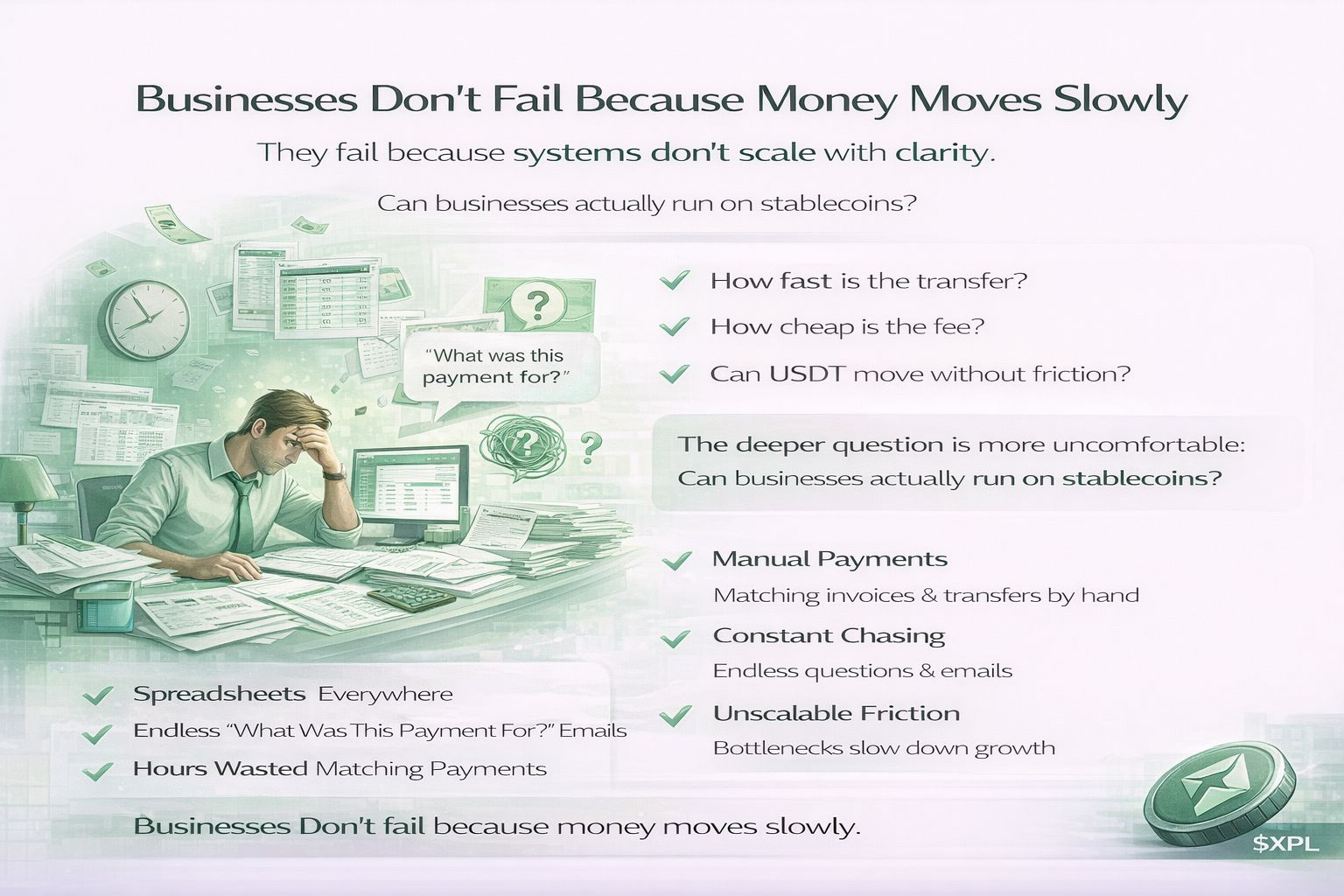

Imagine running a company

where every payment needs manual checking.

Spreadsheets everywhere.

Emails asking, “What was this payment for?”

Hours wasted on matching numbers.

Good businesses don’t fail because money moves slowly.

They fail because systems don’t scale with clarity.

