On the afternoon of February 10, 2026, at the White House, an important meeting took place between major banks and crypto companies to discuss the new bill.

The center of the debate is whether stablecoins (stable-value currencies, like USDT or USDC) are allowed to pay interest or rewards to users.

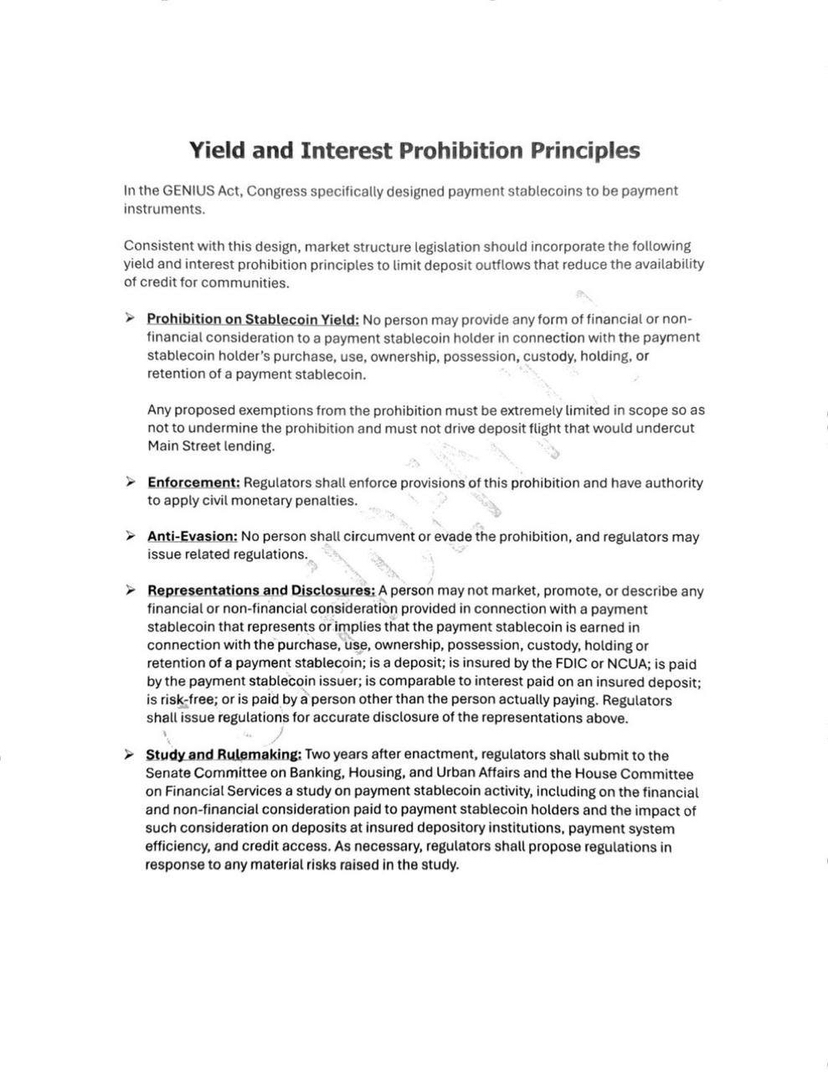

What is happening?

🔹On the bank's side (like JPMorgan, Goldman Sachs…): They worry that if stablecoins offer interest or rewards, people will withdraw money from bank accounts to move to crypto – leading to an imbalance in the traditional financial system.

🔸The crypto side (like Coinbase, Ripple…): They want to offer rewards to attract users, helping to develop a faster and more convenient digital payment ecosystem.

From the shared document (by journalist Eleanor Terrett), the bank proposed:

🔸Completely prohibit interest, profits, or any rewards for holders of stablecoins.

🔸Stablecoin is only used for daily payments, not for 'making money'.

🔸Prohibit advertising stablecoins as 'safe deposits' like banks.

🔸Severe penalties for violations, and only a few very small exceptions allowed, must be under strict control of the regulatory authority.

Today's meeting is considered 'more progressive' than the last, but no final agreement has been reached. Both sides are trying to find common ground before the deadline of 1/3/2026. It is highly likely that limited rewards will be allowed, under strict regulations.

How will it impact the financial market?

🔸Short term: If rewards are completely banned, the price of stablecoins and related tokens may slightly decrease due to loss of appeal, leading to a slowdown in crypto cash flow. Traditional banks may 'breathe a sigh of relief', maintaining stable deposit amounts, but the banking stock market may not experience large fluctuations.

🔸Long term: This is a battle for 'control over digital money'. If crypto wins (allowing limited rewards), it will drive innovation, making global payments faster and cheaper – benefiting users and the digital economy. But if banks win, the old financial system remains intact, potentially slowing the development of DeFi (decentralized finance), affecting the long-term price of BTC/ETH and altcoins.

🔸Overall: The global financial market could be more stable if there are clear regulations, reducing the risk of fraud. But if the debate drags on, it could cause price volatility in crypto (short-term dip due to FUD), and affect investor confidence in digital USD.

This is an important step for crypto to integrate with traditional finance – hopefully, it will yield good results for everyone!

What do you think? Should stablecoins have rewards to be more attractive? Or are banks right to be worried?

Comment to share your opinions, tag friends to join the discussion...