I’ve been trying to make sense of why stablecoin infrastructure is suddenly getting discussed like serious financial plumbing instead of a niche crypto curiosity. My first instinct is to assume it’s just another cycle of hype, but the mix of rising usage and tightening rules makes that harder to dismiss. Once stablecoins start moving through payroll, merchant settlement, and cross-border transfers, the question isn’t just “Does it work?”—it’s “Does it stay reliable when things get messy?” McKinsey says stablecoin activity has surged, with annual transaction volume topping $27T in recent data, and points to 2025 as a realistic turning point for tokenized cash in payments and treasury. What’s changed on the policy side is the vibe: regulators aren’t debating whether stablecoins should exist—they’re zeroing in on reserves, redemption rights, disclosures, and ongoing supervision, especially in major markets.

In that backdrop, Plasma’s institutional story starts to feel coherent to me, even if I keep a healthy skepticism about any new chain’s promises. A research report from DL News describes Plasma as a settlement-focused network that treats stablecoins as first-class building blocks and centers features like gasless transfers, stablecoin-based fees, and sub-second settlement on purpose, not as add-ons. That list sounds technical, but the underlying intent is plain: make moving “digital dollars” feel as boring as moving dollars should feel.

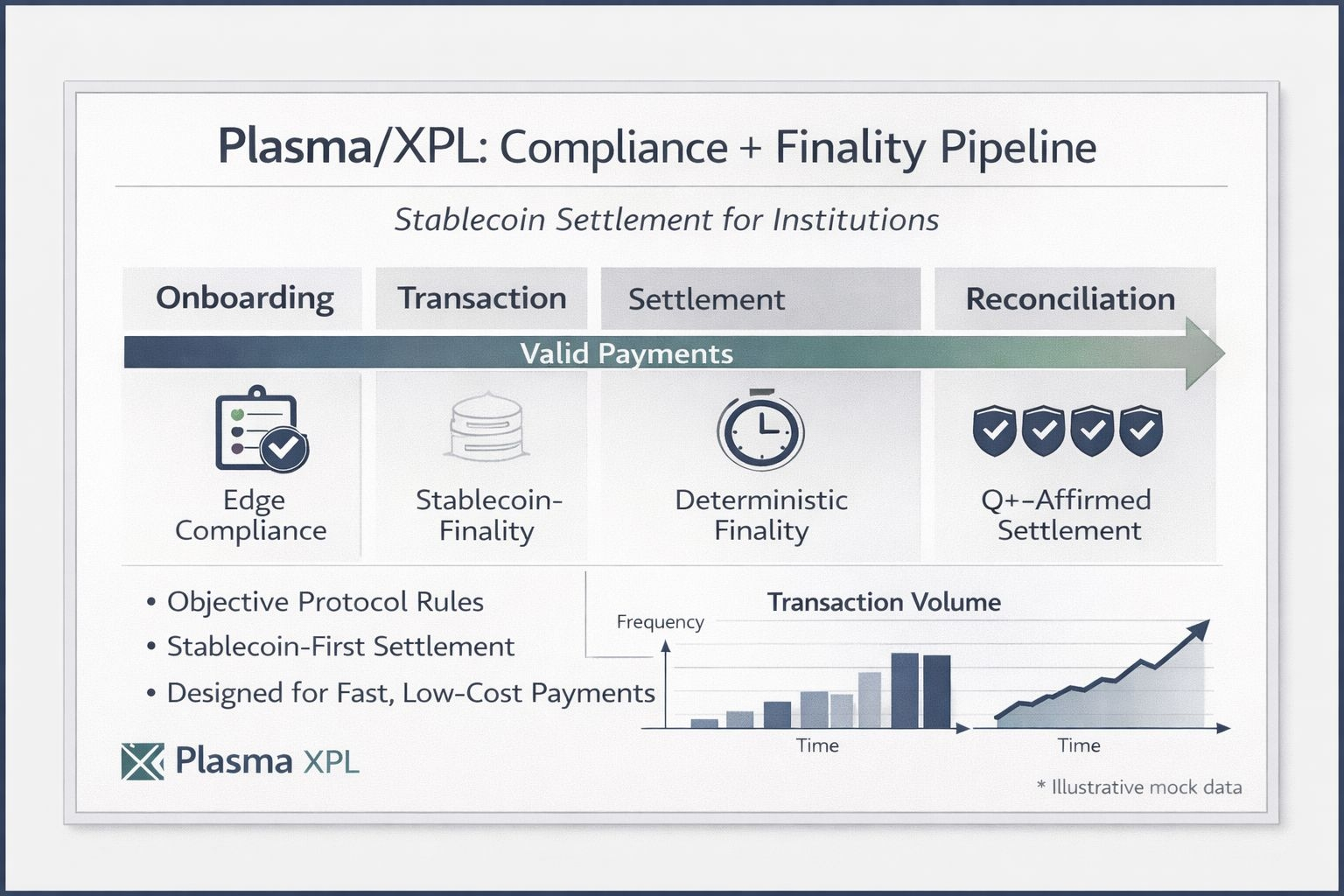

The first constraint is compliance. Institutions don’t get to opt out of monitoring, audits, and sanctions screening, and systems that ignore that reality don’t scale in regulated environments. I used to think this automatically meant a closed network with discretionary control, but I’ve come to see a more workable split: keep the base layer’s rules objective and predictable—valid payments go through because they meet the protocol—and do the identity and policy work at the edges, where firms already have onboarding, reporting, and legal responsibility. It doesn’t make compliance painless, but it avoids baking ad hoc intervention into the settlement engine itself.

The second constraint is finality. In consumer apps, waiting is annoyance; in treasury operations, waiting is exposure. “Final” just means that once a payment is accepted, it doesn’t drift back into doubt, so balances can update, goods can ship, and reconciliation doesn’t become a daily headache. When global remittance flows are estimated at $860 billion in 2023, even small reductions in delay and uncertainty matter because they compound across huge volumes.

Neutral security is the third constraint, and it comes down to one blunt question: can a valid payment be stopped because someone dislikes the sender, the receiver, or the jurisdiction? Plasma leans on a Bitcoin-anchoring approach—periodically checkpointing its state to Bitcoin—so rewriting its history is meant to be as hard as rewriting Bitcoin’s history. What surprises me is how conservative that sounds as an institutional posture. It’s basically an attempt to make the “rules of settlement” feel final, legible, and hard to bend, while still leaving room for regulated actors to meet their obligations where they actually interact with users.