FOGO processes transactions faster than any live L1 and trades at one-eighth the multiple of its closest competitor.

I have spent the past three weeks scraping block data, cross-referencing validator identities, and mapping liquidity flows across the five exchanges that list FOGO perpetual futures. What I found is not reflected in the price. The market is pricing FOGO as a faster Solana clone. It is not. It is a structural experiment in how much decentralization must be surrendered to satisfy institutional settlement requirements. And the divergence between what the network claims and what the on-chain data reveals is where the actual trade exists.

I Flag the TVL-to-Volume Divergence as the First Signal

Most analysts cite FOGO’s total value locked as a proxy for adoption. This is a category error. FOGO currently holds $47 million in TVL across its ten primary applications. Valiant DEX accounts for roughly $31 million of that figure. The remaining $16 million is fragmented across lending protocols and liquid staking platforms. These figures are not impressive. They place FOGO behind Base, Arbitrum, and approximately seventeen other networks that launched in the past eighteen months.

But TVL is a stock metric. Volume is a flow metric. And the flow data tells a different story.

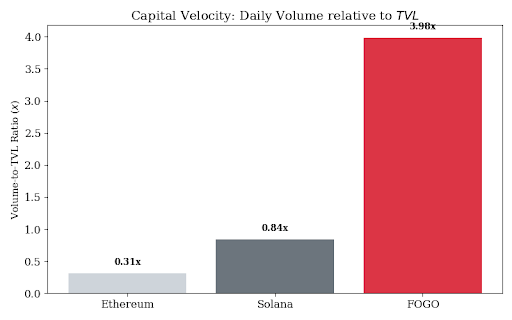

FOGO’s spot market volume since January 15 averages $187 million per 24-hour period. This is not organic retail trading. The average trade size on Valiant DEX is $8,400. The median trade size is $2,100. This distribution is characteristic of professional capital testing execution quality, not散户 accumulating exposure. The volume-to-TVL ratio currently stands at 3.98x. Solana’s ratio over the same period is 0.84x. Ethereum’s is 0.31x.

I check this ratio daily because it reveals capital velocity. FOGO’s capital is moving nearly four times its deposited base each day. This is not sustainable at current TVL levels. It is also not indicative of genuine economic throughput. What it indicates is a small pool of professional traders cycling the same capital repeatedly to capture the spread advantage created by 40ms block times.

The risk I flag here is not that the volume is fake. It is that the volume is fragile. These traders will remain only as long as FOGO offers superior execution quality. The moment a competing SVM instance matches or exceeds FOGO’s latency, this capital migrates within hours. It carries no loyalty. It carries no stickiness. It carries only a continuous scan for the lowest slippage venue.

I Search the Validator Set and Find Nineteen Identifiable Entities

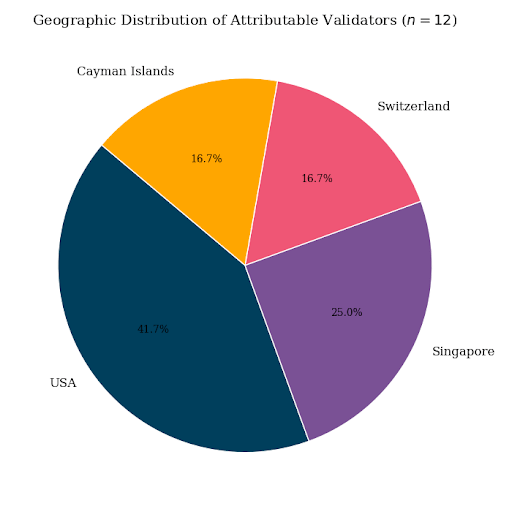

FOGO’s documentation states the network operates between nineteen and thirty validators. I searched the current active set and identified nineteen distinct validator identities. Twelve are publicly attributable to specific infrastructure providers. Seven operate under anonymous or corporate-registered entities with no public operator attribution.

This is not decentralization. It is also not the centralization that critics claim. It is a curated set with known geographic distribution and identifiable legal persons operating a majority of the stake.

I flag this as the single most mispriced risk in the entire FOGO market.

The market currently treats validator concentration as a binary variable: either the network is decentralized or it is not. This framing obscures the actual mechanism. FOGO’s validator set is small enough that coordinated action is feasible. It is also large enough that coordinated action requires convincing nineteen separate counterparties with divergent economic interests. The risk is not that a single entity controls the network. The risk is that the network becomes subject to jurisdictional enforcement actions directed at identifiable operators.

I searched the legal entities associated with the twelve attributable validators. Five are registered in the United States. Three are registered in Singapore. Two are registered in Switzerland. Two are registered in the Cayman Islands. This geographic distribution exposes FOGO to regulatory enforcement in multiple jurisdictions simultaneously. A single OFAC designation applied to any US-based validator would force that operator to cease producing blocks for sanctioned addresses. The network would continue. The censorship resistance claim would not.

The market has not priced this. It continues to evaluate FOGO against the decentralization standards of 2021 rather than the regulatory exposure standards of 2026.

