Today, two major hotspots are affecting global market nerves: on one side, the US-Iran negotiations in Oman have fallen into an awkward situation of 'talking without progress', where Trump clearly displays military posturing but is reluctant to take action; on the other side, China's regulatory authorities are rarely taking a 'dual approach', with eight ministries intensifying pressure on virtual currency regulation, while the Securities Regulatory Commission has opened the door for domestic assets to issue asset-backed securities tokens abroad. These seemingly unrelated events both conceal deep-seated power struggles among various forces. Combining the latest real-time data and dynamics, we will dissect the core logic one by one.

Part One: The US-Iran-Oman negotiations are at an impasse, and Trump's 'wait-and-see' mentality has four core aspects.

First, looking at the latest progress in U.S.-Iran negotiations—no progress is the most real progress.

The latest statements indicate that the Iranian foreign minister has made it clear that both sides have only reached a consensus on 'continuing negotiations' without involving any substantive issues; Trump has also simultaneously stated that 'negotiations will continue next week.' This 'repeated tug-of-war' posture has led many to wonder: why is Trump, who previously easily resorted to 'extreme pressure' and 'lightning strikes,' so reluctant to take decisive action against Iran? Considering the recent situation and real-time dynamics, Trump's caution has long been written into his operational logic.

1. A clever strategy that meets an 'impenetrable' Iran.

Trump's operational principle has always been 'to exchange the greatest benefits for the least cost.' The two previous landmark operations confirm this: last June's 'Midnight Hammer Operation' was initiated after he witnessed the Israeli military's complete suppression of Iran's air defense system and gained absolute advantage; during the capture of Maduro, he even preemptively subverted some of his subordinates, utilizing the geographical advantage of Caracas by the sea to achieve a rapid strike at a low cost.

However, today's Iran is no longer an object that Trump can 'take advantage of': Internal unrest in Iran has been thoroughly suppressed, and the Revolutionary Guards are in a state of high alert, with defenses tight and with no obvious vulnerabilities. As early as January 22, military analysts pointed out that even if the U.S. aircraft carrier strike group is fully deployed, the 'best opportunity for action' against Iran has already been missed—no matter how adept Trump is at speculation, he will not touch the 'hard bone' that is 'difficult and thankless.'

2. Fear of a 'Carter-style tragedy'; significant casualties among U.S. troops are the 'red line of red lines.'

For Trump, the core taboo of the Iranian issue has never been 'whether we can win or not,' but 'whether there will be significant casualties among U.S. troops.' If a large number of U.S. military casualties occur during the conflict, it would not only directly destroy his presidential prestige but may also repeat the Iranian tragedy of the Carter administration—back then, the Carter administration's mishandling of the Iranian hostage crisis directly led to its failure to be re-elected, becoming a 'negative teaching material' in American politics.

This is also why, even though Trump has deployed a large number of troops in the Middle East, displaying a 'ready for battle' posture, he has always been unwilling to take substantial steps. For him, the best outcome is to force Iran to make concessions in negotiations through military intimidation and extreme extortion, reaching an agreement favorable to the U.S.; rather than risking getting bogged down in Iran, which is 'tightly organized and powerful'—it should be noted that Iran's overall strength and defensive capabilities far exceed those of Venezuela, and rash actions would only lead to losses.

3. Missile inventory 'rises and falls'; there is a lack of assurance for a 'decisive strike.'

Another key constraint is the comparison of missile inventories and production capacities between the two sides, which no longer has an 'overwhelming advantage.' During last June's conflict, Israel's Iron Dome system consumed a massive amount of inventory to intercept missiles launched by Iran, and the U.S. military also consumed a large number of air defense missiles. Although both sides have been replenishing inventory since then, the situation has already changed:

On the Israeli side, although they signed a multi-billion dollar contract with Rafael Advanced Defense Systems in November 2025 to significantly increase the production capacity of the Iron Dome's Tamir interceptor missiles before 2026, adding two automated assembly lines and using U.S. aid funds to replenish the ammunition base, the increase in capacity has not yet fully materialized, and inventory replenishment is still ongoing.

On the Iranian side, missile inventories have been quickly replenished. According to assessments by the International Institute for Strategic Studies in 2026, Iran currently possesses over 3,000 ballistic missiles, including 1,500 short-range, 1,000 medium-range, and 500 long-range, having also test-fired its first intercontinental missile in January 2026, covering a range of 5,500-12,000 kilometers, achieving 'meter-level' accuracy with the assistance of the Beidou system, and missile production capacity has been fully enhanced.

