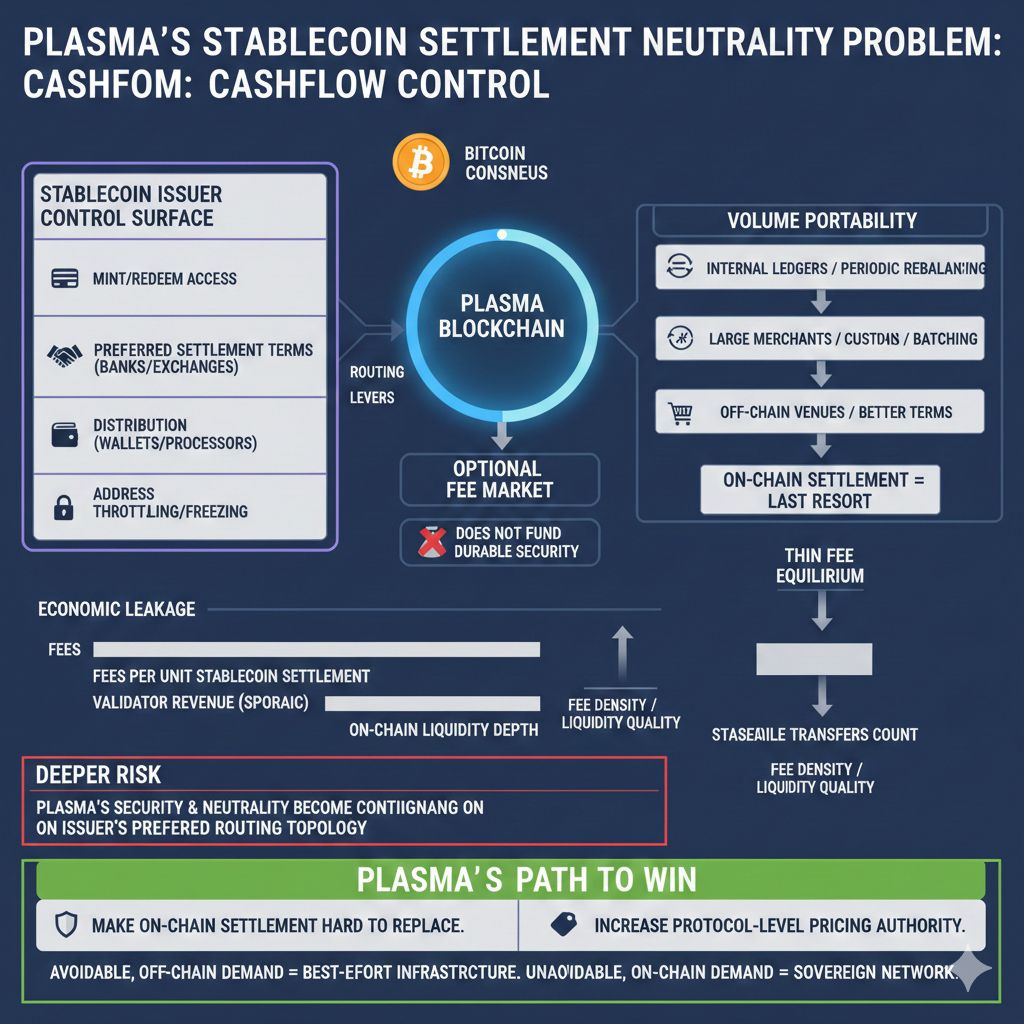

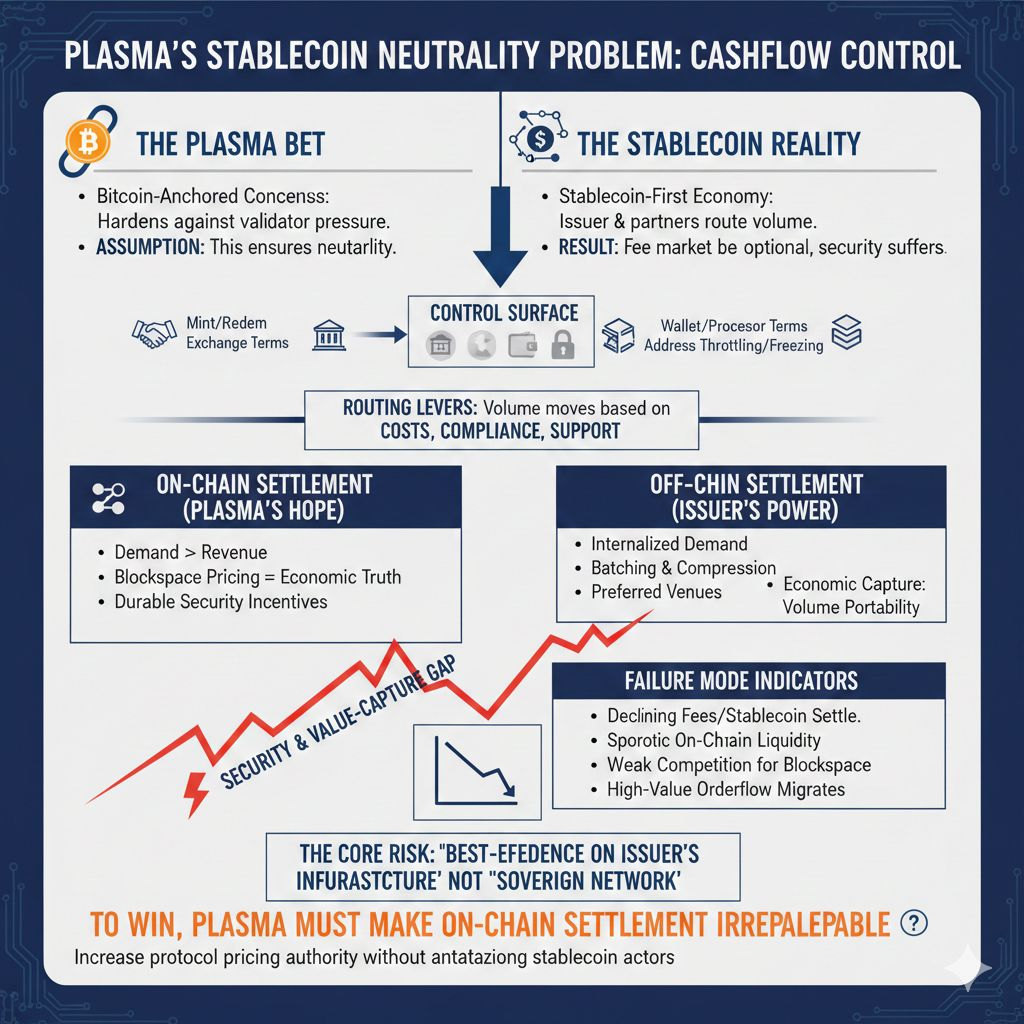

Plasma is making a bet many people will misprice: Bitcoin-anchored consensus can harden the chain against certain validator-level pressures, but it cannot guarantee neutrality in a stablecoin-first economy where the main stablecoin issuer and its top partners decide where volume actually settles. If the dominant gas unit is a stablecoin, and the deepest liquidity and orderflow are stablecoin-native, then the economic “governors” are whoever can route minting, redemption, distribution, and compliance at scale. Plasma can stay technically secure while its fee market becomes optional, and optional fee markets do not fund durable security incentives.Here is the control surface that matters. Stablecoin issuers control who gets high-trust mint and redeem access, which banking partners and exchanges get preferred settlement terms, which wallets and processors get distribution, and which addresses can be throttled, frozen, or excluded. That is not an attack, it is basic issuer operations. But when those permissions and integrations are concentrated, they become routing levers. If a major exchange or payment processor is told, explicitly or implicitly, “settle here for better costs, better compliance posture, faster support, or safer redemption,” the volume moves without Plasma changing a single line of code. In that world, consensus anchoring protects history, but it does not protect the cashflow that pays validators.Plasma’s risk is a security and value-capture gap created by volume portability. A normal fee market converts on-chain demand into revenue and makes blockspace pricing the protocol’s economic truth. In a stablecoin settlement chain, the most valuable demand can be internalized. Exchanges can net transfers inside their own ledgers and touch the chain only for periodic rebalancing. Large merchants can route through custodians or processors that batch and compress activity. Market makers can concentrate liquidity on the venue that offers the best redemption reliability and compliance guarantees. None of these behaviors require drama or a “run,” they only require a few high-volume actors deciding that on-chain settlement is a last resort rather than the default.This is where Plasma’s stablecoin-first gas design becomes a constraint, not just a UX win. If gas is paid in the same asset whose issuer controls key gateways, then the protocol is pricing blockspace in a unit that has an external policy layer. The issuer can push gas sponsorship into partner channels, encourage off-chain netting, or steer high-volume flows to a rival settlement venue that offers better commercial terms. Plasma might still process many transactions, but if the highest-value transfers and the tightest liquidity loops are increasingly settled elsewhere, the chain’s fee equilibrium gets thinner. Thin fee equilibrium means weaker validator revenue, weaker competition for inclusion, and weaker long-term confidence that the protocol itself captures the value of the activity it hosts.

