The European Commission's 20th sanctions package proposes a comprehensive ban on all cryptocurrency transactions involving Russia, escalating from targeting specific bad actors to attempting to sanitize the rails themselves.

The key question: can the EU raise the cost of evasion by controlling chokepoints such as regulated exchanges, stablecoin issuers, and third-country financial intermediaries?

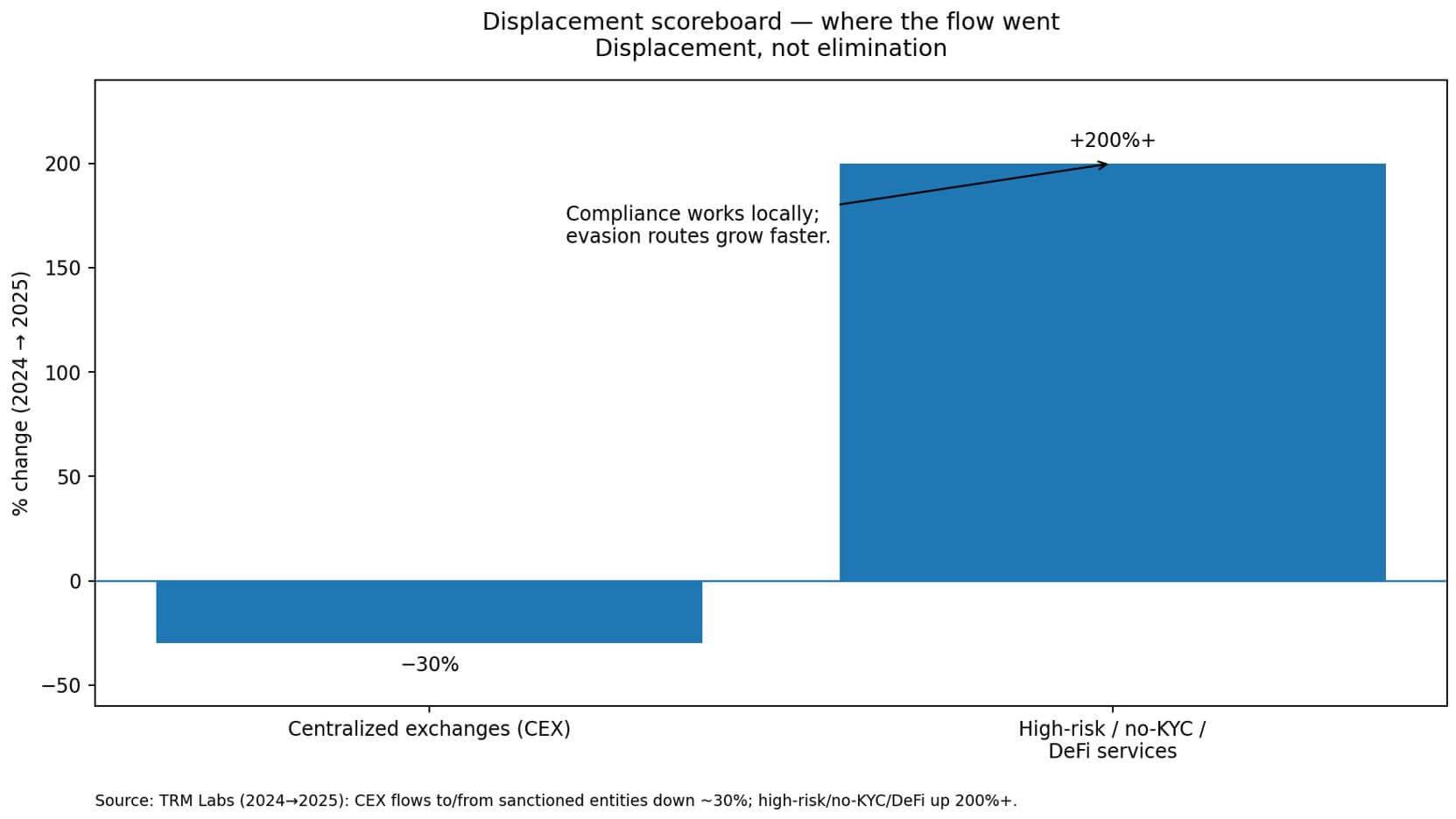

Enforcement data already shows displacement. Between 2024 and 2025, flows to and from sanctioned entities via centralized exchanges fell roughly 30%, according to TRM Labs. Over the same period, flows through high-risk, no-KYC, and decentralized services increased by more than 200%. Russia hasn’t stopped using crypto for cross-border trade it has just shifted activity beyond Western compliance infrastructure.

What’s new vs. what’s already banned

The EU’s Russia sanctions framework already prohibits providing crypto-asset wallet, account, or custody services to Russian nationals, residents, and Russia-established entities.