In the absence of confidence in a 'decisive strike to destroy Iran's core defenses and cause rapid collapse,' Trump's caution is essentially a matter of 'not wanting to gamble and not daring to gamble'—after all, once the conflict becomes a stalemate, a missile attrition battle will only put the U.S. at a disadvantage.

4. The negotiations themselves are merely a 'stalling tactic'; substantive consensus cannot be reached.

In fact, one of the core reasons Trump is willing to 'drag out negotiations' is that the negotiations themselves are a stalling tactic, and the core differences between the two sides have been irreconcilable from the start, making it impossible to reach substantive results.

Before the Oman talks, the White House made it clear that 'achieving zero nuclear capability for Iran' is a core position repeatedly emphasized by Trump; however, Iran's stance is equally firm, explicitly stating in negotiations that it will never accept the condition of 'no uranium enrichment activities'—the uranium enrichment issue serves as a 'deadlock' for both sides; if no agreement is reached, it means that no substantive consensus can be discussed.

More critically, ballistic missiles have now become a more important defensive pillar for Iran than uranium enrichment. Even if the U.S. makes concessions on the uranium enrichment issue, it will undoubtedly demand restrictions on Iran's ballistic missile development, which is precisely the bottom line that Iran will never compromise on. On one side is the strong demand for 'zero nuclear capability,' and on the other side is the firm stance of 'defending its own right to self-defense.' Such negotiations are destined to only 'go in circles.'

Extension: In the subsequent direction of the Iranian situation, two 'potential turning points' are worth noting.

Considering the current situation, the subsequent development of the Iranian situation is likely to revolve around two 'potential turning points' and may also be the timing for Trump to 'take action again.'

1. Iran is experiencing internal chaos again: Previously, Iran had experienced unrest, which was quickly suppressed. However, if chaos breaks out again due to economic and livelihood issues, leading to a decline in internal cohesion and defensive vulnerabilities, it is likely to become the best opportunity for Trump to take action.

2. Israel takes the lead in 'going wild': Just like last year's conflict, if the Netanyahu government cannot help but take the first action against Iran, attacking core facilities such as Iran's power grid and oil exports to deplete Iran's defensive capabilities and trigger internal chaos, Trump will likely once again 'reap the benefits' by intervening after Iran is severely weakened, achieving 'low-cost control.'

Second part: The polarized situation of virtual currency regulation, the underlying logic of tightening and guiding flows.

At the same time that U.S.-Iran negotiations are dragging on, on February 6, Chinese regulatory authorities issued two heavyweight documents, staging a 'polarized' scene in virtual currency regulation: on one side, eight departments jointly intensified high-pressure regulation, further expanding the scope of the crackdown; on the other side, the Securities Regulatory Commission opened a door allowing domestic assets to issue asset-backed securities abroad.

Many people are confused: why is there a push for both 'tightening controls' and 'guiding flows'? This seemingly contradictory operation is actually a manifestation of the regulatory authorities' 'refined governance,' hiding three core considerations (based on the latest regulatory documents and real-time market data interpretation).

First, looking at 'tightening controls': Eight departments' high-pressure regulation, with the scope of the crackdown further upgraded (including real-time data).

On February 6, the People's Bank of China, the Securities Regulatory Commission, and eight other departments jointly issued a notice (on further preventing and addressing risks related to virtual currencies), continuing the previous high-pressure regulatory stance towards virtual currencies, and further expanding the scope of the crackdown. The core control points are as follows:

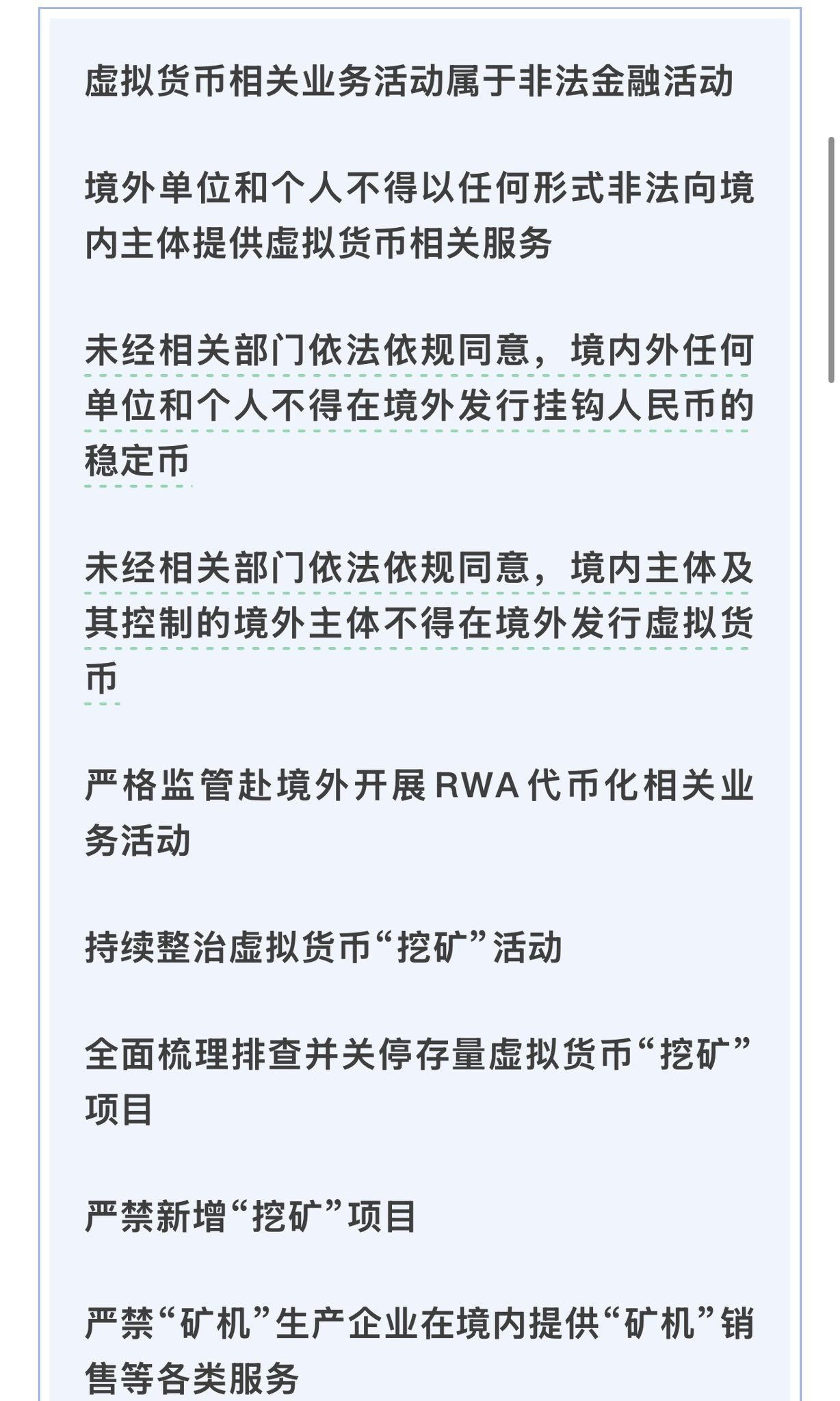

1. A comprehensive ban on related services: No virtual currency services may be provided to entities within the territory of ZA, no issuance of RMB-pegged stablecoins abroad, and no activities in 896.

\ Issuing virtual currencies abroad, continuing to comprehensively rectify virtual currency mining activities;

2. Expanding the scope of crackdown: Clearly stating that foreign entities are not allowed to issue RMB-pegged stablecoins, and foreign entities controlled by foreign entities are also prohibited from issuing virtual currencies—compared to before, it has further blocked loopholes for 'cross-border regulatory evasion.'

3. Refining control details: Market regulatory authorities clearly require that the registered names and business scopes of enterprises and individual businesses must not contain terms such as 'virtual currency,' 'cryptocurrency,' 'stablecoin,' or 'RWA,' thoroughly blocking the space for 'grey area' activities.

4. Strengthening comprehensive regulatory oversight: Financial institutions are prohibited from providing account opening, fund transfer, and other services for virtual currency-related businesses. Intermediaries and information technology service providers are not allowed to provide services for RWA tokenization activities without consent.