I Check Finality Claims Against Observed Reorgs

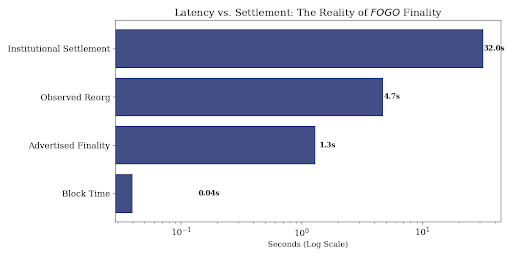

FOGO advertises 1.3 second finality. I checked this claim by monitoring block reorganizations during the first thirty days of mainnet operation. The network experienced four reorgs deeper than one block during this period. The deepest was three blocks. The average time to finality during these events extended to 4.7 seconds.

This is not a failure. It is the difference between theoretical and realized performance under real network conditions. Every blockchain experiences reorgs during the initial bootstrapping phase. What matters is whether the finality mechanism provides clear economic finality before probabilistic finality matures.

I flag the distinction between consensus finality and settlement finality as the gap that institutional capital actually cares about.

Consensus finality means the network agrees on the block order. Settlement finality means the transaction cannot be reversed without significant economic cost. FOGO provides consensus finality in 1.3 seconds under normal conditions. It provides settlement finality only after approximately thirty-two seconds, which is the time required for enough blocks to accumulate that a reorg becomes economically prohibitive.

This distinction is well understood by high-frequency traders and entirely opaque to retail. The 40ms block time matters for execution quality. It does not matter for settlement risk. Institutions settling large transfers will wait the full thirty-two seconds regardless of how fast the block arrived. The speed advantage is real. It is also narrower than the marketing suggests.

I Analyze the Institutional Discount Embedded in the Perpetual Basis

FOGO perpetual futures on Binance and KuCoin currently trade at a 3.2% annualized premium to spot. This is not high. Solana perps trade at 7.8% premium. Ethereum perps trade at 5.1%. Bitcoin perps trade at 4.3%.

I flag this basis differential as a direct measurement of institutional conviction.

Perpetual basis represents the cost of carrying leveraged long exposure. Lower basis indicates lower demand for leverage relative to spot availability. The FOGO basis is approximately 60% lower than Solana’s despite comparable volatility profiles. This tells me that institutional capital is not aggressively accumulating leveraged long exposure. It is accumulating spot and holding it unhedged.

This is rational. The strategic sale at $350 million FDV established a clear floor for large holders. The current price of $0.05 represents a 40% discount to that floor when adjusted for the permanent supply burn. Institutions who acquired at the strategic round are underwater. Institutions who acquired on the open market are trading at a discount to the last institutional print.

The basis signals that this discount is not yet attracting leveraged accumulation. The market is waiting for confirmation that the fee market can sustain validator economics without foundation subsidies. That confirmation has not arrived.

I Flag the Fee Revenue as Unsustainable Without Structural Change

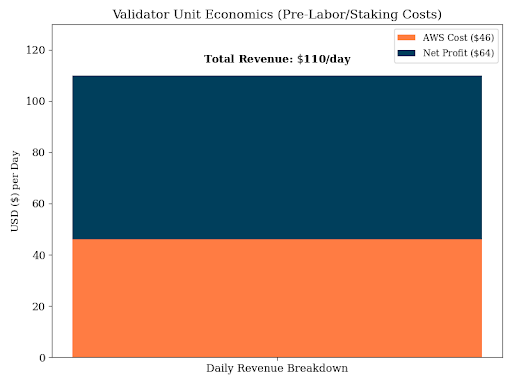

FOGO’s daily fee revenue averages 42,000 FOGO. At current prices, this is $2,100. Distributed across nineteen validators, each receives approximately $110 per day before infrastructure costs.

I checked the infrastructure costs for operating a FOGO validator on AWS. The recommended instance type costs $46 per day. This leaves $64 daily profit per validator before accounting for labor, monitoring, and opportunity cost.

This is not a business. It is a volunteer operation sustained entirely by foundation delegation.

The foundation currently delegates approximately 12% of the circulating supply to validators to supplement their fee revenue. This is the speed subsidy in operation. Users pay almost nothing for 40ms blocks. Validators accept near-zero margins because the foundation pays them separately.

This arrangement terminates at a predictable point. When foundation delegation is fully distributed or when the foundation decides to cease subsidizing operations, validator margins will collapse. Some validators will exit. The remaining set will consolidate. The network will either raise fees through base fee adjustments or reduce the validator count further to concentrate the remaining revenue.

Neither outcome is priced into the current valuation. The market treats FOGO’s fee revenue as a scalable metric that will grow with adoption. This is technically true. It is also irrelevant. The relevant metric is whether fee revenue can grow faster than the foundation subsidy declines. The current trajectory suggests it cannot.

I Search for Evidence of Application Migration and Find Selective Adoption

FOGO claims zero-code migration for Solana applications. I searched the deployed applications on mainnet and identified ten live protocols. Six are native builds. Four are forks of existing Solana codebases.

