A few months ago I tried sending a small payment across three different chains just to see where liquidity actually felt alive. I wasn’t looking at token prices. I was watching what people were actually using. What struck me was simple and a bit quiet: almost every meaningful transfer involved a stablecoin.

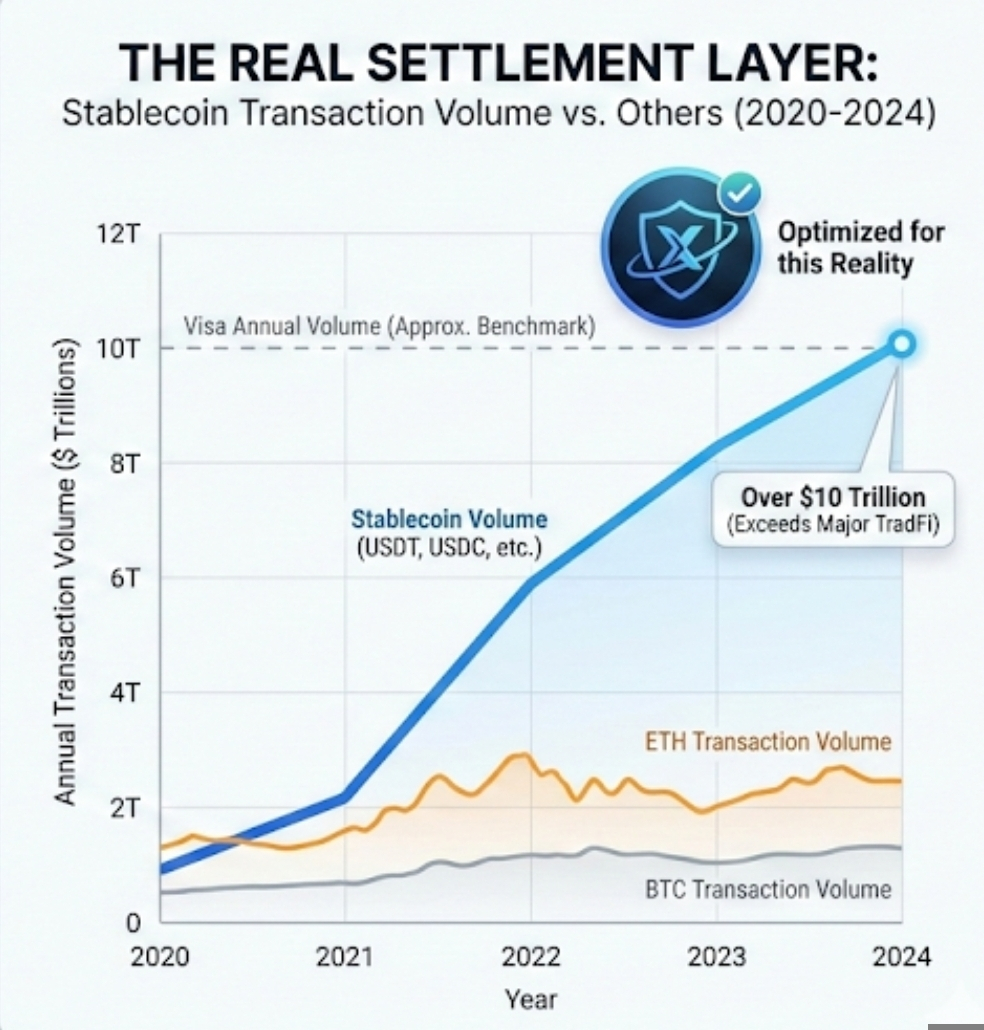

We still talk about Layer 1 competition as if ETH, SOL, or BTC are the center of gravity. But if you look at transaction volume instead of narratives, the texture changes. In 2024, stablecoin transfer volume crossed well over $10 trillion annually. That number matters because it exceeds Visa’s annual payment volume in some years. It tells you something uncomfortable. The dollar, wrapped on-chain, is already functioning as the real settlement layer for crypto activity.

That momentum creates another effect. Stablecoins now represent over $150 billion in circulating supply across USDT, USDC, and others. When that much synthetic dollar liquidity sits on-chain, the chain becomes less important than the dollar rail itself. Traders arbitrage in USDT. DeFi pairs settle in USDC. Even meme coin rotations usually route through stables first. Underneath all the noise, the foundation is dollar liquidity.