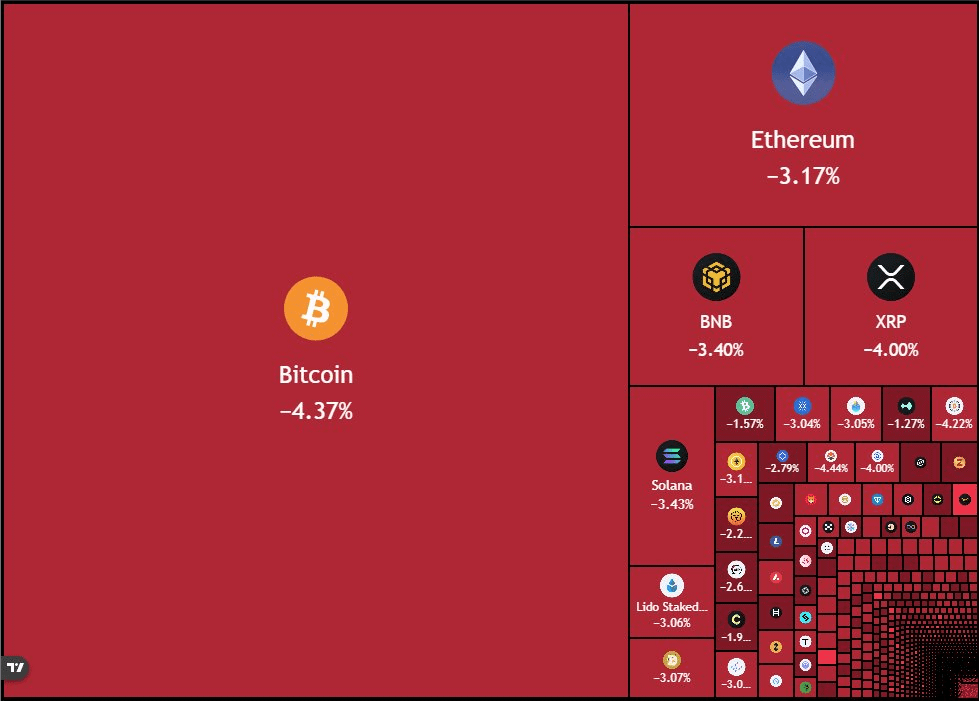

The issuance of this document also directly impacts the global virtual currency market: On February 6, Bitcoin plummeted to around $60,000, marking a new low in 16 months; according to real-time data from Coinglass, over 400,000 people were liquidated within the past 24 hours, with the liquidation scale of long positions in various tokens reaching $1.703 billion, and market panic spread.

It is worth mentioning that a highly dramatic event also occurred that day: The cryptocurrency exchange Bithumb mistakenly distributed 620,000 Bitcoins to users (instead of the previously rumored 2,000), and within 35 minutes after the distribution, 1,788 Bitcoins were sold by users, with the remaining portion being urgently recalled. This operational error is also considered one of the reasons for Bitcoin's sharp decline that day, with many netizens joking, 'Once again proving that the world is a huge makeshift stage.'

The core reason for the regulatory authorities to continue tightening controls is that since 2025, the trend of virtual currency trading speculation has seen a resurgence domestically. Many criminals have used virtual currency, RWA, and mining as a pretext to engage in illegal fundraising, pyramid schemes, and other illegal activities, severely harming public property safety and disrupting financial order. Previously, thirteen departments held coordination meetings to reiterate prohibitory policies, and seven associations had issued risk warnings. This document from the eight departments is a strong suppression of such 'resurgence' signs.

Looking at 'guiding flows': The Securities Regulatory Commission's opening is not a relaxation, but rather 'precise guidance.'

Just one hour after the eight departments' document was released, the Securities Regulatory Commission issued (regulatory guidelines for the issuance of asset-backed security tokens by domestic assets abroad), clarifying a key signal: Domestic entities that actually control the underlying assets can issue asset-backed security tokens abroad as long as their registration information is complete and accurate.

Many people interpret this move as 'regulatory relaxation of RWA,' but in actuality, it is not a complete relaxation but 'precise guidance'—in the context of the Securities Regulatory Commission, there is fundamentally no concept of 'RWA.' The official definition of 'domestic assets issuing asset-backed security tokens abroad' has clear boundaries and requirements, and the core logic has three points:

1. Clear boundaries: Only recognize 'cash flow support,' refuse 'speculative trading.'

The document clearly states that such tokens must be backed by cash flows generated from domestic assets or asset rights as the payment support certificate, rather than asset ownership—simply put, it means 'there is real revenue support,' not speculative tokens issued out of thin air.

