CoinGlass’s 2025 derivatives data shows that after a deep deleveraging phase earlier in the year, open interest (OI) — a proxy for capital allocated into leveraged positions — recovered meaningfully and even reached historical highs before retracing. By year-end, OI (~$145B) was still higher than at the start of the year, indicating that capital has broadly flowed back into exchange markets compared with prior lows. �

coinglass

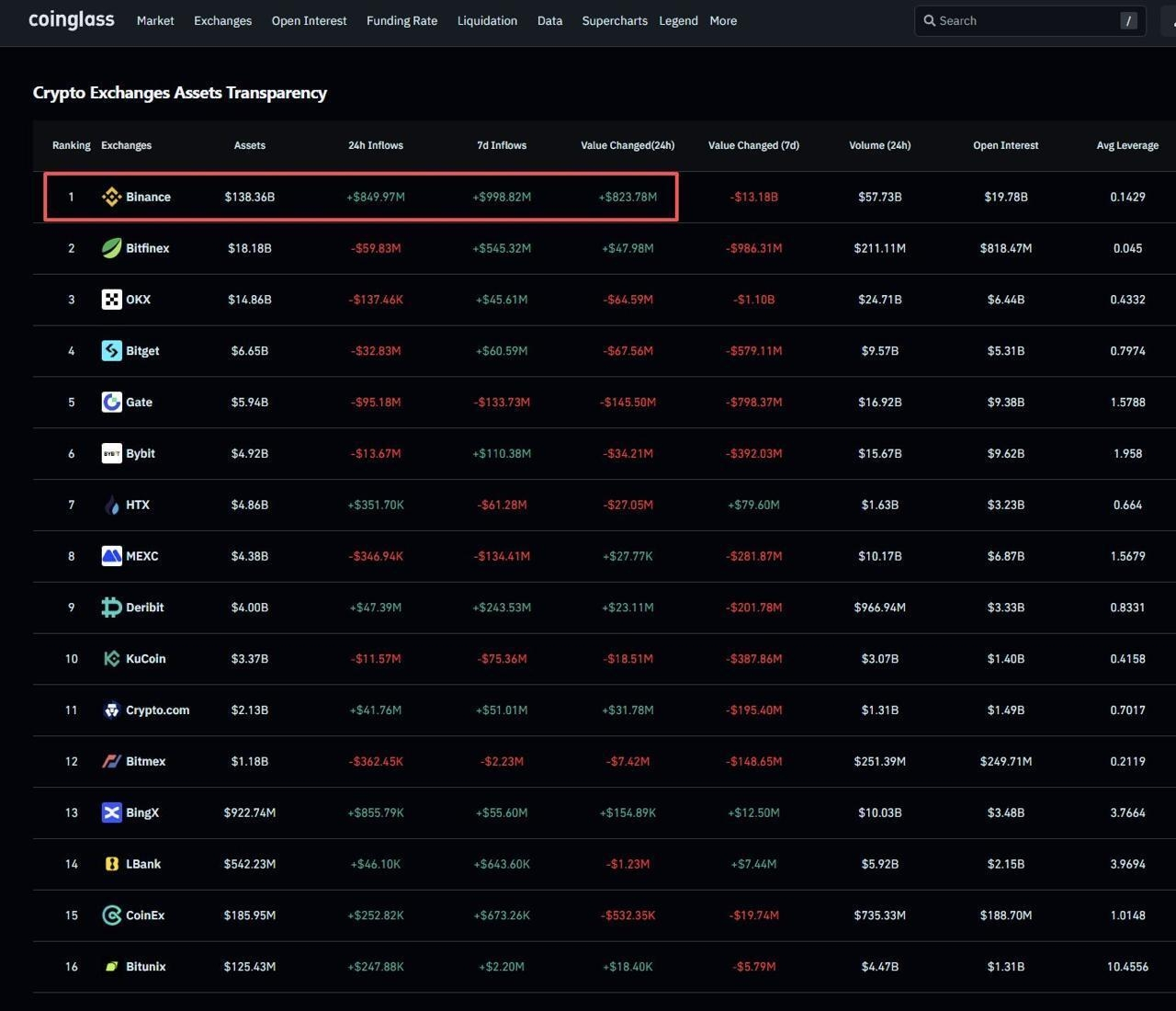

🔄 Strong Binance Inflows & Volume

Binance remains the dominant liquidity hub globally, with trading volume and market share far exceeding most competitors. The platform’s share of derivatives volume is among the highest worldwide, reflecting significant inflows of trading capital and depth for executing large trades. �

coinglass +1

📉 Leverage Still Suppressed

Despite the return of capital and elevated volumes:

• Open interest and leveraged exposure have not exploded back to prior extremes, and periods of deleveraging (sharp trimming of positions, especially after corrections) show that traders are still cautious about taking large leveraged bets. Deep leverage — where traders borrow heavily to amplify positions — hasn’t sustained the same momentum seen in e.g., past bull runs. �

coinglass

📌 What This Means

Capital into exchanges + strong volume ≠ high leverage

Traders and institutions are deploying capital back into exchange markets — particularly on deep-liquidity venues like Binance — but the composition of that activity has shifted. Rather than exceptionally high leveraged directional bets, more capital may be tied to:

Hedging and risk management (e.g., basis trades, institutional flows)

Spot/hedge activity linked to ETFs and institutional demand

More balanced positions with lower funding costs and less risky exposures

In other words, liquidity and participation have revived, but risk appetite via borrowed leverage remains more tempered than in prior highly speculative cycles.