$BTC Many friends who do not want to hold Bitcoin ask Uncle Meow, "If I don't hold Bitcoin, can I just hold MSTR? Will the expected returns be higher in the future?"

The answer to this question is simple: "Returns will definitely be higher, but the premise is that you must endure through a deeper bear bottom." Without this mental preparation, I do not recommend getting into MSTR.

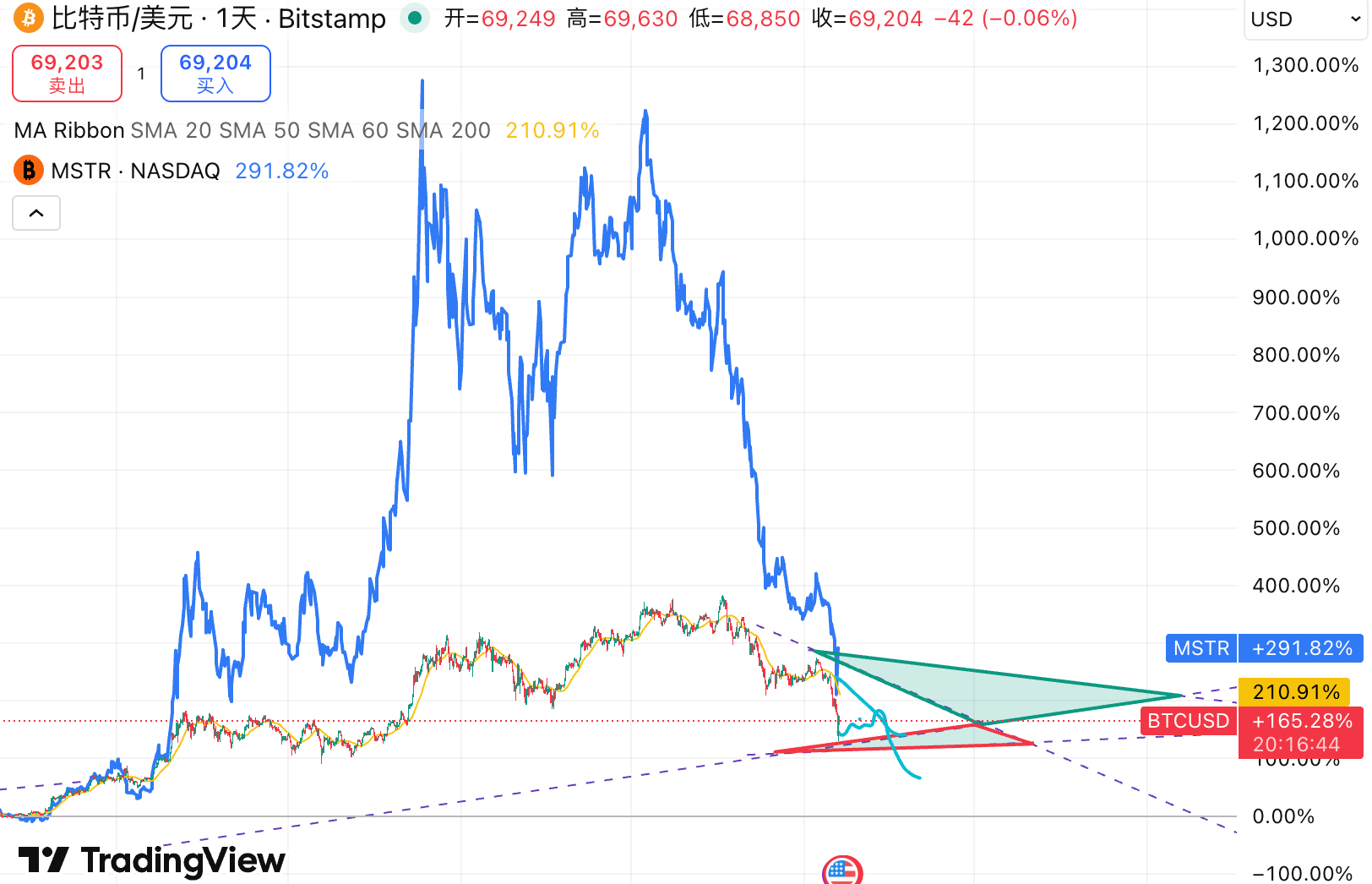

MicroStrategy was originally a software vendor, and later in 2020 began a full transformation into a BTC strategic reserve company, becoming the world's first "BTC asset management company." After five years of accumulation, they are currently the largest corporate holder of BTC, with an average holding cost of $76,000, and under the leadership of Saylor, their motto is to only buy and not sell.

1. MSTR is more like a leveraged Bitcoin.

After fitting the data, MSTR's trajectory essentially completely overlaps with Bitcoin's, just with a greater magnitude. This is closely related to their operational logic (which can also be understood as the logic of financing to buy Bitcoin).