Most discussions around stablecoins stop at the surface. How fast is the transfer? How cheap is the fee? Can USDT move without friction? Those questions matter, but they are not what decides whether stablecoins become real financial infrastructure or remain a crypto-native tool used by a narrow group of power users.

The deeper question is more uncomfortable: can businesses actually run on stablecoins?

When you look at real finance, money is never just money. A payment is always attached to meaning. It represents an invoice being cleared, a salary line item, a supplier settlement, a refund, a subscription renewal, or a tax-related transaction. Traditional payment systems did not win because they were fast. They won because they carried structured information that accounting teams, auditors, and operations staff could understand and trust.

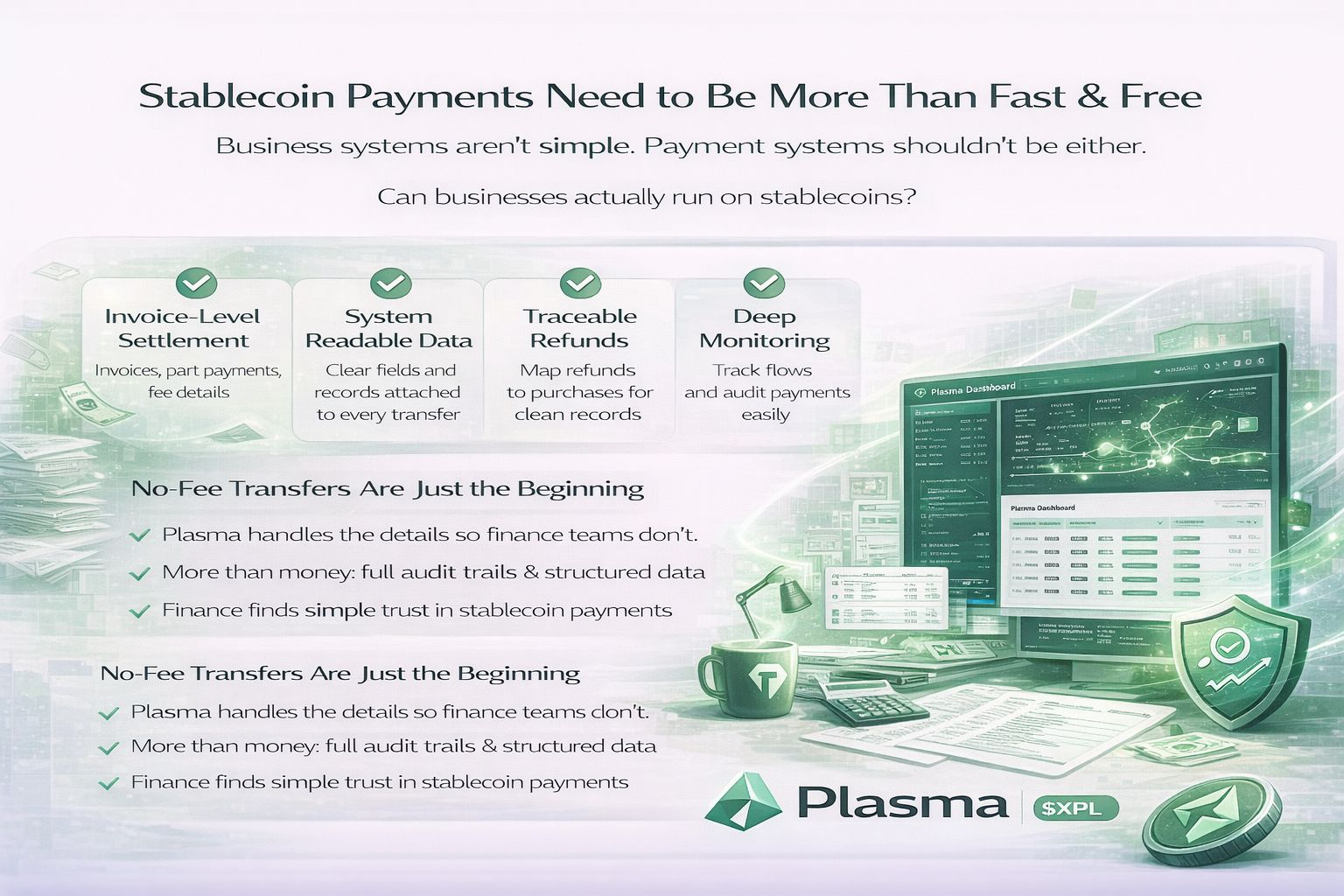

This is where I believe @Plasma real opportunity sits — not in value transfer alone, but in turning stablecoin transfers into data-rich, operable payments.

