Not long ago after a long stretch of meetings I was relaxing with a friend at a café. When the bill arrived there was no debate over who owed what. He simply said “Send it over.” I opened my wallet, entered the USDT amount, and within moments the payment was complete. No lag. No hunting for a separate token to cover fees. No mental checklist about whether I had enough gas. The ease of it felt ordinary which is exactly why it stayed with me.

I’ve used nearly every payment system available over the years: bank transfers cross-border wires card networks and multiple blockchains. They all accomplish the task but each introduces subtle friction. Sometimes that friction shows up as delays. Sometimes it’s cost. Other times it’s the quiet concern about holding the correct token to make a transaction process. That evening made something clear: Plasma didn’t feel like a blockchain mimicking money. It felt like actual money that simply happened to operate on-chain.

Wanting to understand why it felt different I looked deeper into how Plasma is structured. It operates as a Layer 1 blockchain purpose-built for stablecoin settlement. While that sounds technical the premise is simple. Rather than building a general blockchain and later adding stablecoins as just another asset, Plasma designs its entire system around stable value from the start. USDT isn’t an add-on it’s foundational to the network’s architecture.

That design choice carries meaningful implications. Most real-world payments are not speculative trades. They involve invoices payroll supplier payments remittances or trade settlements. These transactions depend on stable amounts. When a company agrees to pay $50,000 it expects $50,000 not a fluctuating figure by the time funds arrive. By centering infrastructure on stablecoins Plasma aligns with how businesses already conceptualize money.

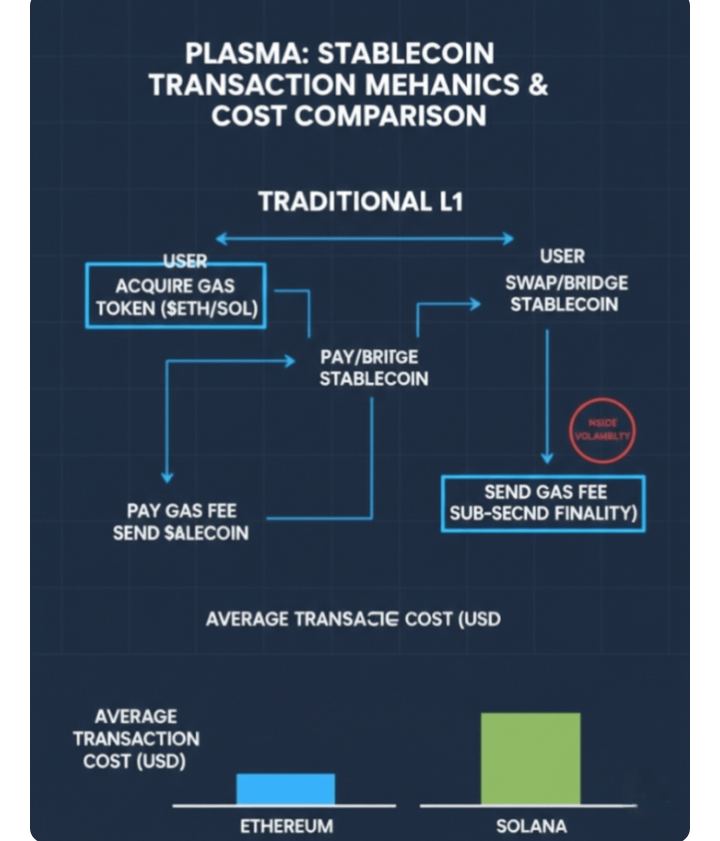

One particularly practical difference lies in transaction fees. On many networks users must maintain a separate native token just to pay for processing. It’s like needing a second currency simply to move the first one. That requirement can be confusing for casual users and operationally inefficient for institutions. Plasma approaches this differently. Standard USDT transfers can be gasless and when fees are required they may be paid directly in stable assets such as USDT. In other words the currency being sent can also serve as the fuel.

