Tesla is entering 2026 with a massive "war chest" of nearly $44.1 billion in cash and investments. Despite a drop in net income in Q4 2025, their core business remains highly profitable, generating strong cash flows that can easily fund the expensive production ramps for the Cybercab (Robotaxi), Semi, and Optimus robot projected for this year.

Tesla is entering 2026 with a massive "war chest" of nearly $44.1 billion in cash and investments. Despite a drop in net income in Q4 2025, their core business remains highly profitable, generating strong cash flows that can easily fund the expensive production ramps for the Cybercab (Robotaxi), Semi, and Optimus robot projected for this year.

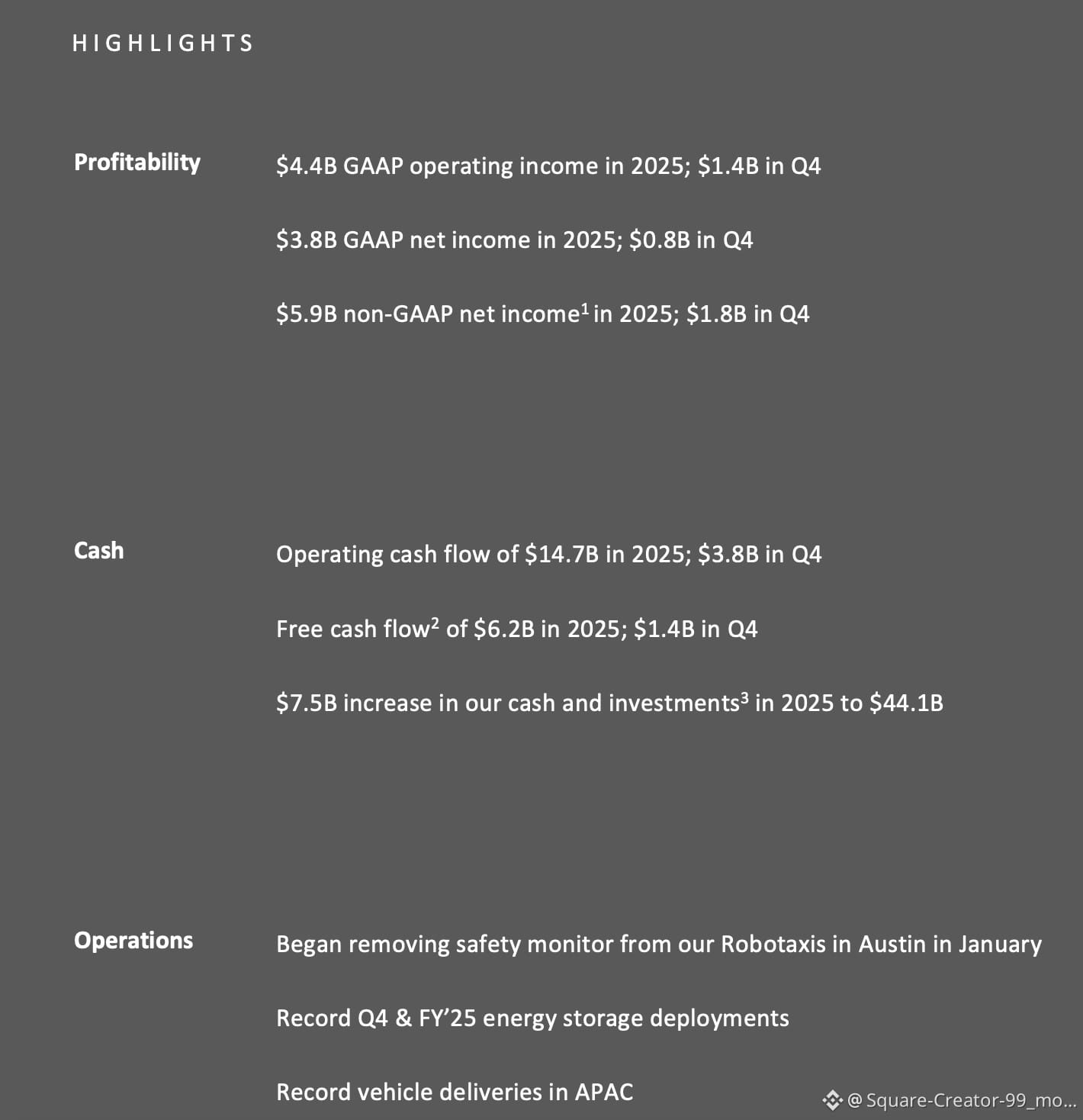

1⃣ Financial health snapshot

The numbers from the Q4 2025 report paint a picture of a company sacrificing short-term "paper profit" to invest heavily in future growth, while maintaining an exceptionally strong balance sheet.

💰 Cash position: Tesla holds $44.06 billion in liquid assets (cash, equivalents, and investments). This is an enormous safety buffer. To put this in perspective, they could run the entire company for over a year with zero revenue and still have cash left over.

💰 Liquidity: Their total debt (current + long-term) is approximately $8.4 billion. With $44B in the bank, they have a net cash position of roughly $35 billion. This is rare for an automaker and gives them immense flexibility to take risks.

💰 Cash flow: In 2025, Tesla generated $14.7 billion in operating cash flow (cash entering the business from selling cars/energy). After spending ~$8.5 billion on capital expenditures (factories/equipment), they still had $6.2 billion in free cash flow (FCF) left over.

2⃣ The "hidden" strength: margins are recovering

You might notice that Net income dropped significantly in Q4 2025 ($856M) compared to Q4 2024 ($2.1B). However, this is misleading if you only look at the bottom line.

✅ Core business is stronger:

Look at Gross profit (revenue minus cost of goods). It actually increased from $4.1B in Q4-2024 to $5.0B in Q4-2025.

✅ Automotive gross margin:

This key metric jumped to 20.4% in Q4 2025 (up from ~16-17% earlier in the year). This signals that Tesla has fixed its efficiency issues just in time for the 2026 product wave.

✅ Why did net income drop?

The drop was caused by a massive increase in Operating expenses (likely R&D for AI/Optimus) and a $1.2B negative swing in "Other income" (likely volatile items like foreign exchange or crypto fluctuations), not because they sold fewer cars.

3⃣ Can Tesla afford the 2026 product roadmap?

The year 2026 is expected to be capital-intensive, but Tesla's $44B cash pile is more than sufficient to cover expected costs without borrowing.

🚖 Cybercab / Next-gen platform: This will require high capital expenditure (estimated $5B - $8B) to build new lines at Giga Texas. Verdict: Yes. This cost is covered by just one year of their current operating cash flow alone.

🚚 Tesla Semi ramp: Expanding the production lines in Nevada will likely require moderate spending ($1B - $3B). Verdict: Yes.

🤖 Optimus (Robot): This requires high R&D (OpEx) and initial production tooling. Verdict: Yes. They are already spending ~$3.6B per quarter on operating expenses to support initiatives like this.

📈 xAI investment: Tesla recently committed approximately $2B to invest in xAI. Verdict: Yes. This represents less than 5% of their total cash holdings.

⚓️ VERDICT: THE FUTURE IS BRIGHT

Tesla does not need to borrow money or sell more stock to fund its 2026 plans. They are effectively "self-funding" their growth.

The financial data indicates they are pivoting from a pure car company to an AI/robotics company, resulting in higher R&D spending now (lower net income) in exchange for potentially massive future revenue 🚨

🚸 Warning 🚸 I do not provide financial advice 🔞The intent of this content is for you to be aware of market conditions before starting to invest 👌Thank you for reading 👌