Plasma already checks many of the obvious boxes. Zero-fee stablecoin transfers, a stablecoin-first architecture, predictable execution, and a clear direction toward real-world payment rails. Those features make Plasma competitive. But competitiveness is not the same as inevitability. The difference between a good crypto rail and lasting payment infrastructure is whether finance teams feel safe relying on it at scale.

In the real world, a business does not ask, “Did the money arrive?”

It asks, “What was this payment for, and can I reconcile it automatically?”

Today, most stablecoin payments are blind. Funds move from wallet 1 to wallet 2, and the chain records that it happened. But when a marketplace pays ten thousand sellers, it doesn’t need ten thousand transfers. It needs ten thousand labeled transfers each tied cleanly to an order ID, a fee calculation, a refund condition, and a settlement record. Without that structure, humans are forced into spreadsheets, manual checks, and support tickets. Humans do not scale.

This is why traditional finance invested decades into messaging standards. Not because banks love bureaucracy, but because structured payment data eliminates exceptions. Exceptions are expensive. They create delays, errors, disputes, and hidden operational costs that dwarf transaction fees. Businesses would rather pay higher fees than deal with unpredictable reconciliation failures.

Stablecoins, as they exist today, still generate exceptions.

@Plasma has the chance to change that by treating payment data as a first-class citizen, not an afterthought.

Imagine stablecoin transfers where reference fields, structured metadata, and traceability are not optional add-ons but part of the protocol’s core design. Not a loose memo field read by humans, but system-readable data that accounting software can ingest automatically. That single shift would move stablecoins from “crypto payments” into something CFOs can approve without fear.

Invoice-level settlement is where this becomes real.

Most global commerce runs on invoices. Every invoice has identifiers, dates, partial payments, adjustments, and settlement rules. A stablecoin rail that can natively express those relationships changes the entire equation. Businesses could accept stablecoin payments and automatically match them to invoices. Suppliers would instantly know which order was paid. Customer support could trace a refund to a specific checkout. Auditors could verify flows without guesswork.

This is not hype. It is adulthood.

Refunds are another place where data matters more than speed. A refund is not just sending money back. It is linking a new transaction to a previous one in a provable, auditable way. Traditional payment systems handle this because refunds are first-class operations. Stablecoins often treat refunds as ad-hoc transfers, which increases risk and confusion. With proper payment context, refunds become routine instead of dangerous.

Operational visibility ties everything together.

The best payment systems are observable. Operations teams can monitor flows, trace failures, detect anomalies, and explain exactly what happened when something goes wrong. Plasma’s direction toward built-in observability — transaction tracing, flow tracking, and real-time monitoring — aligns perfectly with this reality. A system that cannot be operated safely will never be trusted, no matter how cheap it is.

What’s important is that this story isn’t just for enterprises.

Better payment data improves user experience too. Clear receipts. Transparent refund status. Payments that map cleanly to purchases. Fewer “where is my money?” moments. Less fear. Less friction. Fintech products feel simple not because they are simple, but because complexity is handled invisibly behind the scenes. Reconciliation systems are boring — and that is precisely why they work.

If Plasma succeeds here, it won’t look like a viral chart or a speculative narrative. It will look like quiet adoption. Businesses using stablecoins because reconciliation is easy. Marketplaces running payouts without drowning in edge cases. Finance teams trusting on-chain settlement because it behaves like the systems they already understand only faster, cheaper, and global.

Stablecoins become real money not when they move faster, but when they carry meaning.

@Plasma has an opportunity to be the chain that makes stablecoin payments legible to finance not just transferable to wallets. When a transfer becomes a payment, and a payment becomes operable infrastructure, stablecoins stop being crypto experiments and start becoming part of the global financial system.

That transition won’t be loud.

But it’s the kind that lasts.