Moreover, eligible domestic assets must first register with the Securities Regulatory Commission. Whether the registration can be approved depends primarily on the compliance of the assets and the verifiability of cash flows—this effectively blocks the possibility of 'speculation through indirect means' at the source, essentially making it 'on-chain ABS,' rather than the 'RWA speculation' understood by the market.

2. Underlying logic: Responding to dollar assets going on-chain, competing for global liquidity.

The reason the regulatory authorities are willing to open this door is that they have clearly seen the global trend of 'assets going on-chain': Currently, the U.S. is vigorously promoting dollar assets going on-chain, essentially using on-chain channels to siphon global liquidity and consolidate the dollar's global hegemonic position.

In this context, China also needs to take proactive measures: Allowing high-quality domestic assets to issue asset-backed security tokens abroad can not only enable Chinese assets to leverage the liquidity of the global blockchain market and achieve financing with lower issuance costs, but also guide foreign funds back to domestic markets to support the real economy—this is a response that follows the trend and a new attempt at 'financial outreach.'

The reason for still prohibiting the issuance of RMB-pegged stablecoins is primarily to maintain monetary sovereignty: If RMB stablecoins are allowed to be issued abroad while virtual currencies are strictly prohibited domestically, it would lead to awkward disconnects between 'inside and outside,' potentially triggering cross-border capital flow risks. Therefore, the regulatory authorities have chosen to 'temporarily prohibit' to prioritize the security of monetary sovereignty.

3. Policy connection: Revitalizing existing assets is consistent with REITs policies.

Traditional asset-backed securities (ABS) are an important tool for revitalizing existing assets, but the current domestic ABS market still faces issues such as scale limitations, long approval cycles, and a single investor structure. Issuing asset-backed security tokens abroad theoretically takes advantage of the global market to further broaden financing channels and enhance asset liquidity—especially suitable for 'large existing assets with poor liquidity' such as infrastructure, commercial real estate, and supply chain financial assets.

This is consistent with China's recent push for REITs and infrastructure REITs, with the core goal being 'to turn idle money into active money' and guide funds towards the real economy rather than speculative fields.

Key reminder: An opening does not equal relaxed regulation; micro and small practitioners basically have no opportunity.

It should be clarified that the 'opening' from the Securities Regulatory Commission is not meant for all practitioners; rather, it reflects 'precise stratification within strict management.'

1. Eligible entities: Those who can participate are likely institutions that have smooth communication with the Securities Regulatory Commission and possess strong compliance capabilities (such as brokerages and large state-owned enterprises). They must meet multiple requirements including registration with the Securities Regulatory Commission, foreign exchange management, and network data security, essentially making it a 'banking-like' professional service.

2. Excluding entities: For the vast majority of small teams, ordinary entrepreneurs, and those previously engaged in virtual currency consulting, traffic diversion, and knowledge payment, there is almost no opportunity—this high-pressure regulation from the eight departments has completely blocked such 'grey area' businesses, and there is no compliant space left for related businesses to operate domestically.

3. Regulatory bottom line: The early scale will not be too large, limited by registration thresholds, foreign exchange controls, etc., more like a 'pilot, complementary tool,' rather than a mainstream financing channel; any attempts to circumvent regulation or engage in disguised speculation will still be severely cracked down upon. The regulatory authorities' 'prevention of speculation and maintenance of security' bottom line has never wavered.

Conclusion: Behind the two major hotspots are choices made through 'rational games.'

Looking back at today's two major hotspots, they are actually the result of each party's 'rational game': Trump's 'inactivity' regarding Iran is not cowardice, but 'speculative caution' after weighing pros and cons, primarily unwilling to pay too high a price and touch his own political red line; the regulatory authorities' 'tightening + guiding flows' is not a contradiction, but a manifestation of refined governance, with the core being 'to combat speculation, support compliance, and maintain security.'

Subsequently, the U.S.-Iran negotiations are likely to continue to drag on, with Israel's attitude and Iran's internal situation becoming key variables; meanwhile, in the field of virtual currencies, the pattern of 'high-pressure regulation + precise guidance' will also persist long-term, and compliance and securitization will become the only way for domestic assets to go on-chain.

We will continue to monitor the latest dynamics of the two major hotspots, promptly breaking down the underlying games and opportunities, remember to like and follow, and don't miss key interpretations~