To make it relatable imagine paying for SMS credits in dollars but needing to convert part of that balance into another internal token before sending a message. Or consider a car that requires a voucher before allowing you to use fuel. Plasma removes that extra conversion step. The native token XPL still exists and performs essential roles supporting validators maintaining security and sustaining the network but it operates mostly behind the scenes rather than adding complexity for everyday transfers.

Settlement finality is another area where distinctions matter. Many platforms advertise fast transactions but speed alone doesn’t equal certainty. A payment notification doesn’t always mean funds are irrevocably cleared. Traditional banking systems frequently leave transactions pending for extended periods creating a gap between acknowledgment and completion.

Plasma employs a consensus mechanism known as PlasmaBFT designed to reach finality in under a second under typical conditions. Once confirmed transactions are not left in a reversible state awaiting multiple additional confirmations. They are final. For merchants payroll operators and financial applications that certainty reduces reconciliation burdens and lowers the need for temporary liquidity buffers particularly in environments handling large transaction volumes where small inefficiencies can accumulate quickly.

The network’s technical compatibility is also notable. Plasma supports full EVM compatibility through Reth allowing developers to use familiar Ethereum-based tools and smart contracts with minimal modification. Many new infrastructures demand entirely new development stacks increasing adoption friction. Plasma avoids that by aligning itself with established tooling reducing switching costs and preserving flexibility for builders.

I also reviewed early ecosystem integrations not as guarantees but as indicators of strategic direction. Trust Wallet supports direct asset transfers on Plasma. Rhino.fi provides liquidity and bridging across more than 35 chains broadening access to capital. Chainalysis has enabled automated token support for compliance monitoring. Elliptic contributes AML KYC and KYT oversight capabilities. Together these partnerships signal that Plasma is aiming to serve as credible financial infrastructure rather than a purely experimental network.

There are also longer-term ambitions involving Bitcoin anchoring and a pBTC bridge. These components are still in development and remain on the roadmap rather than fully implemented. That distinction is important. Trust in payment systems comes from what works now not solely from what is planned. If these features mature successfully they could enhance neutrality and security but they are still evolving.

In conversation I’ve described Plasma’s focus this way: it isn’t trying to be everything at once. It concentrates specifically on stablecoin settlement. A colleague once compared it to building a highway designed for heavy freight rather than mixing trucks with bicycles and sports cars. The analogy fits. The network is optimized for steady, high-value transfers.

The XPL token plays its part in securing the network and compensating validators particularly for more complex operations. However simple USDT transfers are structured to minimize or remove the need for additional friction. In that sense the token functions as infrastructure rather than as the focal point of user interaction.

Liquidity is another critical factor. At mainnet beta Plasma reported more than $2 billion in stablecoin total value locked placing it among networks with substantial stablecoin liquidity. Rhino.fi’s integration from launch enabled bridging across dozens of chains. Without liquidity a payment network cannot function effectively. Capital availability determines whether funds can move reliably and at scale.

Naturally challenges remain. Projected throughput in the thousands of transactions per second does not always mirror early real-world demand. The broader ecosystem beyond transfers and lending is still developing. Competition from Ethereum Layer 2 solutions and Tron remains strong. And widespread payment adoption depends not only on technical performance but also on regulation partnerships and user trust. Plasma does not eliminate these broader realities.

What stands out is its disciplined scope. Rather than attempting to reconstruct the entire financial system it focuses narrowly on stablecoin settlement. If it succeeds users may barely notice it. They will send USDT see it arrive instantly and continue with their day. The infrastructure will operate quietly in the background.

Reflecting on that evening at the café the defining feature wasn’t complexity or novelty. It was the absence of friction. No additional tokens. No delays. No second thoughts. If Plasma continues in this direction it may become nearly invisible and in payments invisibility is often the ultimate compliment. The most effective systems don’t demand attention. They simply function like power flowing through walls or fuel powering an engine. You only think about them when they fail. If Plasma delivers on its vision moving digital dollars could feel as seamless as sending a text.