The most confusing part of this market today is: you clearly see $BTC a small drop (-0.57%), $ETH and it can still turn positive (+0.98%), yet fear and greed are still hovering at extreme fear. This combination is familiar to veteran players—it's not that the bulls have returned, it's that the 'selling pressure has paused', and the market is waiting for the next bombshell: can spot demand catch up, will macro data give another kick, and will the policy knife actually fall.

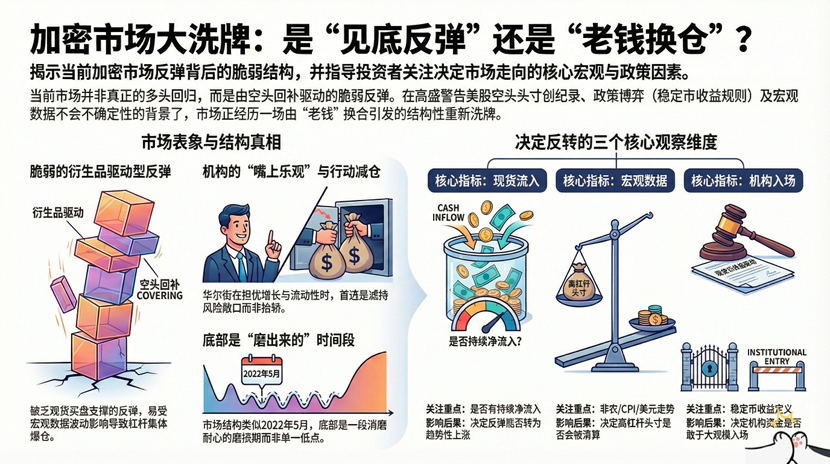

Let's lay out the conclusion first: whether this round of rebound can continue, without looking at the flashy K-lines, the core issue is just one thing—whether there is real buying interest returning in the spot market. If the spot doesn't pick up, no matter how much derivatives are pulled, it’s just a weak rebound made up of 'short covering + market maker hedging'; once non-farm/CPI deviates from expectations, if the dollar and US Treasury yields shake, leverage will collectively kneel again. You will find that the market structure is increasingly resembling that flavor of May 2022: it looks like it has already dropped deeply, but the bottom is usually not a point, but a period of 'grinding until you don’t want to look at the market'.

Why do I say 'old money is changing positions'? Because the traditional market is even more absurd: Goldman Sachs warns that hedge funds are exhibiting record short-selling signs on U.S. stocks, coupled with uncertainty in earnings/valuation brought about by AI shocks, risk appetite is shouting 'bottom-fishing' while quietly reducing positions. You just need to understand one logic: when Wall Street starts to fear growth, volatility, and liquidity simultaneously, their first choice is always to reduce risk exposure, not to lift you up. So you will see: institutional sentiment in crypto is 'optimistic in words,' but market actions do not cooperate — this is why many people feel that 'institutions seem overly optimistic,' but prices just can't break out of the trend.

Looking at the policy line, the most crucial thing recently is not who is bullish or bearish, but 'how the rules are written.' The market structure bill is reportedly likely to advance in a few months, but the biggest point of contention is four words: stablecoin yield. Banks do not want you to earn 'deposit-like yield' on stablecoins on-chain because that would siphon off deposits; the crypto industry cannot just hand over the 'yield' piece of the pie. So the White House is holding a meeting next Tuesday to try to untangle this deadlock again, and for the first time, large bank representatives will be sitting at the table — the significance of this matter lies not in one or two statements, but in whether stablecoins will be allowed to become substitutes for 'programmable deposits.' Once the rules tighten, it will be painful in the short term, but clearer in the long term: those who need to comply will comply, those who need to clear will clear, and the market will resemble a financial system rather than a casino.

At the same time, the Federal Reserve is also promoting limited access through 'bypassing legislation,' such as the so-called discussion of a 'streamlined main account': it may not give you a full pass but could provide a window to access part of the payment infrastructure. You can understand it as a sentence: regulators are slowly opening the door, but the key must be kept in their hands.

What's even more interesting is the wind direction: on one side, Federal Reserve Governor Waller says, 'The crypto craze triggered by Trump may be fading,' while on the other side, Trump is still loudly claiming that Waller can push economic growth to 15% and continues to criticize Powell. Do you understand? Politics is setting off fireworks while the central bank is tightening the faucet. This division itself will raise volatility, and when volatility rises, the first to die are always those highly leveraged and those 'selling volatility' — so derivatives are bearish, and ETH's short-term upward space is limited. This judgment is not surprising: it's not that I am not optimistic, but structurally, it does not allow it to proceed too smoothly.

Don't overlook the geopolitical side either: the probability of 'U.S.-Iran reaching a nuclear agreement before 2027' on Polymarket is hovering around 44%. The market's pricing of 'successful talks/failed talks' is actually pricing in risk premiums. If talks go smoothly, risk appetite warms up; if talks collapse, oil prices, the dollar, and interest rate expectations will tremble together, making it difficult for crypto to stand alone.

Meanwhile, there are still highlights on-chain. The signs of large holders continuing to accumulate BTC during the pullback are still present, and DeFi TVL has also seen a mild rebound, with protocols like Aave and Morpho, which cater to real demand, slowly building their foundations back up. The market is always like this: emotions die first, while structure lives later; when prices are at their worst, it is often when infrastructure is quietly being repaired. If you only watch the price, you will miss many 'preparation actions before trend turning points.'

And the hotspots have not stopped: MegaETH mainnet is launched, claiming 100,000 TPS with millisecond latency; Aztec's TGE is set for February 12; SushiSwap has started supporting Solana ecosystem token trading... These messages sound like 'narratives,' but behind the narratives is actually a more realistic matter: everyone is scrambling for the next round of 'liquidity entrance.' Performance chains, privacy chains, and cross-chain liquidity are all competing for 'where users default to exchange, where to use, and where to settle.' As the market enters a 'reshuffling period,' the entrance is more valuable than flashy tricks.

Speaking of 'settlement', I’d like to mention.@Plasma $XPL #Plasma (Don't get me wrong, it's not a call to action). My positioning on it is very simple: stablecoin settlement infrastructure. The value of this track in a high-volatility era does not lie in 'whether it rises or falls,' but in 'whether the channel is stable and settlement is secure.' But I don't want to overstate it: in the short term, it will still follow the market's fluctuations, and the stablecoin narrative cannot save it from the selling pressure when risk appetite collapses. I prefer to see it as an observation target: looking at its long-term value while not getting too carried away in the short term: waiting for real recovery in spot demand, policy framework to be implemented, and interest rate expectations to stabilize, only then can this 'service for stablecoins' chain more easily capture real incremental value.

Finally, here’s a framework closer to practical operations: in the coming weeks, you only need to focus on three things — first, whether there is sustained net inflow in the spot market (not just one or two days of replenishment); second, how the dollar and U.S. Treasury yields respond if non-farm payrolls/CPI significantly deviate from expectations (this determines whether leverage can survive); third, how the rules for stablecoin yields are ultimately set (this determines whether institutions dare to treat stablecoins as 'cash equivalents + yield assets' for allocation). As long as these three things do not warm up simultaneously, don't rush to announce 'the bull is back.'

One thing the market loves to do is reward you for chasing the rise with a rebound, then educate you with the next sharp drop that 'this is not a reversal.' Those who can traverse cycles are often not the best predictors, but the ones who can best control their impulses during these phases.