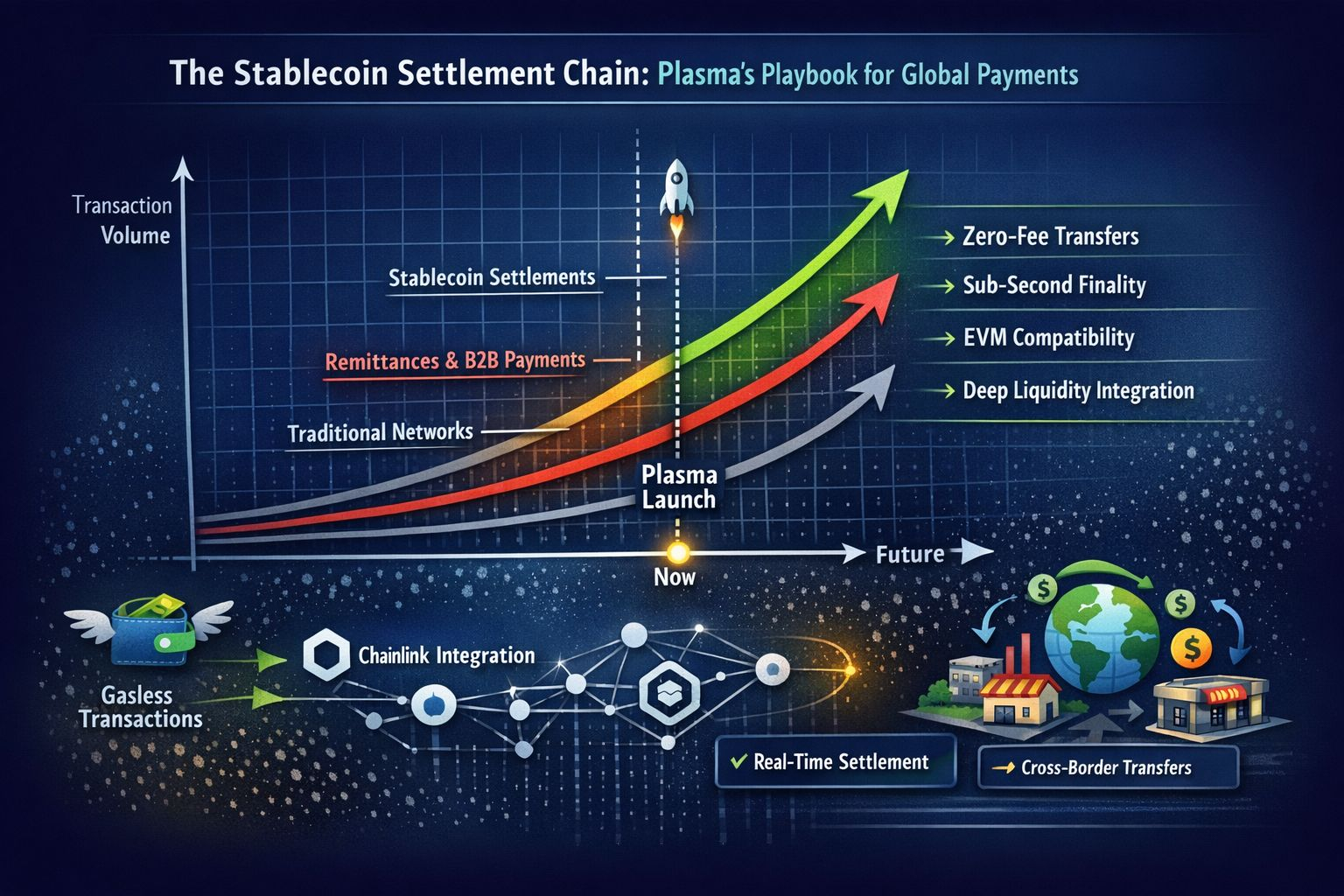

That’s the context in which Plasma is being discussed more and more. Plasma describes itself as a stablecoin-first settlement chain—essentially a Layer 1 designed so stablecoin transfers aren’t competing with everything else for blockspace. The team’s framing is straightforward: most general-purpose networks treat stablecoins like “just another asset,” but stablecoins have become the asset people actually move most often. So why not build rails that assume stablecoins are the main event?