You can actually observe this failure mode before it becomes obvious. The tell is not a consensus incident, it is a revenue reality: declining fees per unit of stablecoin settlement, validator revenue that depends on sporadic bursts rather than steady demand, shrinking on-chain liquidity depth relative to off-chain or competing venues, and less meaningful competition for blockspace as high-value orderflow migrates. If Plasma’s stablecoin transfers grow in headline count while fee density and on-chain liquidity quality stagnate, that is economic leakage, not adoption.Bitcoin anchoring still matters, but it is one axis. It can raise the cost of rewriting history or coercing validators, yet Plasma’s core challenge is whether stablecoin-native actors are forced to reveal their demand on-chain. If those actors can keep the profitable parts of settlement and liquidity off-chain, while only using Plasma as an occasional clearing layer, then “neutral infrastructure” becomes “best-effort infrastructure.” Plasma does not get to vote on the issuer’s partner graph, and that graph is where the real governance happens in stablecoin rails.The honest risk is deeper than issuer freezes. The deeper risk is that Plasma’s long-term security budget and perceived neutrality become contingent on staying inside an issuer’s preferred routing topology. Even without explicit capture, there is economic capture: the protocol cannot credibly compel issuers to keep volume on-chain, but issuers and their partners can credibly deprioritize the chain whenever cost, compliance, or commercial strategy shifts.For Plasma to win, it has to make on-chain settlement hard to replace, not just easy to use. That means creating reasons why large issuers, exchanges, processors, and market makers cannot get the same outcome through internalization, batching, or migration to a different venue with better terms. That is a narrow path, because Plasma must increase protocol-level pricing authority without antagonizing the very stablecoin actors whose routing decisions determine whether the chain is economically alive. If it fails, it will not fail loudly. It will remain anchored, continue producing blocks, and quietly lose the only thing that turns a stablecoin rail into a sovereign network: unavoidable, on-chain demand that pays for its own security.