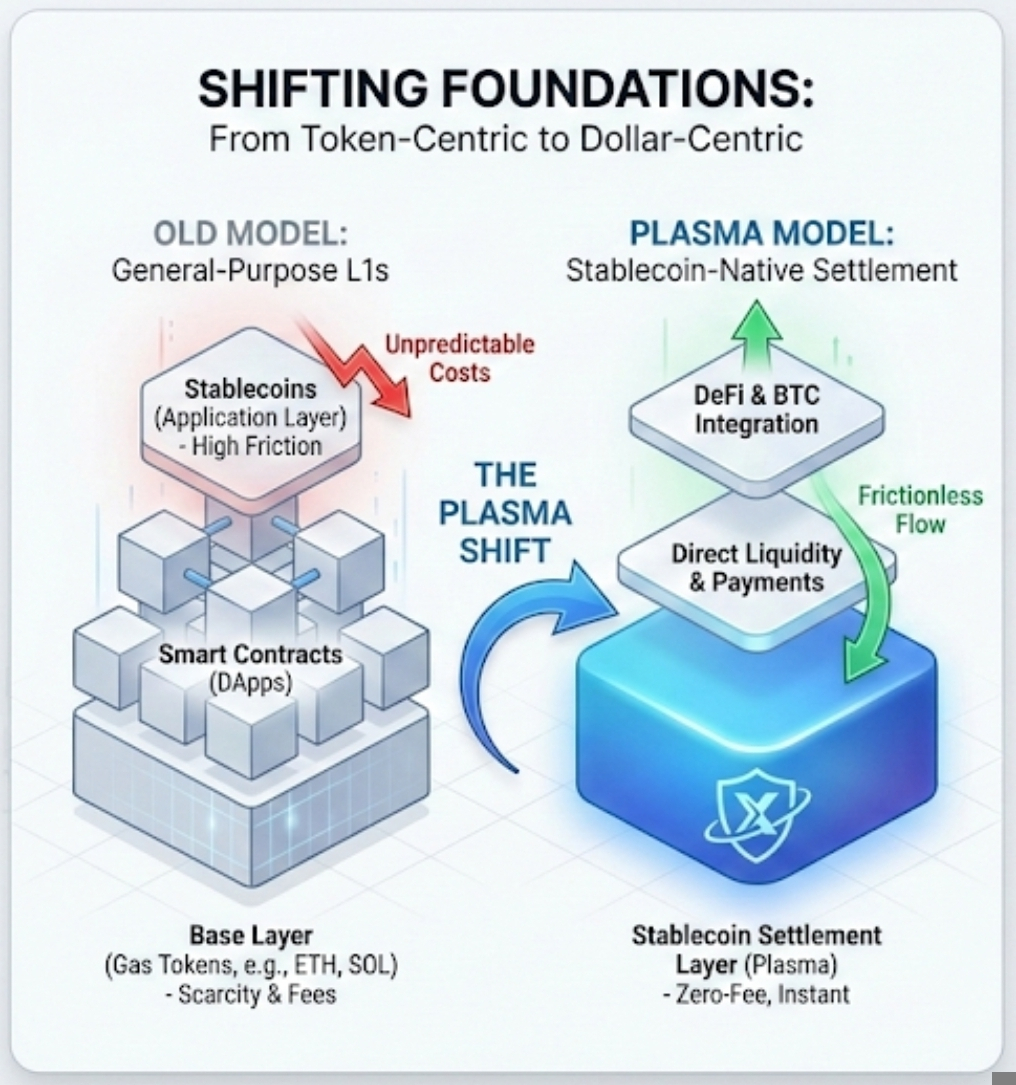

Understanding that helps explain why some infrastructure decisions feel outdated. Many chains were designed for general-purpose smart contracts first and stablecoins second. Gas tokens capture value through transaction fees. Blockspace becomes scarce. Users pay unpredictable costs just to move dollars around. That design made sense in 2017 when experimentation was the point. It feels less aligned now that stablecoins behave more like payment rails than experimental tokens.

