The same 'outstanding' non-farm employment report is seen by traders as irrefutable evidence for delaying interest rate cuts, while for Trump, it is a rallying cry that 'America is strong, so interest rates must be at their lowest.' And caught in the middle, the Federal Reserve is staging a performance of a departing governor's 'lonely opposition' to colleagues.

Washington time February 11, the non-farm payroll data for January showed an increase of 130,000, and the unemployment rate dropped to 4.3%. Logically, an overheated economy should dampen expectations for interest rate cuts. However, the conclusion given by the White House is exactly the opposite: precisely because the data is good, the interest rate cuts should accelerate.

This is not a divergence in economics, but a reflection of the misalignment between the power cycle and the policy cycle. Meanwhile, across the ocean, Bitcoin provided a deeply meaningful reaction — a collapse followed by a surge, completing a full long-short trap within 24 hours.

1. The "two faces" of non-farm: traders see hawks, the White House sees doves.

1. The "two faces" of non-farm: traders see hawks, the White House sees doves.

Looking solely at the headline figure of 130,000 non-farm jobs in January, it certainly far exceeded the expected 55,000. But breaking it down, this report is not clean:

● First, there is a severe structural imbalance. Healthcare and social assistance contributed 122,000 jobs, almost encompassing all the growth; federal government employees decreased by a net 34,000, and the "delayed resignation plan" implemented after Trump's election began to be counted in the statistics. The real demand for labor in the private sector is far from being as hot as the headlines suggest.

● Second, the annual revisions have been selectively ignored. The total employment for 2025 was heavily revised down by 862,000, shrinking from 584,000 to 181,000—this means there was almost no hiring last year. The rebound in January resembles a slight jump from the bottom rather than a takeoff.

● However, the market does not care about this. CME FedWatch shows that the probability of no change in March skyrocketed from 79.9% to 94.1%, and the probability of no rate cut in June rose from 24.8% to 41.1%. Bets on Polymarket are even more extreme, with traders nearly wiping out hopes for a rate cut in June.

Strangely, the White House is completely dismissive of this.

● The statement Trump posted on Truth Social is quite intriguing. He did not mention "inflation is controllable," nor did he criticize Powell as he typically does; instead, he framed rate cuts as a privilege of a strong nation—"We are number one in the world, so we should pay the lowest interest rates."

● This is a de-technologized narrative. Simplifying complex interest rate resolutions into "strong countries are entitled to low costs" bypasses the independence of the Federal Reserve and the stubborn inflation in the service sector.

● However, what truly caught the market's attention was not Trump's post but the soon-to-depart Federal Reserve board member—Stephen Miran.

2. Miran's "final resistance": the rare logic of supply-side dovishness.

Stephen Miran is a unique figure.

