Short answer: yes. But…

What happened

This week wasn’t driven by a single event or headline. It was the result of several pressures lining up and then releasing at the same time.

Macro conditions were already fragile.

• Liquidity is still being drained.

• Rate expectations haven’t eased.

• Tech stocks started to soften again,

and crypto continues to react to that environment faster and more violently than most other assets. That part isn’t controversial. It’s been the backdrop for months.

What changed this week was the structure.

Bitcoin didn’t drift lower. It moved quickly, through levels that usually slow price down. That kind of move doesn’t come from people calmly changing their minds. It usually comes from positions being closed because they have to be.

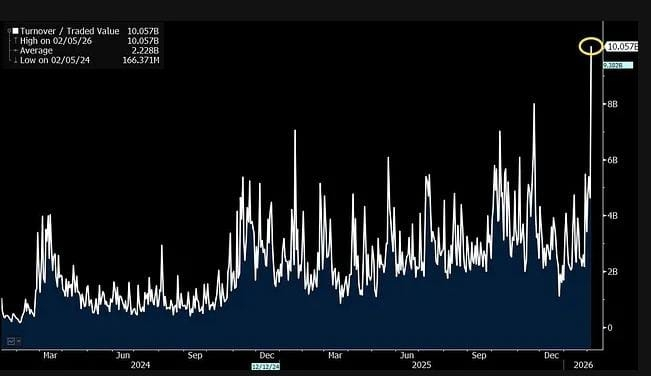

The clearest signal showed up in IBIT. This was the highest IBIT options volume day ever recorded, almost double the previous peak. That tells you institutions weren’t sitting on their hands. They were actively trading downside and protection at size.

Heavy volume like that doesn’t mean panic, and it doesn’t mean one sided selling. It means large players were willing to transact at lower prices, immediately.

At the same time;

• leverage came out of the system fast.

• Funding rates turned deeply negative.

• Long positions were liquidated in a short window.

That’s the signature of forced selling. It’s not about conviction. It’s all about margin.

There’s a plausible explanation for why this unwind looked the way it did. A meaningful share of IBIT exposure sits inside single-asset funds, many of them outside the US, particularly in Asia. These structures isolate margin by design. They don’t cross-collateralize with other strategies. When something breaks inside them, the response isn’t gradual. Positions get cut.

The timing was important. This happened while other leveraged trades were already under stress.

• Japan’s carry trade has been unwinding.

• Silver collapsed sharply.

• China tightened its stance around stablecoins and tokenization.

• Liquidity across several markets thinned at once.

When that happens, the most liquid venues tend to absorb the shock first.

Crypto did exactly that.

By the end of the week, sentiment reflected the damage. Fear readings dropped to levels usually associated with crisis periods, not routine corrections.

That doesn’t tell you what comes next. It only tells you that a lot of people stopped feeling comfortable very quickly.

That’s the sequence of events.

Where we are?

After a forced unwind, markets behave differently.

• Leverage is lighter now.

• Funding has stabilized after turning sharply negative.

• Most of the easy liquidations have already happened.

That doesn’t mean the market is “safe.” It means fewer participants are being pushed out mechanically.

Several institutional desks described this move as momentum driven liquidation rather than a reassessment of long term fundamentals. That distinction important, because it changes how capital responds after the fact. Selling driven by margin tends to end when margin is gone.

ETF behavior fits that picture. Volume stayed elevated even as price fell. That’s not disengagement. That’s basic repositioning. Capital didn’t leave. It adjusted.

Ethereum is the quiet counterpoint. Price remains weak, but usage doesn’t show stress.

• Monthly active addresses just reached a new high.

• The validator entry queue is the largest it’s ever been.

• For every one ETH trying to exit staking, well over a hundred are waiting to enter.

That kind of imbalance doesn’t show up in price immediately, but it says something about how long term holders are behaving.

Institutional activity around Ethereum hasn’t slowed either. BlackRock, Fidelity, JPMorgan are still building and expanding real products. That work isn’t speculative and it isn’t sensitive to short term price moves.

Regulatory progress continues in the background. It’s slow and procedural, but the tone is materially different from previous cycles. Less adversarial, more technical. That doesn’t create rallies yes, but it does change the environment over time.

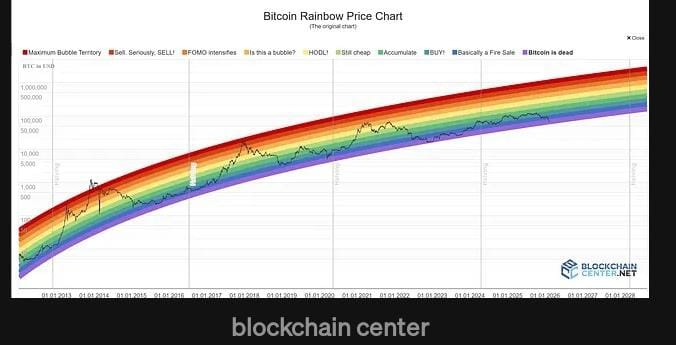

Bitcoin itself is sitting near long-observed historical reference levels that tend to appear after forced selling phases. These areas have never felt obvious in real time. They didn’t in past cycles either. They felt uncertain, often frustrating, and usually earlier than most people were comfortable with.

So…

Is bitcoin dead?

Long answer: It’s officially in the dead zone now (look at the rainbow chart).

Remember, long term holders start selling when everybody screams that it will go to the moon, right?

So, when do they start buying?

• • • • • •

Price could still move lower. It could also spend time going nowhere. Markets often do that after stress events.

What has changed is the quality of the selling. It looks less deliberate and more exhausted.

• Fear is high (all time record “5” at Feb 6. It’s crazy).

• Confidence is thin.

• Narratives are scattered.

That’s not a signal. It’s just context.

And context is usually the only useful thing when certainty disappears…

That was the week.

Talk again soon…

Follow me for more educational content 🫶