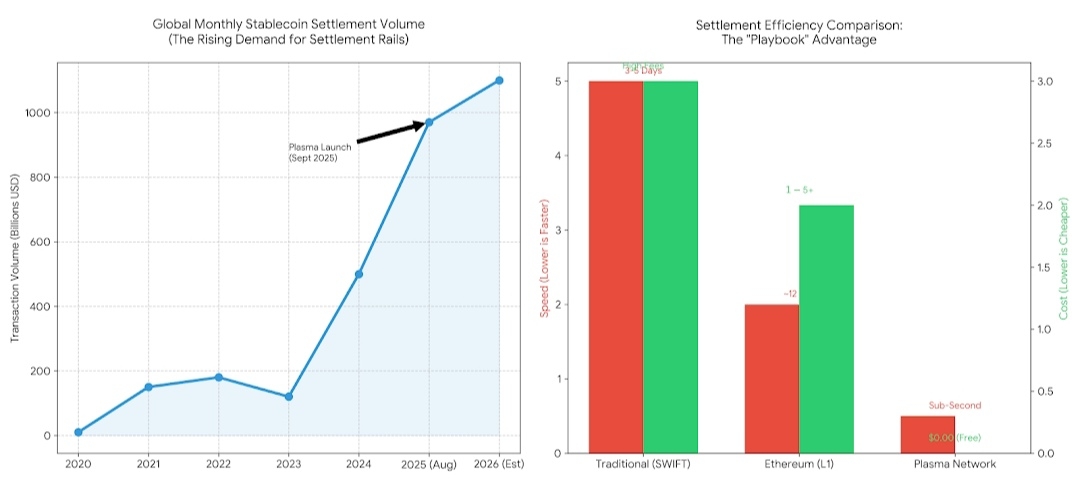

One reason it’s trending now is simple timing. Stablecoins are pushing further into mainstream payment conversations, including among traditional processors. For example, Shift4 announced a stablecoin settlement platform for merchants, supporting multiple stablecoins and networks. That kind of headline makes people look harder at what “settlement” really means when the rails are public blockchains. If merchants and payment companies are treating stablecoin settlement as a real product surface, then the chains optimized for it start to look less theoretical.

Plasma’s “playbook” seems to rest on a few pragmatic bets.

First: reduce friction for the most common action—sending stablecoins. Plasma launched with a pitch around zero-fee USDT transfers and sub-second finality using its own consensus design, PlasmaBFT. The point isn’t that fees are always huge everywhere; it’s that even small fees become meaningful when you’re doing high-frequency payments, small transfers, or operating in cost-sensitive corridors. And finality isn’t a marketing word in payments—it’s the difference between “funds available” and “funds pending.”

Second: make the chain feel familiar to builders while changing the economics under the hood. Plasma emphasizes EVM compatibility, which matters because payment apps don’t want to reinvent everything from scratch. At the same time, Plasma’s research coverage highlights features that are unusually “payments-native,” like gasless transfers and stablecoin-based gas mechanics—details that sound minor until you imagine onboarding a normal user who doesn’t want to hold a separate token just to pay network fees.

Third: start with liquidity and integrations, not “we’ll add that later.” Plasma’s public coverage repeatedly mentions launching with deep liquidity and many DeFi integrations from day one. In payments, liquidity is not a bonus feature—it’s the cushion that helps systems behave predictably at scale, and it’s what makes “instant” feel real rather than aspirational.

There’s also a quiet but important fourth bet: interoperability and data infrastructure. #Plasma has public announcements around integrating Chainlink tooling (including CCIP and data feeds) and joining Chainlink Scale. You don’t have to be a DeFi person to care about that; if you’re settling value across systems, reliable messaging and price/data primitives become part of operational risk.

So what counts as real progress, beyond narratives? Mainnet launch matters, but the more interesting question is whether the chain can stay cheap and predictable when activity spikes. Another test is whether “free” transfers can remain sustainable without slipping into hidden costs somewhere else—like worse execution, higher spreads, or centralized gatekeeping. Some research writeups describe a freemium-like model where basic transfers are cheap/free while programmable activity supports the economics. It’s a clever idea, but it still has to survive real usage patterns, not just whiteboard math.

And there’s a human question I keep coming back to when I read about projects like Plasma: if you handed this to a small business owner who sends money across borders every week, would they feel the difference in one day? Lower fees are nice, sure. But what they remember is whether transfers are consistent, whether support is clear when something goes wrong, and whether the system behaves the same on a Monday morning as it does during market chaos.

Plasma is one attempt to take that expectation seriously by specializing the chain around stablecoin settlement. It might not be the only approach, and it won’t replace banks overnight. But in a world where stablecoins are increasingly treated like practical money rather than a crypto instrument, specialized settlement rails are no longer a strange idea. They’re a logical next step—and @Plasma is trying to write the play for that next step.