MSTR's operational mechanism is mNAV (the ratio of market value to net asset value). MSTR has completely divested its software business and is now a machine that amplifies Bitcoin's price fluctuations using financial instruments, with its core business logic being 'premium'. Purchasing MSTR is essentially buying leveraged Bitcoin.

The logic behind this can be explained by the classic 'wine cellar theory': suppose MSTR is a wine cellar and BTC is the red wine stored within. If the market price of red wine is $100, and the transfer price of the wine cellar is also $100, then mNAV is 1; however, in a frenzied market sentiment, investors are unable to buy wine directly due to regulatory restrictions or believe that the custodian of the cellar (Saylor) will be able to produce more wine in the future, they are willing to pay $200 to buy this cellar. At this point, mNAV becomes 2, and the extra amount is the premium.

The higher the mNAV, the more insane the emotional value assigned by the market.

2. This premium model is a very perfect amplifier for price increases in a bull market (positive flywheel).

If mNAV is at a high level (high premium), MSTR will issue more stocks. At the same time, since the stock price is expensive, the company can exchange fewer shares for huge cash and immediately use this cash to buy Bitcoin. The magic is that, despite the increase in equity, due to the high premium, the number of Bitcoin obtained from the issuance grows much faster than the dilution speed of the equity, resulting in an increase in 'BTC per share' rather than a decrease (that is, the more shares of MSTR you buy, the proportion of BTC in the equity actually increases, equivalent to buying more BTC for less money). This increase in per-share value will ignite market sentiment, continuing to push up the mNAV premium, allowing the company to continue issuing at higher prices.

So this flywheel works like this: when Bitcoin's price rises, mNAV rises, equity increases, financing volume increases, and the total amount of Bitcoin purchased by MSTR increases, they continue to hold more Bitcoin; this model is very effective in an upward trend.

This is also the reason why MSTR can rise 30 times.

3. In a bear market, the decline of MSTR will be magnified, and this flywheel will also fail (even turning into a negative flywheel).

However, the only premise for this flywheel to operate is that the market is willing to pay a premium, meaning mNAV must be significantly greater than 1. Once mNAV falls back to 1 or even below 1, the flywheel will instantly fail, and investors will face the cruel 'Davis double kill'. If the price of BTC crashes, its premium will start to fail, the previous flywheel logic reverses, users will no longer be willing to pay a premium to buy MSTR's stock, leading to a decrease in MSTR's financing efficiency, equity containing BTC decreases, and a large number of users begin to sell MSTR, causing the flywheel to reverse and MSTR's stock price to plummet.

Moreover, we must also consider the boosting effect of short selling. MSTR issues a large number of convertible preferred notes to purchase Bitcoin, and those who buy these notes are often risk-free arbitrage institutions. To hedge the equity risk in the convertible bonds, these institutions will establish a large number of short positions in MSTR in the secondary market while buying the bonds.

This creates a dangerous negative feedback loop: when the stock price falls, in order to maintain the hedging ratio or because shorts are profiting handsomely, institutions will increase their short-selling efforts; the deeper the stock price falls, the weaker MSTR's ability to finance through stock issuance to repay debts or buy coins becomes; if forced to issue stocks at a low price, it will severely dilute existing shareholders' equity, further driving the stock price down. This short-selling mechanism inherent in the financing structure will create a huge selling pressure vortex during the down cycle, even if the company does not sell coins, the stock price will plummet.

4. So, will MSTR go bankrupt, and will it sell Bitcoin to repay debts?

In fact, MSTR is hard to go bankrupt; Uncle Meow believes that those waiting for MSTR to go bankrupt lack data awareness.

Their debt duration management is very good, with a long safety window; this is the core of their 'exchanging time for space' strategy. According to the latest debt structure analysis, MSTR's first large-scale debt principal repayment will not be until September 2028, with subsequent debts extending to 2029, 2030, and even 2032. This means the company has completely shielded itself from repayment pressure for nearly three years in the future. Therefore, even if Bitcoin enters a long bear market or consolidation period, MSTR will not be forced to sell Bitcoin at low prices.

Long-term debt arrangements provide the company with a significant buffer time; even if there are short-term paper losses, MSTR can withstand debt pressure.

5. When can we get into MSTR?

The logic is simple, wait for MSTR to start when it is consolidating at the bottom.

First, the fundamentals of MSTR itself have not changed; the current crash of MSTR is more a regression of the premium in the valuation model. MSTR's logic of survival does not depend on the rise and fall of Bitcoin, but on whether it has the ability to maintain 'financing capacity and the ability to avoid bad debts'. However, over the next five years, MSTR locks in long-term debt due in 2028, utilizes reserves to lock in cash flow, and combines perpetual capital to secure financing channels, making MSTR's asset-liability structure healthy. As long as Bitcoin does not go to zero, and as long as Saylor can survive the bear market, MSTR will be fine.

However, confirming the bottom still takes time, and the real market bottom is always a horizontal range. Before the bottom is truly confirmed, remain calm.