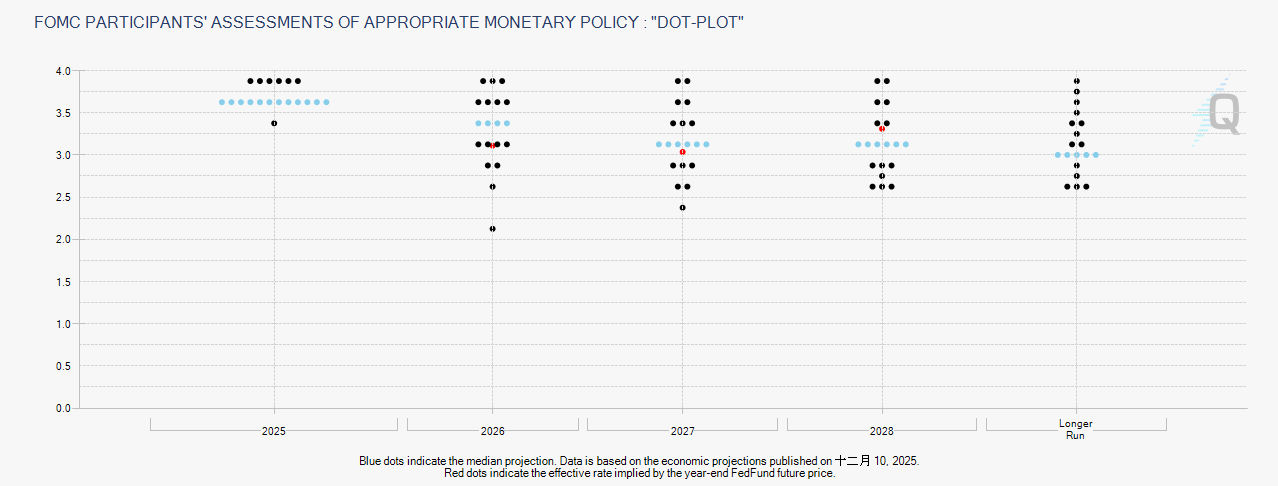

● Since joining the Federal Reserve Board in September 2025, he has voted against every policy meeting—it's not that he opposes rate cuts, but he thinks they're happening too slowly and conservatively. At the January FOMC meeting, colleagues unanimously agreed to stay put, with only he and Waller (Christopher Waller) insisting on cutting another 25 basis points.

● His term expired on January 31. According to protocol, he can stay until his successor is confirmed, but everyone knows that Trump nominated Kevin Waller to take the very chair he occupies.

But Miran did not hold back.

In response to the questioning of "why cut rates when non-farm data is so good," his response is layered, each level challenging the traditional framework of the Federal Reserve:

● First layer: strong employment does not equal the need to hit the brakes. Miran believes that the U.S. economy still has the potential to absorb about one million new jobs without triggering inflation. The current labor market is not "overheated" but is simply "just pulling back a foot from the edge of the cliff." At this point, cutting rates is not pouring oil on the fire, but rather providing insurance for the economy to prevent unexpected contractions caused by policy lag.

● Second layer: supply-side reforms are rewriting the lower limits of interest rates. This is the core and most controversial part of Miran's logic. He believes that the deregulation, early retirement plans, and the reduction of government employees (which has already decreased by 360,000) promoted by the Trump administration are enhancing total factor productivity. If the supply side can run faster, the demand side's interest rates should not lag behind. In other words, the same economic growth now requires lower nominal interest rates than in the past.

● Third layer: housing inflation is going to come down, and tariffs are not that scary. Miran is much more optimistic about inflation than his colleagues. He estimates that the current core inflation rate is about 2.3%, already within the error range of the 2% target, and the lagged effects of the housing component are about to be released. As for tariffs, he considers them to be "relatively weak" factors, with no widespread transmission signs.

This logic of "supply creates room for rate cuts" is absolutely a minority view within the Federal Reserve. Most decision-makers are reluctant to bet short-term policies on long-term productivity—what if productivity doesn't arrive, and inflation returns first? How would that play out?

However, Miran's remarks are important not because he can change the decisions made in January or March, but because he represents the White House's attempt to implant a new narrative into the Federal Reserve. Once Waller takes over, this logic will shift from "personal dissent" to "chair's tone."

3. The "split personality" of market pricing: how much is left in the June window?

Traders are very honest; they do not follow political slogans.

● After the non-farm report came out, short-term interest rate futures faced selling. The pricing for a rate cut in June devolved from "a done deal" to "fifty-fifty," with the probability of action before April dropped below 20%. Reports from JPMorgan and Wells Fargo were unusually consistent: this data has made the likelihood of a rate cut in the first half of the year increasingly small.

● However, the market's "hawkish pricing" is not complete. The yield on the 10-year U.S. Treasury rose only slightly by 2.77 basis points, closing at 4.17%. This range is very restrained, indicating that no one is betting on the resumption of the rate hike cycle. Although the three major U.S. stock indices closed down, the declines were all within 0.2%, with the S&P 500 nearly flat.

● This is a pricing stance of "rate cuts being late but not absent." No one believes the Federal Reserve will turn hawkish; they are just betting on whether the first rate cut will be in June or July, and whether there will be two cuts or just one for the year. Amid this relatively dull macro landscape, the crypto market has provided a distinctly different intensity.