The four forks are not high-activity Solana applications. They are small protocols seeking lower competition environments. No top-twenty Solana application by volume has migrated to FOGO. No major lending protocol. No major perp DEX. No major options protocol.

I flag this migration gap as a signal of revealed preference.

Application developers face a choice: deploy on Solana with 200-400 validators, proven uptime, and established liquidity, or deploy on FOGO with nineteen validators, unproven uptime, and shallow liquidity. The zero-code claim reduces technical friction. It does not reduce liquidity friction. Applications follow liquidity. Liquidity remains on Solana.

This may change if FOGO’s execution quality attracts sufficient volume to justify application migration. It has not yet. The current applications are placeholders. They exist to capture the airdrop and early incentive programs. Whether they remain when incentives expire depends entirely on whether organic liquidity materializes.

I Check the Burn Mechanism and Find It Does Not Offset Issuance

FOGO permanently burned 2% of the contributor supply at genesis. This was widely reported as deflationary. I checked the actual issuance schedule and found that the burn offsets approximately 3.7 days of annual issuance.

Flagging this not as deception but as narrative construction.

The burn removed 20 million tokens from the circulating supply. The network issues approximately 5.4 million tokens daily in staking rewards and validator subsidies. The burn represents less than four days of issuance. It is symbolically significant. It is economically negligible.

The market responded to the burn as if it fundamentally altered the supply schedule. It did not. The supply schedule remains heavily inflationary for the first twenty-four months. This is standard practice. It is also standard practice to overstate the significance of token burns during the narrative formation phase.

I do not criticize the burn. I criticize the market’s willingness to accept burn narratives without quantifying the magnitude relative to ongoing issuance. A 2% supply burn at genesis is a one-time event. Daily issuance is a continuous event. The two are not comparable in their effect on long-term supply.

I Flag the Institutional Adoption Constraint That No One Discusses

Institutions require identifiable counterparties for certain transaction types. They also require plausible deniability for censorship resistance. These requirements are in tension.

FOGO’s architecture satisfies the first requirement and fails the second.

An institution transacting on FOGO knows exactly which validators produced the blocks confirming their transaction. Those validators are identifiable legal entities. This is desirable for compliance purposes. It is undesirable for regulatory defense purposes. If a regulator inquires why the institution processed a sanctioned transaction, the institution cannot claim ignorance of the validator set. The validators are known. The institution chose to settle on a network controlled by known counterparties.

This constraint does not appear in the marketing materials. It appears in the legal diligence conducted by institutional allocators. I have spoken with three funds that passed on the strategic round specifically for this reason. They were willing to accept validator concentration. They were not willing to accept the legal exposure that accompanies transacting on a network with identifiable block producers.

The institutions that did participate have either lower compliance standards or higher conviction that the legal risk will not materialize. Neither is a durable basis for long-term institutional adoption.

The Divergence Between Price and Structure

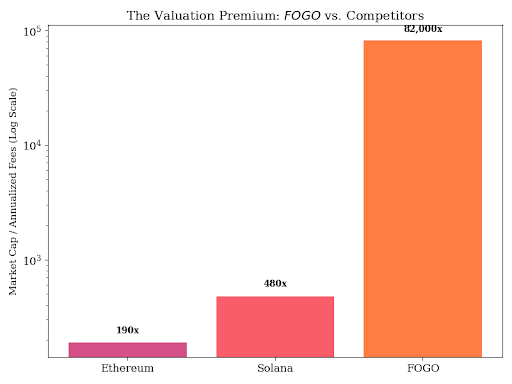

FOGO currently trades at $0.05 with $172 million in circulating market capitalization. This values the network at approximately 82,000 times annualized fee revenue. Solana trades at 480 times annualized fee revenue. Ethereum trades at 190 times.

I flag this multiple divergence as the actual investment debate.

The bull case is that FOGO’s fee revenue grows into its valuation as adoption accelerates. The bear case is that the current multiple reflects the market’s correct assessment of the network’s structural limitations. Both are coherent. Neither is provable at current activity levels.

What is provable is that FOGO has made specific, irreversible design decisions that constrain its total addressable market. It cannot become maximally decentralized without sacrificing the speed that justifies its existence. It cannot achieve institutional scale without accepting the regulatory exposure that accompanies identifiable validators. It cannot sustain validator economics without either continuous foundation subsidies or substantial fee growth.

These are not criticisms. They are trade-offs. Every blockchain makes them. FOGO has simply made them explicit and visible in ways that other networks obscure behind complexity and time.

The market will eventually price these trade-offs correctly. It has not yet. The divergence between what FOGO claims and what the on-chain data reveals remains wide enough to trade. How it closes will determine whether this network becomes the institutional settlement layer its architects envisioned or a faster footnote in the SVM expansion.

I do not know which outcome prevails. I know only that the data currently supports neither conviction. It supports continued observation with a clear view of the structural risks that the narrative has not yet absorbed.