When I first looked at Plasma, what stood out was not a flashy feature. It was the decision to treat stablecoins as the primary unit of economic activity rather than an application on top. That shift is subtle but important. On the surface, Plasma talks about zero-fee transfers and native stablecoin settlement. Underneath, it is rethinking what the base layer is actually for.

Zero fees sound simple, but they are not cosmetic. On most networks, fees serve two roles. They prevent spam and they capture value for validators. If you remove fees for stablecoin transfers, you are not just improving user experience. You are changing the incentive structure. Plasma’s model leans on alternative value capture, such as ecosystem-level incentives and liquidity positioning, rather than taxing every dollar movement. That changes how capital flows.

Meanwhile, stablecoin usage keeps rising in places where local currencies are weak. In 2023 and 2024, countries like Argentina and Turkey saw spikes in USDT trading volume relative to GDP. That context matters. People are not using stablecoins for yield farming. They are using them as digital dollars. When that behavior becomes steady rather than speculative, infrastructure that reduces friction starts to look less like a feature and more like a necessity.

There is also a liquidity map angle that few talk about. On Binance, a large percentage of spot pairs are quoted in USDT. Billions in daily volume route through stablecoin markets. If stablecoin-native chains lower transfer friction between venues, arbitrage tightens spreads. That means liquidity moves faster. Faster liquidity is not just good for traders. It quietly reshapes where capital prefers to sit.

Now layer in the Bitcoin angle. Wrapped Bitcoin products have grown into tens of billions in value across DeFi. That number reveals demand, but it also shows friction. Users want BTC liquidity without Bitcoin’s slower UX. Plasma’s native bridge thesis suggests that instead of forcing Bitcoin into complex wrappers, you design a settlement environment where BTC liquidity can interact with stablecoins more directly. If that holds, it reduces psychological and technical barriers at the same time.

Of course, risks remain. Stablecoins rely on centralized issuers. USDT and USDC depend on reserves held in traditional banks. If regulation tightens or banking partners shift, the foundation could wobble. There is also the question of spam resistance in zero-fee environments. If you remove transaction costs entirely, you must design other filters. That is not trivial.

Critics might argue that Ethereum already dominates stablecoin settlement, processing hundreds of billions monthly despite high fees. That is true. But high fees during congestion reveal something else. When gas spikes to $20 or $50 per transaction, small transfers become irrational. That creates a tiered system where only larger players can move efficiently. Plasma’s bet is that if stablecoins are the base layer, transfers should feel like moving dollars in a banking app, not bidding for blockspace.

Early signs in the market support this shift. Over 70 percent of on-chain transaction count in some periods involves stablecoins. That proportion matters because it shows usage concentration. We are not watching a diverse economy of tokens. We are watching a dollar-centric network with other assets orbiting around it. If that pattern continues, chains optimized for generic programmability may slowly cede ground to chains optimized for dollar throughput.

There is also a psychological shift underway. Traders increasingly evaluate chains by liquidity depth and settlement speed rather than developer count. When stablecoins move instantly and cheaply, that becomes the benchmark. A chain that cannot match that texture feels heavy. Plasma is building for that comparison, not for the old narrative of smart contract expressiveness.

Meanwhile, regulatory tone is softening in parts of the world. In the United States, discussions around stablecoin legislation have become more concrete. In Europe, MiCA frameworks are already active. If regulated stablecoins gain clearer status, their role as settlement assets strengthens. Infrastructure aligned with that reality may find itself in a favorable position.

None of this guarantees Plasma’s dominance. Execution matters. Liquidity bootstrapping is hard. Network effects are earned, not declared. But the framing feels directionally correct. If stablecoins are the steady layer underneath trading, payments, and even speculative cycles, then designing a chain around that assumption makes strategic sense.

Zoom out further and a pattern emerges. Crypto began as an experiment in decentralized money. Over time, it has quietly become an experiment in digital dollars. The asset that moves most is not ETH or BTC. It is USDT. That fact alone should reshape how we think about base layers.

If stablecoins are becoming the real base layer, then the chains that treat them as the foundation rather than the application are aligning with where activity already lives. The old model built chains for tokens and let dollars adapt. The new model builds chains for dollars and lets everything else orbit around them.

And if this trend continues, the chains that win may not be the ones with the loudest ecosystems, but the ones that quietly make moving a dollar feel like nothing at all.