4. The crypto market's "predict your predictions": recovering from the crash.

4. The crypto market's "predict your predictions": recovering from the crash.

● On the evening of February 11, within an hour after the non-farm data was released, Bitcoin fell below the $66,000 mark, with a 24-hour decline exceeding 5% at one point. This decline direction was consistent with the trend after the U.S. stock market opened, but the magnitude far exceeded the Nasdaq's 0.16%. Assets with shallower liquidity are more sensitive to interest rate expectations—this pattern still holds true.

● After 00:00 on the 12th, Eastern Standard Time, Bitcoin pulled up from a low of $65,984, quickly breaking through $67,000, recovering more than half of the daily decline. As of the early morning close, it was reported at $67,035, rebounding over $1,000 from the lowest point.

● This "first a crash, then a deep V" trend is typical of speculative buying entering the market. Some are betting that the market has overinterpreted the non-farm report, wagering that traders will reprice after cooling down.

● Fairly speaking, this non-farm report is indeed insufficient to support a long-term high level of real interest rates. The unemployment rate of 4.3% remains historically low, but total employment is down by more than three million compared to pre-pandemic levels, and the recovery of the labor participation rate is extremely slow. Excluding the one-time impact of government layoffs due to regulatory dividends, the endogenous momentum is not strong.

● The crypto market has never followed macro data; instead, it predicts "the market's predictions of macro data." Crashes are a submission to immediate sentiment, while rises reflect long-term pricing in anticipation of the Federal Reserve being forced to turn dovish in the second half of the year.

5. Seats and terms: hidden variables determining the 2026 interest rate path.

5. Seats and terms: hidden variables determining the 2026 interest rate path.

● One person cannot be overlooked: Kevin Waller. Trump has clearly nominated Waller to replace Miran’s board seat and will officially appoint Waller after Powell's term ends in May. The market's stereotype of Waller is "hawkish"—he was known for his anti-inflation stance during his previous term at the Federal Reserve.

● However, careful analysis reveals that the macro environment in which Waller finds himself has turned upside down. In 2018, he faced a tax hike cycle and idle production capacity; in 2026, he faces a deregulation cycle and a productivity pulse. He recently acknowledged in a closed statement that productivity improvements could change the estimates of the long-term neutral interest rate.

● Waller's real challenge is not whether his stance is left or right, but whether to take over the "supply-side rate cut logic" left by Miran. If he does not take it on, it will conflict with the White House's expectations; if he fully adopts it, it means a substantial shift in the Federal Reserve's policy framework.

● There is also a more subtle institutional issue: Powell's Federal Reserve board seat doesn't expire until January 2028. If Powell retains his board seat after stepping down as chairman in May, the Federal Reserve will experience a rare situation of "one former chair and one new chair" coexisting. This is extremely uncommon in the century-long history of the Federal Reserve.

● Miran's remark in an interview, "I would be happy to stay on, but that is not up to me," subtly expresses the uncertainty surrounding this personnel change. Even if he wants to stay and continue fighting as a dove, the physical vacancy of the position does not change with personal will.

When economic data does not support rate cuts, but policymakers are determined to cut rates, whom should the market listen to? The answer for the past fifteen years has been "listen to the Federal Reserve." But this year, the White House is trying to change that answer.

Trump's policy rhythm in his second term has clearly accelerated. Deregulation, spending cuts, and expanding production capacity—these supply-side measures, the faster they are implemented, the more the Federal Reserve's justification for maintaining high interest rates is eroded. Even if inflation remains sticky, real interest rates are already too high.

The rapid rebound of Bitcoin after the crash is a tentative recognition of this logic by risk assets. It may not be correct, but it reflects the urgency of capital seeking an exit.

As for Miran, this "shortest-lived" dovish member of the Federal Reserve completed his last few lonely dissenting votes during the countdown of his term. His policy suggestions did not win over his colleagues, but his framework of thought is gaining traction in the White House. May in Washington is truly the moment of reckoning.