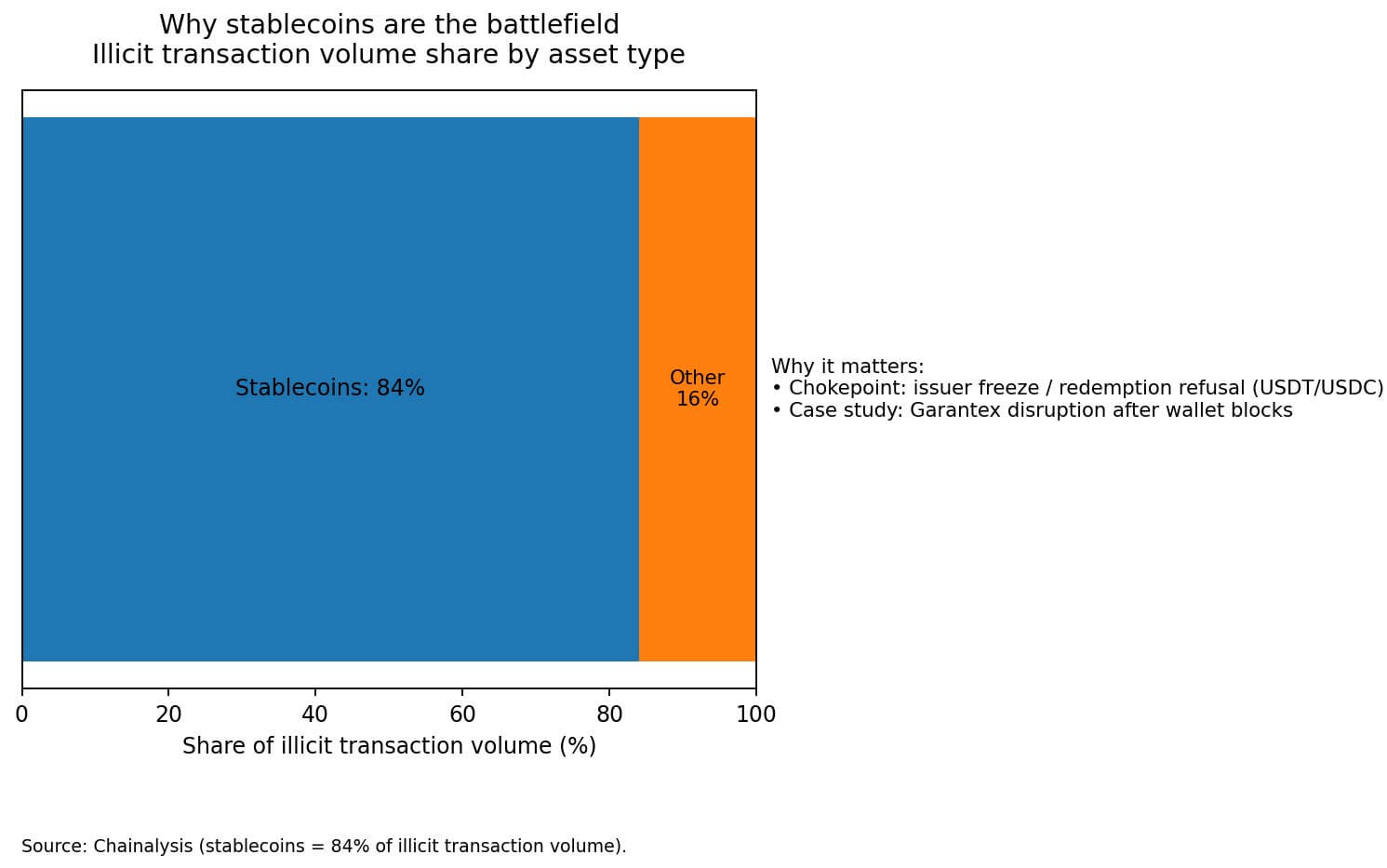

The 19th package banned transactions involving the Russia-linked stablecoin A7A5, which Chainalysis estimates processed $93.3 billion in under a year. Specific infrastructure associated with Russia’s crypto ecosystem was also sanctioned.

The new blanket ban expands the perimeter: any EU person or business dealing with Russia-linked crypto service providers or facilitating Russia-related transactions falls under scope. Draft language explicitly flags third-country facilitators, shifting from “sanction the actor” to “sanitize the rail” making infrastructure itself harder to use.

How evasion works

Sanctions evasion in crypto happens across three layers:

Identity: fake KYC, shell entities, nominee accounts — easiest and least impactful

Jurisdiction: routing through non-EU virtual asset service providers, OTC desks, Telegram brokers, and third-country banks

Instrument: shifting to stablecoins and bespoke rails that bypass traditional banking

Chokepoints that matter

Stablecoin redemption: If issuers like Tether or Circle freeze or block Russia-linked wallets, evasion costs rise sharply.

Third-country facilitators: If Russia can cash out via jurisdictions outside EU enforcement, the ban’s total impact is minimal. Secondary sanctions or market-access restrictions are needed to exert influence.

EU-regulated CASPs: Strong compliance reduces flows touching EU platforms; weak enforcement allows displacement. The 30% decline via centralized exchanges reflects baseline compliance.

Compliance-only: EU CASPs comply. Offshore and no-KYC venues remain accessible. EU-touchpoint flows drop 20%-40%, later 60%-80%, but most displaced flow reappears via non-EU platforms. Russia-linked crypto activity overall barely changes.

Chokepoint squeeze: EU coordinates with stablecoin issuers and targets third-country facilitators. EU-touchpoint flows fall 50%-75%, forcing Russia to pay higher friction costs in OTC markets, more intermediaries, and bespoke rails like A7A5. Total activity persists but is costlier and riskier.

The EU can make Russia's crypto routes more expensive and less convenient.

Regulated EU exchanges and custodians will shut their doors to Russia-linked flows, and the compliance baseline will tighten.

Yet, unless the EU can control stablecoin issuers, coordinate with third-country regulators, and maintain consistent supervision of its own CASPs, the blanket ban will function more like a reroute order than a shutdown.

Russia will still use crypto for cross-border trade and to evade sanctions. It will just do so through venues the EU can't see, at costs Russia has already demonstrated it's willing to pay.