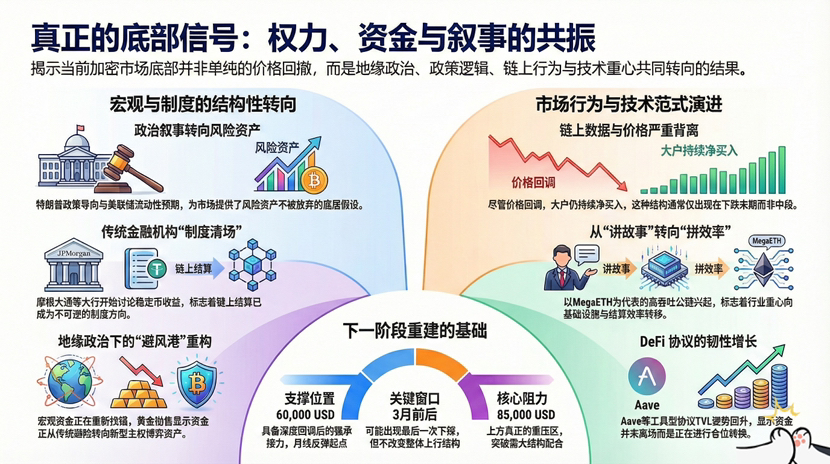

If you only focus on Bitcoin bouncing between 60,000 and 70,000, it’s easy to overlook one thing: the context of this decline is unlike any in the past. Geopolitical tensions are rising, negotiations between Denmark and the United States over Greenland have stalled, and Canada and France are directly establishing consulates, with the Arctic routes, energy, and sovereignty games beginning to come to the fore; on the other hand, the U.S. Treasury is pouring cold water on gold, stating that this looks more like a speculative sell-off than a systemic demand for safe-haven assets. Macro funds are not seeking refuge in traditional safe havens but are looking for new anchors.

Meanwhile, the political narrative has started to clearly tilt to the right. Trump openly declared, 'The Dow will hit 100,000 before the end of my term.' You may not believe such statements, but the signal behind them is clear: risk assets will not be abandoned, and balance sheets will not easily contract. Waller will not suddenly cut the balance sheet; the Fed's 'slow variables' still exist, providing the market with a fundamental assumption — liquidity is not an issue, the only issue is the pace.

Returning to the crypto market itself, the panic in prices and the behavior of funds have clearly diverged. On-chain data is honest; large holders are not selling off, but rather continually net buying amid the pullback, with multiple queues showing accumulation simultaneously. This structure often only appears in one phase during past cycles: at the end of a decline, not in the middle of one. The DeFi side is also intriguing; TVL has rebounded when price sentiment is very poor, and 'tool-like protocols' such as Aave and Morpho recorded moderate growth, indicating that funds have not left the market but are merely changing positions.

More importantly, the entire industry's 'center of gravity' is quietly shifting. The MegaETH mainnet is live, with 100,000 TPS and millisecond-level latency. Whether you believe it or not, the emergence of such public chains is itself sending a signal: the market has shifted from 'telling stories' to 'competing on throughput and efficiency'; Aztec is about to launch its TGE, and the privacy track is back on the table; SushiSwap is beginning to embrace Solana assets, and cross-chain liquidity is no longer just a slogan but a reality that must be addressed.

What many people often overlook is the dark line of stablecoins. The CFTC allows national trust banks to issue US dollar stablecoins under the GENIUS framework, and the White House is holding its second round of internal crypto meetings, focusing directly on 'stablecoin yields', with institutions like US Bank, JPMorgan, and Wells Fargo sitting at the table. This is not a trial; this is a formal institutional clearing before traditional finance enters the market. When banks start discussing 'how stablecoins can yield returns', it suggests they assume one thing: on-chain settlement is already an irreversible direction.

Viewed in this context, Bitcoin's price movement is no longer so agonizing. The selling pressure over the past four months has provided a sufficiently deep pullback; around 60,000 may not be the final bottom, but it is certainly a 'willing to absorb position'. Both the monthly and weekly charts show a rebound impulse, and a correction around the Lunar New Year is not unexpected; the 72,000 level on the 4-hour chart was quickly pushed back, indicating that the short-term structure is still a weak rebound, with 85,000 being the real heavy resistance. In other words, while short-term volatility is not lacking, it is time that is in short supply; another dip around March does not change the larger structure.

By the way $XPL . In the short term, it still cannot escape market sentiment; it gets hit when it rebounds and is also hit during declines. This is a commonality of settlement and infrastructure-type assets; however, in the current context where topics like 'stablecoin yields', 'on-chain settlement', and 'compliant issuance' are frequently put on the table, the value judgment of such things should not be defined by a week or two of prices. A short-term bearish outlook does not equate to long-term lack of value; it simply means the market hasn't reached the stage where it needs it.

After going through a few cycles, you'll understand that a true bottom is never confirmed by a single bullish candle but rather when local geography, policy, funds, and narratives all begin to tilt towards 'reconstruction'; price is merely the last variable to react. The current market is more like it's preparing for the next phase rather than wrapping up the previous one.

Take it slow, see clearly, and then act; this is often safer than rushing to take sides.