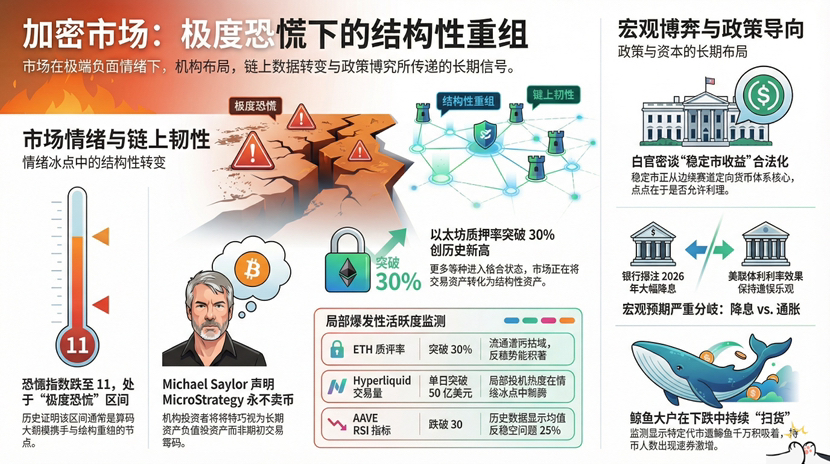

The market sentiment has reached its limit. Today's crypto fear index is 11, still in 'extreme fear'. Bitcoin's rebound is weak, $ETH falling over 4% in one day, and many people are starting to ask the same question: is it not at the bottom yet? But what is truly interesting is that it has never been the price itself, but rather when the market is most fearful, who is buying, who is making statements, and who is planning the next step.

Michael Saylor publicly responded again: concerns in the market about Strategy being forced to sell Bitcoin are unfounded; the company will continue to buy and will never sell. This is not emotional trading; this is a balance sheet level attitude. In the last cycle, many institutions collapsed during the 'liquidity crisis', but this time, Strategy chose to directly bet on the long term. The biggest signals in panic often come from those who do not need to make statements.

Meanwhile, an intriguing change has occurred in Ethereum's on-chain data. During the downturn, the volume of token transfers surged instead. On-chain extreme activity typically appears during two moments: at the tail end of panic selling or at nodes where chips are being significantly transferred. More critically, the ETH staking rate has surpassed 30%, reaching a historic high. More and more chips are choosing to lock up rather than circulate, meaning the market is turning 'trading assets' into 'structural assets'. If sellers truly exhaust themselves, a rebound only needs a trigger point.

The situation over there is even more dramatic. Hyperliquid's HIP-3 daily trading volume surpassed $5 billion, and the precious metals craze has boosted activity; AAVE's three-day RSI fell below 30, with historical data showing that rebounds in this range average over 25%; whales bought 48 million Pippin tokens, leading to a surge in the number of holders, with the token price soaring over 40% in a single day. Sentiment is at a freezing point, but local speculation is boiling. This kind of 'ice and fire', is often the most typical scene in the mid-cycle.

On a macro level, there is also division. Goldman Sachs' CEO believes the macro environment is very favorable for risk assets, while State Street Bank predicts that the rate cuts in 2026 may exceed expectations, with the dollar potentially falling by 10% over the year. However, the Federal Reserve maintains a calm stance, stating that there is no urgent need for rate cuts this year, being 'cautiously optimistic' about the current interest rates while remaining vigilant against inflation risks. Trump has loudly proclaimed that the U.S. should have the lowest interest rates in the world. The market is betting on easing while also worrying about a resurgence of high inflation, leading to heightened divergence.

What is truly noteworthy is the White House's second round of stablecoin yield meetings. Crypto reporters describe the meetings as 'productive', but no compromise has yet been reached. The core of the divergence is simple: can stablecoins actually yield returns? If returns are allowed, the deposit structure of the banking system would be torn open; if not allowed, the allure of on-chain dollars would be suppressed. This is no longer just a cryptocurrency issue, but a monetary structure issue. The future of stablecoins is becoming the focal point of policy games.

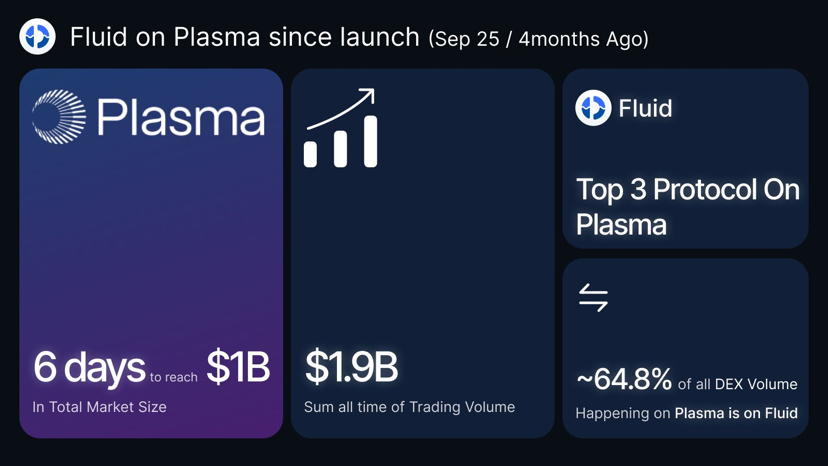

This is also why I continue to pay attention to @Plasma $XPL projects that are oriented towards stablecoin infrastructure. Short-term prices will follow market fluctuations and may even drop together in extreme panic, but what truly determines long-term value is how settlement channels, liquidity efficiency, and regulatory frameworks are implemented. When the White House discusses 'stablecoin yields' and banks are brought to the table for the first time, this track has moved from the edge to the core.

Santiment points out that Bitcoin's rebound cannot hide the panic, but the probability of a sustained rebound is increasing. Historical experience tells us that when the panic index hovers around 10, it is often not the starting point of a crash, but rather a stage of structural reorganization. Selling pressure is released, leverage is cleared, chips are transferred, staking is on the rise, whales are buying, and policy games are being played; these signals combined do not resemble an ending, but rather a brewing.

Short-term? Fluctuations, violent swings, and emotional pulls will continue. Both bulls and bears should not be too confident. Long-term? If the dollar truly enters a down cycle, if stablecoin rules gradually clarify, and if mainstream institutions continue to allocate, the pricing logic of Bitcoin and core infrastructure assets will be rewritten.

Panic 11 is not the endpoint, but a test. The market is asking: who is the true believer and who is short-term capital? When the emotional tide recedes, those that remain will be the true protagonists of the next cycle.

#Plasma #黄金白银反弹 #何时抄底? #BTC #加密货币 $BTC